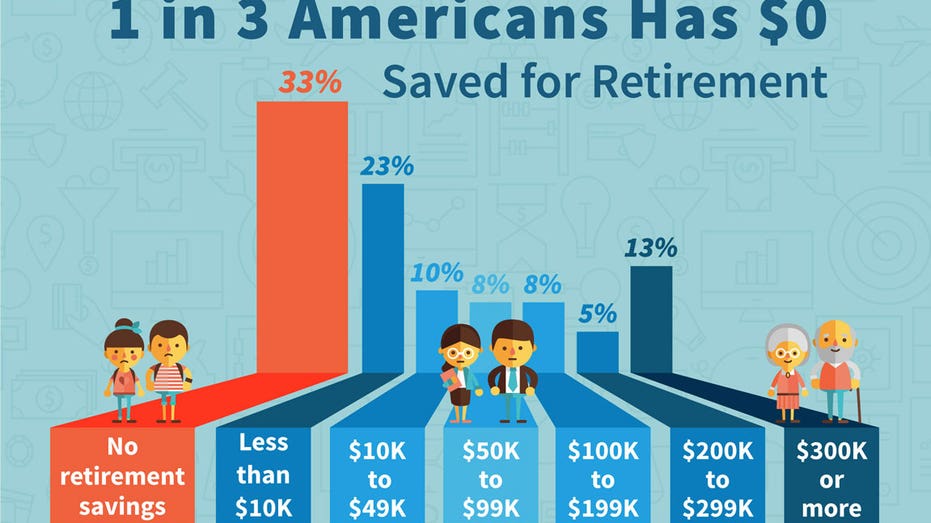

One in Three Americans Have Nothing Saved for Retirement

Nothing was more important to Winnie than her young children. The married mother of three took care of their needs but seldom took care of her own. As Winnie neared retirement, she divorced her spouse without a pension, 401-k or any significant savings. Because of an illness, she was forced to retire early and take reduced Social Security benefits. Her story is not uncommon.

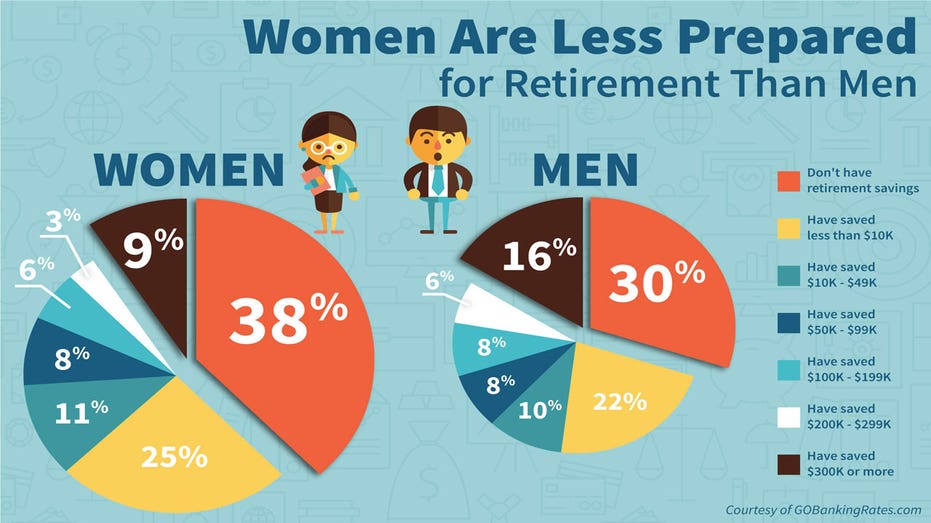

Winnie is my mother. A study by GOBankingRates.com found that one in three Americans has nothing saved for retirement. Women are 27% more likely than men to have no retirement savings.

Experts say everyone should start preparing for the future as soon as possible.

“A young person starting their first job is thinking - retirement is 40 years in the future and I can deal with that later,” says John Sweeney, Executive Vice President of Retirement and Investing Strategies at Fidelity. “That’s exactly the time to set up a disciplined savings process and let that money compound over their 40-year working career.”

Workers should contribute enough to their job’s retirement plan to get their employer’s full matching contribution – if one is offered.

“That’s the closest thing to free money and a great way to grow your retirement savings,” says Cameron Huddleston, Life & Money columnist at GOBankingRates.com. “Even small amounts contributed monthly can add up to hundreds of thousands of dollars by the time they retire.”

Calculate how much of a nest egg you will need to live comfortably. Take into account health care costs - which may rise as you get older. The Department of Labor says the average American spends roughly 20 years in retirement. Fidelity, Vanguard and other investment firms offer free online retirement calculators.

“Savers are looking between 70 and 80% income replacement in retirement,” Fredrik Axsater, Head of Defined Contribution Retirement for State Street Global Advisors. “In order to get there, we need to think of an overall savings rate of 15 to 20% of our paychecks.”

If your company offers a traditional pension plan, check if you’re covered. An Individual Retirement Account (IRA) may also be an option. An IRA allows an individual to save for retirement with tax-free growth or on a tax-deferred basis.

Social Security may also play a key role in your retirement plan. But keep in mind: Social Security only replaces about 40% of pre-retirement earnings for the average American worker. Review your options at www.ssa.gov.

Northwestern Mutual says a majority of Americans expect to begin taking Social Security between the ages of 65-67. Angela DiCastri, Director of Retirement Markets at Northwestern Mutual says consumers should take into account their savings/investments, current/future earnings, health, taxable income and family situation when deciding when to collect Social Security.

“Make sure you are getting the most you can based on your circumstances and what makes the most sense you as an individual or a couple. That’s something many consumers are overlooking and potentially leaving a significant amount of dollars on the table.”

This is the second in a series of articles that will appear weekly during April; National Financial Literacy month.

Linda Bell joined FOX Business Network (FBN) in September 2014 as an Assignment Editor after more than a decade at Bloomberg News. She is an award-winning journalist/writer of personal finance content. Follow her on Twitter @lindanbell.