3 Companies That Might Not Live to See 2020

Sears Holdings (NASDAQ: SHLD), MannKind (NASDAQ: MNKD), and Novavax (NASDAQ: NVAX) face stiff headwinds that cast their future survival in doubt. Here's what's going wrong, and why our Motley Fool contributors think these companies might not be able to overcome their obstacles.

One foot in the grave

Rich Duprey (Sears Holdings): I've been predicting the demise of Sears Holdings for several years now, and one of these days I'm going to be right. Although the ability of CEO and chairman Eddie Lampert to keep the old-line retailer hanging surprised me, and ultimately proved wrong my (repeated) calls that it won't be around for Christmas, there's little argument Sears has been heading for the abyss. It's always been a matter of when, not if.

Image source: Getty Images.

Unfortunately, that day might be swiftly approaching. Heck, forget Sears not seeing 2020; it might not see 2018.

The problem for the retailer is that customers are abandoning the store in droves. And while Lampert's hedge fund-style financial gymnastics have kept the lights burning longer than expected, the continuous need for short-term cash infusions -- whether from loans Lampert gives it through his ESL Investments hedge fund, asset sales or spinoffs, or selling real estate -- indicates the business of Sears is dying.

Although I haven't been a fan of Lampert's management of the retailer over the past few years, I have to admit his most recent moves have almost been strokes of genius. Not that I think they'll save Sears, as they amount to too little, too late, but they are innovative ideas that, had they been implemented earlier, could have perhaps staved off the inevitable.

Of course, I'm talking about the way the sale of the Craftsman brand was structured, as well as the licensing deal for the Kenmore name. Equally brilliant was launching a DieHard-brand auto services center. People so closely associate the DieHard battery brand with cars that they rated DieHard tires one of their favorites -- even though DieHard doesn't make tires! An auto center should prove popular, and though there's only one planned right now, it's easy to see this concept expanding -- assuming, of course, Sears survives.

And that's just the problem: It likely won't. Earlier this year ratings agency Moody's downgraded Sears to Caa2 as the likelihood of default rises due to comparable store sales during the holiday period plunging by as much as 13%. Of course, Sears' sales-comparison woes are related to the number of stores the retailer has closed or sold off, and since consumers generally don't view shopping at the retailer as a positive experience, comps will likely hemorrhage further.

While Lampert has made a big effort to expand Sears' digital capabilities, and there may be a future for the department store chain online, the possibility of it seeing 2020 is becoming increasingly unlikely.

A bad news biotech

Keith Speights(MannKind):Few companies have encountered as much bad news as MannKind. The company failed to win regulatory approval for inhaled insulin Afrezza in its first two attempts. When it seemed things might be finally going its way after finally securing approval, MannKind's partner, Sanofi , threw in the towel on marketing Afrezza.

The question facing MannKind now is: Can it succeed where a larger company couldn't? MannKind regained marketing rights to Afrezza in April 2016. The company struggled in its first several months of selling the drug using a contract sales team. CEO Matthew Pfeffer later admitted that the company was "working somewhat on fumes financially." MannKind even had to engage in a reverse stock split to avoid its stock being delisted.

It appears, however, that MannKind's management team is doing the right things to turn the ship around. A settlement with Sanofi brought in much-needed cash. The company discontinued use of the contract sales team and hired its own internal staff. MannKind has also made significant progress in winning payer coverage for Afrezza.

Despite all of these positive steps, MannKind still faces a tough road ahead. It could be that Afrezza simply doesn't take off at all -- or doesn't grow sales quickly enough for MannKind to be successful. If either scenario occurs, this long-suffering biotech won't be around to see the next decade. For now, however, I'd say MannKind has a fighting chance of survival.

Burning through cash

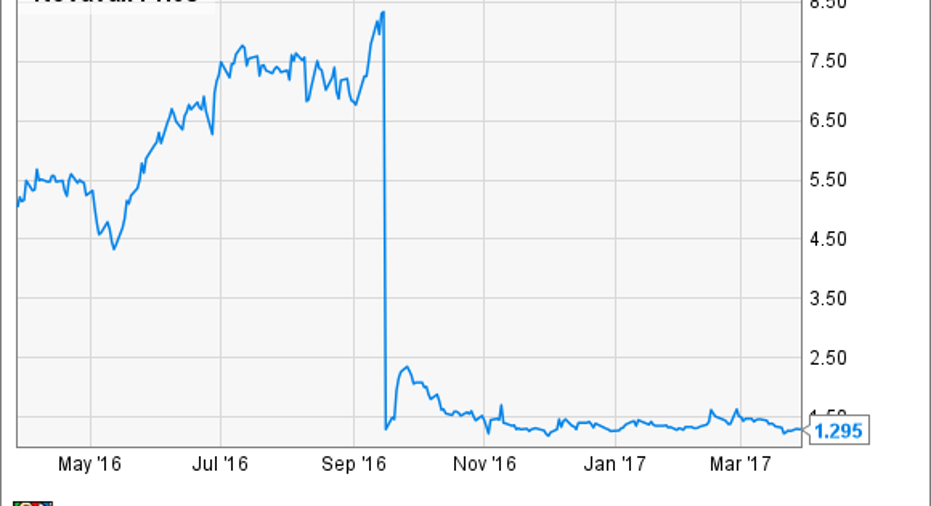

Todd Campbell (Novavax): A little good fortune could help Novavax sidestep risks associated with its high-risk financials, but absent a phase 3 win for its respiratory syncytial virus (RSV) vaccine, this company's future becomes pretty unclear.

A vaccine that protects people from this life-threatening virus could benefit millions of seniors and infants, and such a vaccine should be worth billions of dollars in sales. Unfortunately, Novavax reported last fall that a phase 3 study of its vaccine failed to beat out placebo in elderly patients, and since then, the company's shares have lost over 80% of their value.

Another phase 3 study seeking to determine if babies can be immunized via their mother, is ongoing, but that trial isn't expected to finish up for a couple more years, according to ClinicalTrials.gov.

Unfortunately, that timeline is worrisome because the company is losing a lot of money, and its ability to raise money isn't what it used to be. In the past, the company's relied on stock and convertible debt offerings for funding, but management burned through $255.5 million in cash last year, and it entered 2016 with only $235.5 million in cash on the books. Given the infant study isn't wrapping up for a bit, Novavax may have to tap investors again for financing, but I have to wonder when that well will run dry. After all, management is already on the hook for $316 million in long-term debt, and current investors aren't going to like the idea of further dilution, especially at current prices.

Obviously, it's anyone's guess if Novavax makes it to 2020 and beyond, or if its vaccine is ultimately a success. Nevertheless, there are simply too many questions surrounding this company for me to want to risk owning its shares right now.

10 stocks we like better than NovavaxWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Novavax wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Keith Speights has no position in any stocks mentioned. Rich Duprey has no position in any stocks mentioned. Todd Campbell has no position in any stocks mentioned. His clients may have positions in the companies mentioned.The Motley Fool owns shares of and recommends Moody's. The Motley Fool has a disclosure policy.