2016 SEP IRA Limits

Source: 401kcalculator.org via Flickr.

A SEP-IRA, whichstands for Simplified Employee Pension, can be a great tool for small-business owners to help their employees save for retirement, or for self-employed individuals to save for their own. For the 2016 tax year, the contribution limits remain the same, thanks to a lack of inflation. Here's what you need to know about the 2016 SEP-IRA limits, and how to calculate yours.

Generous contribution limitsThe contribution limits for SEP-IRA accounts are both straightforward and generous. Unlike many other retirement account types, such as 401(k) plans and SIMPLE IRAs, 100% of SEP-IRA contributions come from the employer. Employees are not required to, nor are able to, contribute to their own accounts.

For the 2015 and 2016 tax years, SEP contributions are capped by the lesser of these two criteria:

- 25% of the employee's compensation for the year

- $53,000

And unlike many other retirement account types, there's no such thing as SEP "catch-up" contributions for older employees. As I said earlier, the limits are pretty straightforward. SEP accounts definitely live up to the word "simplified" in the title.

Why did the limits stay the same for 2016?There was no inflation during the past year, so there was no need to increase retirement savings limits. The consumer price index (CPI) did not increase between the third quarter of 2014 and the third quarter of 2015, when the 2016 limits were determined.

The ability to contribute to retirement accounts is based on the increase in the cost of living over time. If the cost of living doesn't increase, retirement savings limits remain the same.

All retirement savings limits set by the IRS remained the same for 2016. In fact, the only significant changes were slight upward adjustments in certain retirement-related income thresholds, such as the maximum allowable income to contribute to a Roth IRA.

How to calculate the maximum SEP contributionFor employees, the calculation is easy -- simply multiply the total compensation by 0.25. For example, if one of your employees earns $50,000 this year, you can contribute up to $12,500 to their SEP-IRA on his or her behalf.

For self-employed individuals, it's a bit more complicated. Because self-employed SEP account holders fill both roles -- employer and employee, there are a couple of other factors that need to be taken into consideration. Specifically, the self-employment tax and the SEP contribution itself serve to reduce the income that can be considered toward the limit.

If you're self-employed, you can figure out your maximum SEP contribution with these steps:

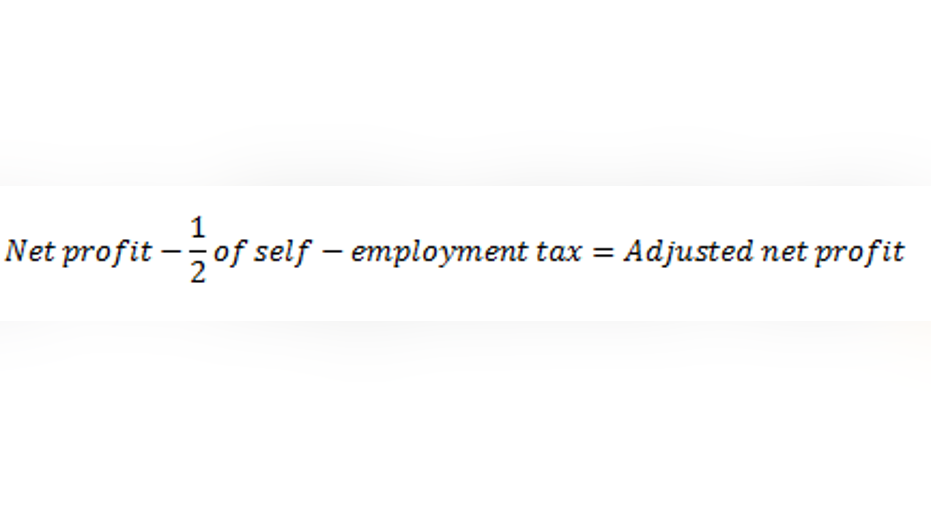

First, take your net profit for the year (from IRS Schedule C) and subtract one-half of your self-employment tax. This will give your adjusted net profit.

Then, divide this amount by 1.25, in order to remove the SEP contribution from your income. This number is your adjusted earned income.

Finally, multiply your adjusted earned income by 0.25 to determine your maximum 2016 SEP-IRA contribution.

Remember, the maximum SEP-IRA contribution for 2016 can't exceed $53,000, regardless of how much you earned.

Is a SEP-IRA right for you or your employees?There are plenty of reasons to use a SEP-IRA to save for retirement. Just to name a few:

- SEP-IRA plans are easy to establish and maintain.

- Contributions are flexible -- it's easy for employers to increase, decrease, or suspend contributions, as long as all employees receive an equal contribution rate.

- Contributions are made on a tax-deferred basis.

- Employees are always 100% vested in their accounts.

- Contributions can be invested in any stocks, bonds, or funds.

Small businesses have a few other options to help employees save for retirement, such as the SIMPLE IRA. Self-employed individuals can utilize those, as well, plus they have the additional option of a Solo 401(k). A SEP-IRA is an excellent retirement savings tool, but all of these account types have their benefits and drawbacks. That's why it's important to evaluate all of your options before deciding which is best for your individual circumstances.

The article 2016 SEP IRA Limits originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.