3 Healthcare Stocks That Are Looking Cheap

After a years-long bull run, it's not easy to find cheap stocks. If unusually high stock valuations across the board have you feeling frustrated, I've got few special treats for you. CVS Health Corp (NYSE: CVS), Gilead Sciences, Inc. (NASDAQ: GILD), and Omega Healthcare Investors Inc (NYSE: OHI) are three awesome-sauce healthcare stocks that operate in different corners of the sector. One thing they all have in common, though, are recent prices that bargain hunters will find hard to pass up.

Let's have a look at each to see if any fit in your portfolio.

Image source: Getty Images.

Much better together

Although nearly all of us have shopped at one of CVS Health's 9,700 retail pharmacies, it's what you don't see on the shelves that makes this a great stock. CVS' list of integrated healthcare businesses is long, but the most important one is a pharmacy benefits manager (PBM) that boasts about 90 million plan members.

Combined, the PBM and retail chain gives CVS unprecedented leverage to negotiate favorable prices from prescription drug manufacturers. As you can see, the unique mix has allowed CVS Health to maintain a higher operating profit margin than Walgreens and Express Scripts, its fiercest competitors in the retail pharmacy and PBM spaces, respectively.

CVS Operating Margin (TTM) data by YCharts.

Expanding specialty pharmacy services, a successful Medicare part D prescription drug plan, and a recently acquired senior pharmacy care business that serves over one million patients annuallyhave also allowed CVS' top line to grow at an impressive clip that isn't showing signs of a slowdown. In fact, the average analyst following CVS expects 10.4% annual bottom-line growth over the long run.

With such a rosy outlook, you might expect CVS Health to be one of the more expensive large-cap stocks, but it's not. At recent prices, its shares are trading at just 16.4 times trailing earnings. That's miles below the average stock in the broad market S&P 500 index, which has climbed to an eye-watering 24.9 times trailing earnings.

Are you serious?

Another year of outstanding HIV and hepatitis antiviral sales helped Gilead Sciences generate a stunning $15.9 billion in free cash flow last year, which works out to $11.73 per share. That means at recent prices, this leading biotech stock is trading at the ridiculously low price of 5.9 times free cash flow.

The reason it's so low has to do with flagging sales for its hepatitis C virus (HCV) franchise that's expected to continue into 2017 -- and perhaps longer. With an estimated 180.6 million people around the globe carrying HCV, demand for a cure isn't about to evaporate.That said, it's hard to say just how much lower sales will fall. Patients in earlier stages of the infection are generally curable with shorter treatment durations -- and less willing to seek treatment until their symptoms become difficult to ignore.

Image source: Getty Images.

Unfortunately for patients, HIV still requires lifelong treatment. Luckily, Gilead's recently-launched, single-pill options are far more tolerable than earlier drug cocktails. Sales of the new treatments are surging, and I expect them to continue climbing in the long term.

A lack of thrilling candidates in development has also taken a toll on Gilead's stock price. The company has one of the most promising programs aimed at the growing non-alcoholic steatohepatitis (NASH) epidemic. This indication lacks an effective treatment, and the first to succeed will probably generate several billion in annual sales.

Of course, investors would love to see Gilead make another transformative acquisition, such as the one that spawned its HCV franchise. Despite returning heaps of cash to shareholders in the form of share buybacks and a dividend that yields about 3% at recent prices, its balance sheet boasts a $32 billion cash pile. That should be plenty to stock its pipeline with some clinical-stage excitement.

18 straight payout bumps

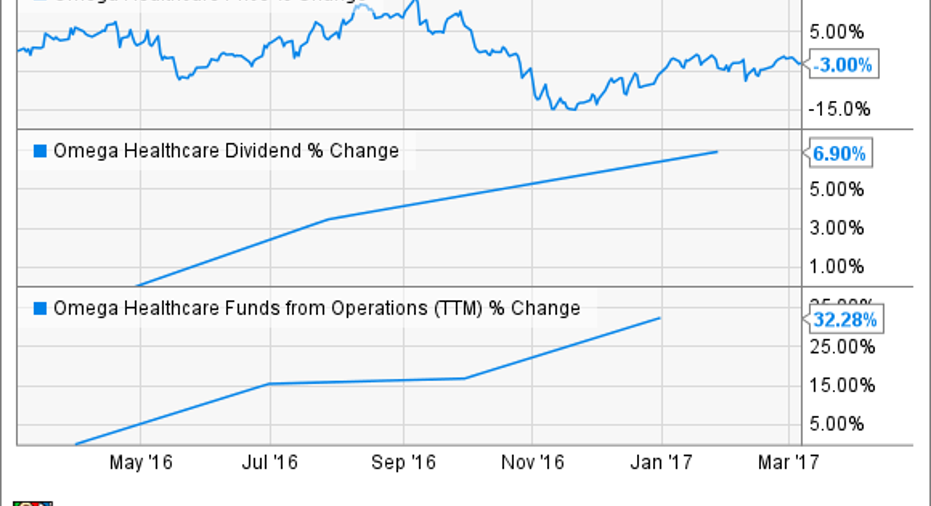

While most dividend-paying companies raise their quarterly payments once per year, Omega Healthcare Investors has treated its investors to a raise in each of the past 18 quarters. This real estate investment trust (REIT) provides capital to skilled nursing and assisted-living facility operators in the form of triple-net leases. In a nutshell, this means Omega collects rent from facility operators that remain responsible for property taxes, maintenance, and insurance.

The combination of longer life spans and scores of baby boomers approaching their twilight years make these types of facilities a growth industry. Plus, Omega's hands-off approach keeps it laser-focused on what it does best, which includes paying shareholders a juicy dividend that offers a 7.7% yield at recent prices.

Over the past several quarters, Omega's stock price has languished while funds from operations (FFO) rose significantly. Last year, FFO jumped 29.8% over 2015 to $3.27 per share, and management expects between $3.38 and $3.42 per share this year. The latest dividend raise works out to an annualized $2.48 per share, which gives the healthcare REIT plenty of room for the 19th consecutive quarterly dividend hike.

10 stocks we like better than Omega Healthcare InvestorsWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Omega Healthcare Investors wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

Cory Renauer owns shares of Gilead Sciences. The Motley Fool owns shares of and recommends Gilead Sciences. The Motley Fool owns shares of Express Scripts. The Motley Fool recommends CVS Health. The Motley Fool has a disclosure policy.