1 Reason Bank of America Could Soon Earn a Lot More Money

Bank of America's headquarters in Charlotte, North Carolina. Image source: iStock/Thinkstock.

Here's a question that should be at the forefront of every bank investor's mind right now: If President-elect Donald Trump follows through on his promise to "dismantle" the Dodd-Frank Act, and is able to actually do so, what would that mean for banks -- and, for our purposes here, Bank of America (NYSE: BAC) in particular?

Ignoring the question of whether this is good or bad for the stability of the financial system, I think it's pretty clear that rolling back Dodd-Frank could unleash a wave of profits for banks. The most potent impact would come from loosening up bank capital and liquidity requirements.

Heightened liquidity standards

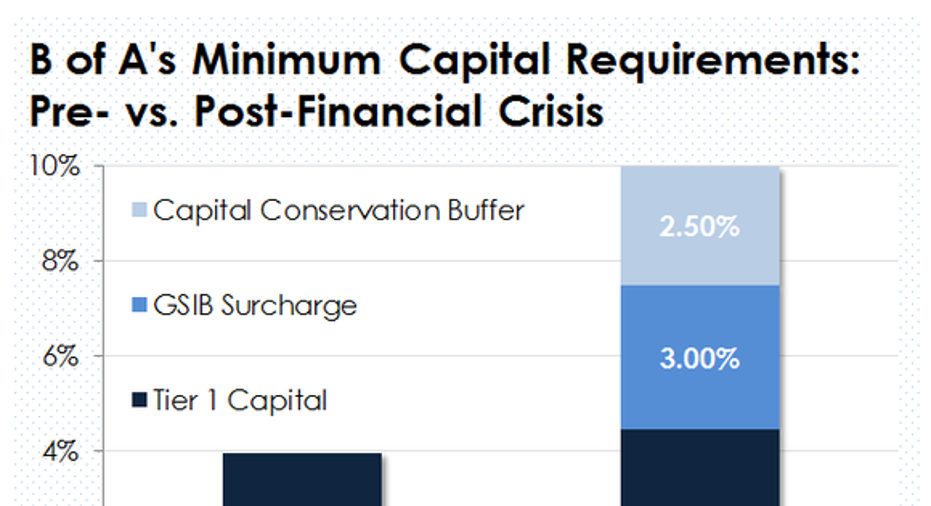

Under regulations passed pursuant to Dodd-Frank, banks now have to hold substantially more capital than they did before the 2008 financial crisis. Bank of America, for instance, used to face a Tier 1 capital ratio of 4%. That figure now is 10% -- or at least it will be once the post-crisis standards are fully phased in.

Data source: Bank of America. Chart by author.

Perhaps even more significant for banks, is the requirement that they allocate a larger portion of their assets to things like cash and highly liquid government securities, as opposed to loans. The thought process behind the elevated liquidity standard is that it will help banks avert failure in the event of a bank run, similar to what brought down Bear Stearns and Washington Mutual in 2008.

The problem at Bear Stearns, wasn't that it didn't have enough capital -- it did. The problem was that, when depositors sought to withdraw their funds en masse, the investment bank couldn't convert its less liquid assets into cash quickly enough to satisfy the onslaught of withdrawal requests. It was illiquidity and not insolvency, in other words, that led to Bear's downfall.

You don't have to look far to see how much liquidity banks now hold on their balance sheets. JPMorgan Chase leads the way in this regard with $539 billion worth of high-quality liquid assets. And Bank of America isn't far behind, with $522 billion worth of so-called "global liquidity sources" as of the end of the third quarter.

What exactly are these? According to Bank of America's third-quarter earnings release, they consist of:

This is obviously great from a safety and soundness perspective. But it's horrible for Bank of America's bottom line.The average annualized yield on Bank of America's highly liquid assets is something like 1.5%. Meanwhile, the annualized yield on its less liquid loan portfolio last quarter was 3.72%.

If you do the math, this means that Bank of America would earn an added $550 million a quarter in interest income for every $100 billion worth of low-yielding liquid assets that it reallocates to higher-yielding loans. That translates into 10% or so of its quarterly profits. That's a rough estimate, but you get the point.

Will liquidity standards be eased?

We don't know that the incoming administration will do this. For that matter, given the scant amount of policy details that Trump's team has shared publicly, they probably don't know either.

But what we can say is that Texas Rep. Jeb Hensarling, a close ally of Vice President-elect Mike Pence, is promoting this by way of the proposed Financial CHOICE Act. As the website for the Act notes (emphasis added):

And with respect to connecting the dots between Hensarling and Pence, here's The Wall Street Journal:

At the end of the day, while it remains to be seen what the Trump administration, together with Republicans in Congress, actually do about banking regulations, it isn't unreasonable to think that their approach, for better or for worse, will consist of loosening capital and liquidity standards and thus make it easier for banks to earn more money.

Forget the 2016 Election: 10 stocks we like better than Bank of America Donald Trump was just elected president, and volatility is up. But here's why you should ignore the election:

Investing geniuses Tom and David Gardner have spent a long time beating the market no matter who's in the White House. In fact, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of November 7, 2016

John Maxfield owns shares of Bank of America. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.