15 Reasons to Buy Visa and Never Sell

Image source: Flickr user Hakan Dahlstrom.

This has certainly gone down as one of the wildest years on record for the stock market as a whole. The first two-week period marked the worst performance of U.S. indexes in recorded history. We followed that by staging one of the most voracious quarterly comebacks in decades.

But the smartest investors understand that the best chance they have to generate inflation-topping wealth over the long run is to buy high-quality stocks and hang onto them over the long-term. Based on data from Yardeni Research, the S&P 500 has undergone 35 corrections of at least 10% since 1950, and in each and every instance the index has completely erased the drop. Sure, it can take weeks, months, or even years to recoup losses from a downswing in the stock market, but investors who've held onto companies with solid business models over long periods of time have often outperformed short-term investors who are trying to time the market.

15 reasons to buy Visa and never sell The biggest issue is locating these so-called "high-quality stocks," because they're not exactly something you'll find under every unturned stone. One company that just might fit the bill is payment processing facilitator Visa . In fact, it could be argued that the following 15 reasons to buy Visa may make you never want to sell.

Image source: Flickr user PT Money.

1. High barrier to entry One of the biggest selling points of Visa is that there's well-defined, but minimal competition when it comes to payment process facilitation. Visa,MasterCard, American Express,and Discover Financial Servicesmake up the lion's share of the market, primarily because the cost to lay the groundwork (i.e., infrastructure) can be quite expensive.

2. Leading market share Among the four major credit card networks, Visa is the market share kingpin. In 2014, Visa's $1.2 trillion in purchase volume on its networks was nearly as much as AmEx, MasterCard, and Discover's combined purchase volume ($1.4 trillion). Having the highest market share means it's easily recognizable by consumers and is often the premier choice of merchants and credit cardholders.

3. No lending risk Two of Visa's biggest rivals, American Express and Discover, are able to double-dip -- they earn fees through merchant transactions, but they also act as credit lenders. The downside is when the economy contracts, credit delinquencies often rise, potentially hurting both companies. Visa and its main rival MasterCard have no lending risk, so a rise in delinquencies isn't necessarily a big concern.

4. Geographically diverseThe reason rising delinquencies in one country, such as the U.S., may not be a big concern is that it's very geographically diverse. Visa operates in far more countries than it does not, meaning a slowdown in transactions or gross dollar volume in one country or region can often be mitigated by growth in other parts of the world.

5. Large untapped international marketAccording to MasterCard CFO Martina Hund-Mejean, 85% of global transactions are still being conducted in cash. This means a large untapped opportunity for Visa to expand its business over the coming decades. Regions of opportunity include Africa, the Middle East, and Southeastern Asia.

6. Consistency History may be no guarantee of future results, but it's hard to argue against Visa's growth over the past decade. Revenue has grown by a double-digit percentage in all but two years, and based on Wall Street's estimate of $14.9 billion in revenue this year, Visa will quintuple its top line since 2006 if it manages to hit that mark.

7. Operating margin Because of Visa's commanding market share, its countless merchant partners, and its geographic diversity, its operating margin is among the highest of any megacap companies. Over the trailing 12-month period, Visa's operating margin is nearly 66%, which is more than double the industry average of 28% for credit services. In simpler terms, Visa is getting more bang for its buck.

8. Free cash flow Having a high operating margin also means Visa tends to generate substantial free cash flow, which can further build up its current net cash position. In 2015, Visa generated nearly $6.2 billion in FCF, which allows it the flexibility to boost shareholder yield or take on other business ventures (which we'll get to shortly).

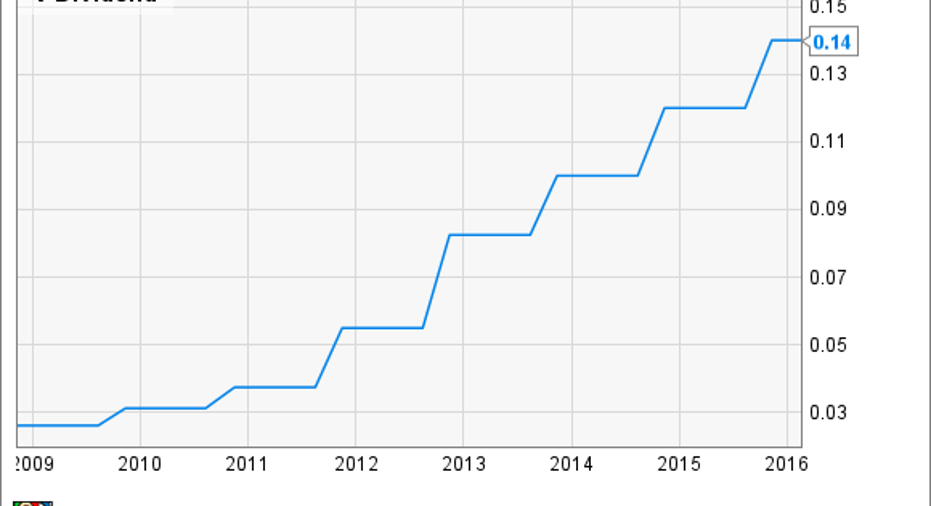

9. Dividend growthA good example of what solid FCF generation can do can be seen in Visa's dividend growth since 2008, when it first introduced a quarterly stipend. Adjusted for its split, Visa had been paying just under $0.03 per quarter. Today, Visa is paying $0.14 per quarter, meaning it almost quintupled in a span of eight years.

10. Payout ratioVisa's current yield of 0.7% may not seem like much to write home about, but its payout ratio is suggestive that there's plenty of room for it to become a dividend juggernaut of the future. Based on the $2.80 it's expected to earn in full-year EPS, this year's payout ratio is a mere 20%. Most Dow Jones Industrial Average components typically target payouts or around 50% or even higher, so I'd anticipate consistently strong dividend growth moving forward.

11. Share buybacks On top of rewarding its investors with a money-in-hand dividend policy, Visa is also very active when it comes to repurchasing its own common stock. Last year, Visa's board authorized a $5 billion share repurchase agreement. Buying back stock reduces the number of shares outstanding, thus boosting EPS and possibly improving the attractiveness of Visa's valuation. Since 2010, Visa has retired nearly a fifth of its outstanding shares as a result of buybacks.

12. Extended low-yield environmentIt may be intangible, but the extended low-yield environment perpetuated by an accommodative Federal Reserve, as well as other developed countries around the world, some of which have adopted negative interest rate policies, has encouraged consumers to reach into their pockets and make big dollar purchases. A long-spanning, low-yield environment is great news for credit-based transactions.

Image source: Flickr user Nguyen Hung Vu.

13. Partnerships Visa's high margins and solid FCF also allow it to partner up with smaller payment technology companies that could be sitting on stellar ideas. In July of last year Visa announced a partnership with Stripe that saw Visa make a direct investment in the online and mobile-based payment solutions company. On one hand, Stripe gets access to Visa's expansive merchant network in overseas markets, while Visa gains access to new merchant payment experiences that could enhance its current payment solutions portfolio.

14. Inorganic growth On top of partnerships, Visa also supplements its organic growth with acquisitions. Earlier this year Visa gobbled up a 10% stake in rival Square, but the game-changer could be its purchase of former subsidiary Visa Europe for around $23 billion. This move should allow Visa to cut expenses long-term and boost fees over in Europe, further boosting FCF, operating margin, and profits.

15. Institutional ownershipLastly, we see that a whopping 93% of Visa's float is held by institutions and mutual funds. Although big money isn't always right, it's worth noting that nearly 1,500 institutions and money managers believe Visa will be worth more at some point in the future than it is now.

Is there a key point I missed that'd entice you to buy Visa and never sell? Share it in the comments below.

The article 15 Reasons to Buy Visa and Never Sell originally appeared on Fool.com.

Sean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool owns shares of and recommends MasterCard and Visa. It also recommends American Express. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.