2 Stocks That Quadrupled (or More)

A company that quadruples in share price in a year is almost unheard of. Those kinds of gains are typically found in the nightmarish world of penny stocks, or if you're lucky, in a small biotech stock that gets approval for a blockbuster drug. Last year, though, two companies saw much more than 300% gains that in no way fit the mold of a high-flying stock: commodity chemical producer The Chemours Company (NYSE: CC)and independent oil and gas producer Clayton Williams Energy (NYSE: CWEI).

Let's take a look at how these two unlikely candidates were able to accomplish this feat, and whether there's any juice left to squeeze in these stocks.

Image source: Getty Images.

A quick rebound

The business of manufacturing chemicals isn't a glorious one, especially for commodity chemicals like the ones Chemours manufactures. Chemours is the world's largest producerof two chemicals: titanium oxide, a ubiquitous chemical used as a white pigment for plastics and coatings, and fluoroproducts, such as Teflon. These are good, but not great, businesses that deliver about 20% earnings before interest, taxes, depreciation, and amortization (EBITDA) margins, and don't have a whole lot of growth. These are hardly the qualities in a company that you'd expect to gain more than 300% in just a year's time.

To understand this vast increase in stock price, you have to look a little further back in time to 2015, when former parent company DuPont (NYSE: DD) spun off Chemours into a unique entity. Chemours was spun off because it was a stable cash-generatingbusiness without much growth, so Dupont loaded it up with more than $4 billion debt. The idea was that, with few needs for capital spending, Chemours could pay down the debt load and return cash to shareholders over time.

The problem was that Chemours IPO was not well received due to declining prices for its products, its very high debt load, and an indemnity clause in Chemours 10-k that said Chemours would be responsible for any legal liabilities related toperfluorooctanoic acid (PFOA) and the probable health risks it poses. As a result, shares of Chemours tanked in 2015.

While the risk of PFOA litigation expenses hasn't yet abated, Chemours benefited from some tailwinds in 2016. Rising prices for titanium oxide and other products allowed the company to generate enough free cash flow to start chipping away at that debt load. Since the company was showing signs of life and trading at an absurdly low 0.1 times sales at its nadir, investors started piling into this seemingly cheap cash-flow producer.

By no means should investors expect a repeat performance in 2017. The prices for Chemours' primary products are still increasing modestly, but certainly not enough to justify another 300% gain. If the company can continue to crank out free cash flow, trim its debt load, and not get ensnarled in some huge liability lawsuit related to POFA, it's not unreasonable to assume Chemours will have a decent year.

Right place, right time

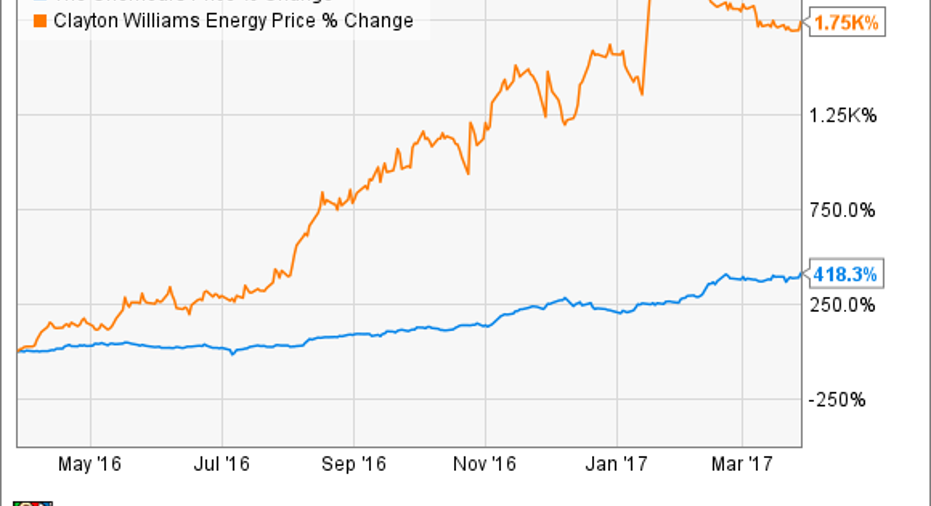

Up until 2016, Clayton Williams Energy wasn't a company that stood out in the oil and gas business. It produced a little less than 14,000 barrels of oil equivalent per day and had hemorrhaged cash for the past six years. It would have been quite easy for investors to overlook this stock for other producers. Yet over the past year, Clayton Williams stock has gained an unfathomable 1,700%.

What changed? During this past year, people started to realize the potential of a part of its portfolio -- 71,000 acres of land right in the heart of the Delaware Basin. Those discoveries have made the Delaware Basin -- part of the larger Permian Basin formation -- one of the hottest properties in the oil and gas business today.

The Permian Basin is known as a stacked play, which means it has multiple layers of shale rock in a single place that drillers can tap. Production companies are now more proficient at drilling shale wells, and it has made drilling in the Permian one of lowest cost production sources out there, with an average breakeven price of less than $30 per barrel across the Basin.

What was even more attractive about Clayton Williams was that this acreage holding has immense potential. Most of the work Clayton Williams has done on this land was tapping conventional reservoirs with vertically drilled wells, so those shale reservoirs are mostlyundisturbed. As investors unpacked the potential of this acreage, shares started climbing fast.

Clayton Williams also helped its own case by shedding its East Texas properties in October for $400 million. The sale helped to pay down debt and recapitalize the business. After all, the only way that Delaware Basin acreage could be valuable for Clayton Williams investors is if it gets developed.

What really sent shares of Clayton Williams skyrocketing was the announcement in January that Noble Energy (NYSE: NBL) would be buying Clayton Williams for $3.2 billion. That price tag is about $45,000 per acre, well above the average 2014 price of $30,000 per acre in the same region.

Now that Clayton Williams will be a part of a larger, more established producer, another 10-bagger performance isn't on the horizon. That said, Noble Energy is one of the better-positioned producers with a robust portfolio of shale assets, as well as a stake in several massive natural gas reservoirs off the coast of Israel. If these can be developed at low costs, it should lead to decent rates of returns for Noble that will drive growth.

10 stocks we like better than Clayton Williams EnergyWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Clayton Williams Energy wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.