1 Reason Wells Fargo Recovers So Quickly From Financial Crises

One Wells Fargo Center in Charlotte, North Carolina. Image source: iStock/Thinkstock.

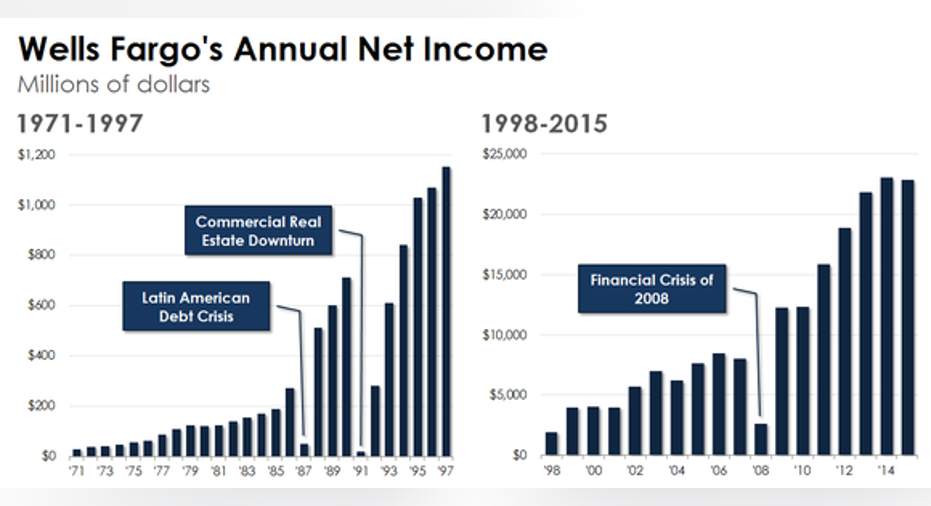

There are three periods in Wells Fargo's past that shine a revealing light on its approach to banking:

- The Latin American debt crisis of the mid- to late 1980s

- The recession and commercial real estate downturn in the early 1990s, and

- The financial crisis of 2008

Although none of these crises caused Wells Fargo to record an annual loss -- which distinguishes it from many other banks -- they all had a meaningful impact on its bottom line. The chart below illustrates this, which traces Wells Fargo's yearly earnings since 1971.

Data source: Wells Fargo's annual reports. Chart by author.

As you can see, Wells Fargo's profits dropped precipitously in 1987, 1991, and 2008. The reason in each of the cases was the same: higher loan loss provisions.

- In 1987, Wells Fargo set aside an extra $589 million to cover expected losses from its portfolio of Latin American loans.

- It boosted its loan loss provisions by more than $1 billion in 1991 to buffer it against the downturn in commercial real estate.

- And the drop in Wells Fargo's earnings in 2008 stemmed principally from its $16 billion provision tied to the housing downturn as well as its acquisition that year of Wachovia.

This is not unusual. Even the best-run banks suffer loan losses. One could argue in fact that every bank should make some bad loans; otherwise, they're not being aggressive enough on the sales front. The key is to minimize losses and to respond to them immediately and aggressively when they do materialize.

Wells Fargo's experience serves as a case in point. With the benefit of hindsight, it's clear that the California-based bank has consistently set aside more money at the beginning of crises than it ended up using to absorb losses during the crises.

- From 1987 to 1990, it recorded $1.9 billion in loan losses provisions but charged off only $998 million worth of loans.

- From 1991-1993, it set aside $3.1 billion but charged off only $1.9 billion worth.

- And from 2007-2009, it recorded $42.6 billion in provisions versus $29.5 billion in net charge-offs.

The impact of setting aside more money than it needs is twofold. First, it means that Wells Fargo's profit in the first year of a crisis will bear the brunt of any losses that materialize during the crisis. And, second, it means that the bank can later boost its profit by releasing unused provisions.

Wells Fargo did so from 1994 to 1999, during which its charge-offs exceeded its provisions every year, meaning that it released money from its loan loss reserves. And it's done so every year since 2010. In 2011, for instance, Wells Fargo's provisions added up to $7.9 billion while its net charge-offs amounted to $11.3 billion.

The net result is that not only can investors in Wells Fargo assume that it will be better equipped to survive crises, on account of its aggressive approach to loan loss provisions, but also that it will recover more quickly, as it benefits in subsequent years from reserve releases.

The article 1 Reason Wells Fargo Recovers So Quickly From Financial Crises originally appeared on Fool.com.

John Maxfield owns shares of Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.