3 Facts About Claiming Social Security At 62

SOURCE: FLICKR USER 401KCALCULATOR.ORG

59 million Americans receive Social Security and tens of millions more are fast-approaching retirement age, but that doesn't mean that everyone knows everything about this important program. Here are three facts that everybody should know if they plan to file for Social Security at age 62.

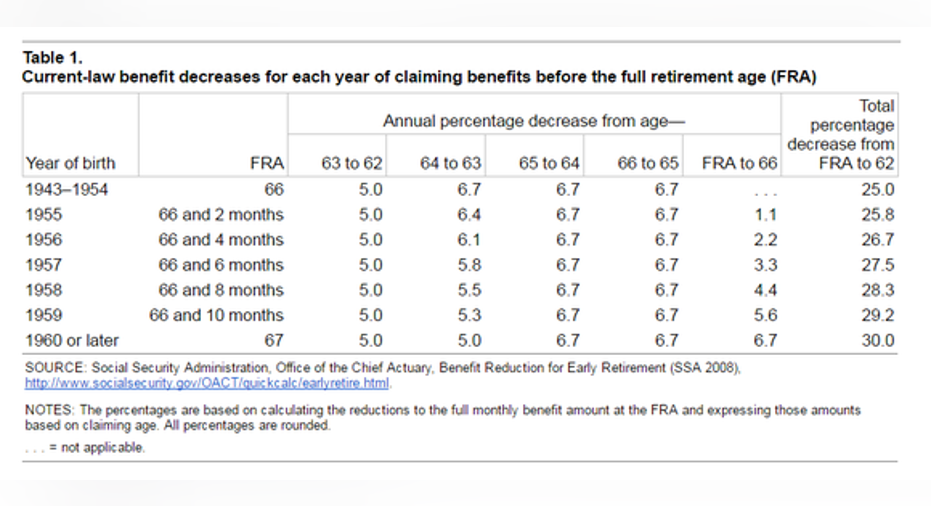

No. 1: Smaller checksSocial Security is designed so that the average person gets the same amount in total lifetime benefits regardless of whether they claim early at 62 or wait until 70. That means that the size of the monthly Social Security check that hits your bank account is less if you claim when you're younger and more if you claim when you're older.

Currently, the full retirement age, or age at which you can receive 100% of your Social Security benefit, is 66. If a person with that full retirement age claims benefits at age 62, they'll receive 25% less than if they wait until 66. If they delay until age 70, then they'd receive 32% more than they'd receive at age 66.

The exact percentage less that any individual will receive will vary depending on birth month and birth year, but nevertheless, claiming at 62 will result in a smaller check than if you wait.

No. 2: You can change your mindOne advantage that is afforded to some Americans who claim Social Security early is the ability to pay back the money received and reset the clock on their benefits.

For example, if you claim at 62 and then get offered the job of a lifetime within 12 months, you can cut Social Security a check for past Social Security income that you've received and then refile later on. That move allows you to receive 100% of your benefit at full retirement age, or to receive more than 100% if you wait until you turn 70 to refile.

Unfortunately, there are a few rules that have to be followed. First, you can only do this within 12 months of claiming your Social Security. Second, if any other people receive benefits on your record (for instance, a spouse), then they'll need to consent to your withdrawing your application. Third, you're eligible for this option only once.

If you are below full retirement age, but beyond the 12 month window, you're not completely out of luck.

Social Security reduces your Social Security check by $1 for every $2 you earn in income from working above $15,720. Therefore, if your income is high enough, a large portion of your Social Security benefit will be withheld. Any money that does get held back by Social Security will be used later to increase the size of your monthly payments.

No. 3: Paying uncle SamMany Americans who claim Social Security at age 62 don't fully understand the tax consequences. Let's make sure that doesn't happen to you.

When you receive Social Security above a certain amount, you'll have to pay taxes on some of that money, however, no one pays the IRS taxes on more than 85% of their Social Security income.

Specifically, if you're single, and your combined income (adjusted gross income + nontaxable interest + one half of your Social Security benefit) is between $25,000 and $34,000, you may have to pay taxes on up to half of your Social Security benefit. Earn more than $34,000 in combined income, and you could be taxed on 85% of your benefit. Married couples with a combined income between $32,000 and $44,000 could pay taxes on up to half their benefit, while couples earning more than $44,000 in combined income may be taxed on up to 85% of their Social Security benefit.

The article 3 Facts About Claiming Social Security At 62 originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.