1 Major Concern Facing These 3 Stocks

What's on your list of concerns today? Is it President Donald Trump, who keeps many executives awake at night at the risk of being the next victim of a tweet? Are you concerned that Tom Brady is about to potentially win his fifth ring? Are you concerned about the timing of the Federal Reserve's rate hikes? Whatever happens to top your list of concerns, it probably isn't used car prices -- but if you own stock inFord Motor Company(NYSE: F)TrueCar(NASDAQ: TRUE)orCarMax(NYSE: KMX), it should.

Image source: Getty Images.

Used car prices, really?

Let me explain. There's been a small phenomenon taking place since the Great Recession. As financing became extremely cheap, to encourage economic growth, consumers were able to purchase more bang for their buck on big-ticket items such as vehicles. That scenario played out at the same time vehicles became more connected and packed with technology, which increased the price tag. Consumers did a couple of things to help offset the increased price: extended their loan length, or leased vehicles. The first issue, extended loan lengths, is an article in itself for another day, but the latter is an issue worth discussing now.

The total number of vehicles that came off-lease during 2015 was 2.3 million units, which increased during 2016 to 3.1 million. This year J.D. Power & Associates estimates 3.4 million vehicles will come off-lease, and that figure jumps to 3.7 million during 2018. The accelerated rate of vehicles coming off-lease has flooded the used-car market, driving prices down. For context, the total used-vehicle supply totaled 11.9 million in 2015 and is estimated to balloon to 14.5 million during 2018. Here's a glance at what it's doing to industry auction values.

Image source: Ford analyst presentation.

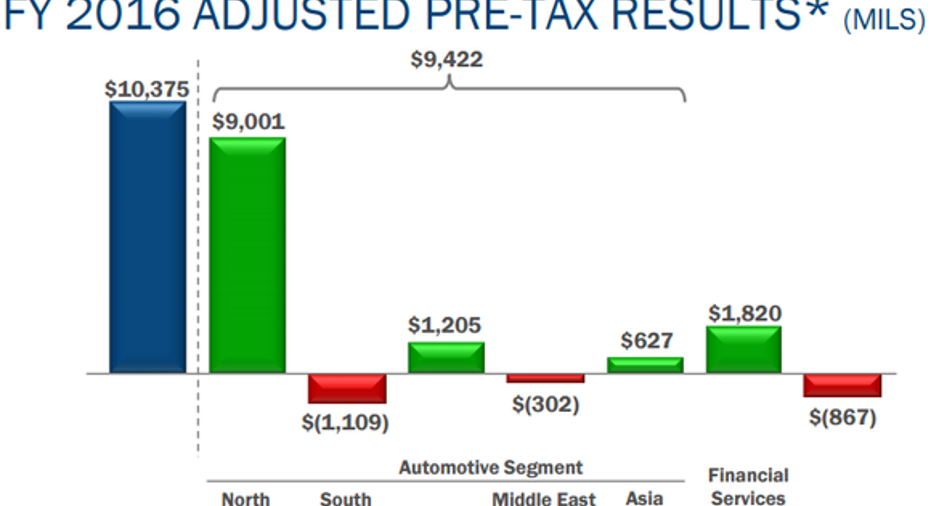

Why does this concern investors? Let's break it down by each of the three companies mentioned. For Ford, it's pretty simple: Its second most profitable entity outside North America is Ford Credit.

Image source: Ford Motor Company Q4 presentation.

Residual pain

Ford Credit is the company's finance division, which, among other things, helps consumers purchase and lease vehicles. When Ford Credit leases a vehicle, it's forced to assume a value for the vehicle when it's due to be returned. If the residual value of vehicles declines more rapidly than anticipated, as has happened over the past year, the company faces immense bottom-line pressure. Ford Credit's pre-tax profits were 28% lower during the fourth quarter, compared with a 10% decline during the full year 2016, suggesting the residual value declines are intensifying.

In large part because residual values are declining, Ford Credit has guided for full-year 2017 pre-tax profits to check in at $1.5 billion, a significant step back from its $1.9 billion result during 2016 and $2.1 billion during 2015. To be fair, this issue is more of a near-term hurdle, and the company can offset weaker prices by relying less on lease sales as well as offering extended warranties on its certified used vehicles, which helps support prices.

Top-line pressure

For CarMax, it's a different story, because a decline in used-car prices means it has less margin of error to work with taking its top-line revenue down to its bottom-line profit. Unlike Ford, CarMax's business revolves around sales of used cars, and when those decline, it puts immediate pressure on its entire business. Unfortunately for investors, CarMax's average used-car transaction prices have plateaued recently, and that could even reverse as more off-lease vehicles flood the market.

Image source: CarMax's FY Q3 presentation.

To offset a decline in used-car prices, CarMax will have to make its operations more cost effective, expand its store count, and, perhaps, offer fewer discounts or incentives on purchases. Investors would be wise to watch how management plans to deal with this scenario going forward. Through 2015, CarMax had the best of both worlds, as its sales were increasing in price and it was opening new stores, which added incremental sales. Now, part of that story will slow, and that could alter investors' thesis on the stock.

Cheap substitute products are bad news

TrueCar's issue is also different from either Ford or CarMax. TrueCar acts as a middleman between consumers looking for information and a way to finish part of a purchase online at home, rather than spending time haggling at a dealership, and dealers looking for easier-to-close sales leads. Dealers pay TrueCar for consumers very near the end of a purchase cycle, which is often cheaper than typical advertising or marketing. Consumers get immense and detailed vehicle information and pricing in return, and in theory, everybody wins.

The issue going forward is that TrueCar generates a vast majority of its profits from new-vehicle sales, which already face slower growth as new-vehicle sales plateau in the U.S. market, and could face even more pressure as used vehicles -- a cheaper substitute to new vehicles -- decline in price. If consumers begin opting to purchase increasingly cheaper used vehicles rather than new vehicles, TrueCar will have to adjust its business model accordingly.

Ultimately, these scenarios aren't apocalyptic developments for any of these three companies, but savvy investors should absolutely put used-car prices near the top of their concern list, and few even have it on their list at all.

10 stocks we like better than TrueCar When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and TrueCar wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Daniel Miller owns shares of Ford. The Motley Fool owns shares of and recommends CarMax and Ford. The Motley Fool recommends TrueCar. The Motley Fool has a disclosure policy.