Grading ObamaCare, Week 1: Incomplete

The Affordable Care Act’s health insurance exchanges made their long-awaited debut this week, kicking off open enrollment on the same day the federal government went into shutdown mode. And while opponents of the law may be quick to judge the law’s success or failure, numbers are lacking with experts say if they were to grade the law’s first week, it would be “incomplete.”

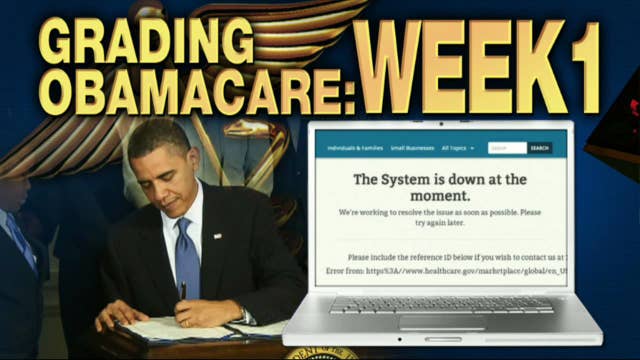

The administration has remained tight-lipped on divulging exact numbers as to how many people have signed up for coverage on the exchanges, but anecdotal reports have been heavily weighted with tales of glitches and inaccessibility to enroll. The Department of Health and Human Services (HHS) said 2.8 million people visited Healthcare.gov on its first day live, but declined to say how many people successfully enrolled in an insurance plan.

Devon Herrick, senior analyst at the National Center for Policy Analysis, says the administration has been extremely aggressive in promoting the exchanges, holding nationwide rallies and enlisting celebrities to raise awareness and urging people to sign up for coverage—specifically young people.

“The idea was to get the ‘young invincibles’ into the market,” Herrick says. “The administration really needs this, it’s the cornerstone of the Affordable Care Act and they really need it to work.”

The federal health exchange, which is operating in 36 states, wasn’t operating as efficiently due to the amount of people visiting in large volumes. President Obama likened the glitches to what happens when major companies like Apple (NASDAQ:AAPL) roll out a new product.

“They didn’t have the capacity online, but that doesn’t mean insurance won’t sell,” Herrick says. “The Department of Health and Human Services won’t release any figures, but it appears to be more a trickle than a flood for the first week of open enrollment.”

States that operate on their own exchanges seemed to fare better in getting people online, according to reports, Herrick says.

“Kentucky, for example, seemed to go pretty well,” Herrick says. “But they tested this in advance, so it was ready and it seemed to work. Some others, not as much—and in states like Texas and Florida [with higher populations] that’s more of a headache, so it makes sense.”

Susan Dentzer, senior policy advisor to the Robert Wood Johnson Foundation, says the federal exchange experienced more glitches than many expected, but individual state exchanges did better than predicted.

“This is not ‘glitch-free’ by any means,” Dentzer says. “But given the enormity of the task, it’s not unexpected. In a perfect world, they would have been finding this out through testing six months ago.”

Herrick agrees, adding the government’s plan was simply just too ambitious, and should have been tested one piece at a time.

But for Larry Kocot, visiting fellow at the Brookings Institution, its way to soon to pass judgment on how well the rollout fared. He says there has been too much emphasis on numbers.

“I’d give this an incomplete,” Kocot says. “You can’t really evaluate in week one. We anticipated a lot of technical problems, as you have with any new programs as soon as someone flips the switch. But I don’t think you can infer anything about open enrollment based on how many hits there were on a website.”

Enrollment completion can be judged once individuals actually pay for their premiums, Kocot says.

“The process isn’t over until someone pays a monthly premium, and that is the question people should be asking—how many people actually completed the enrollment process and are in a plan?”

But the open enrollment period still has nearly six months to go, ending on March 31, 2014, and coverage purchased on these exchanges won’t kick in until the New Year, so many may wait until mid-December to actually sign up, he says.

Dentzer agrees it’s too premature to grade the rollout. And glitches aside, she says the volume is positive.

“It shows a lot of people are aware of these exchanges, and if the test is whether or not Americans are interested, the answer is yes,” she says.