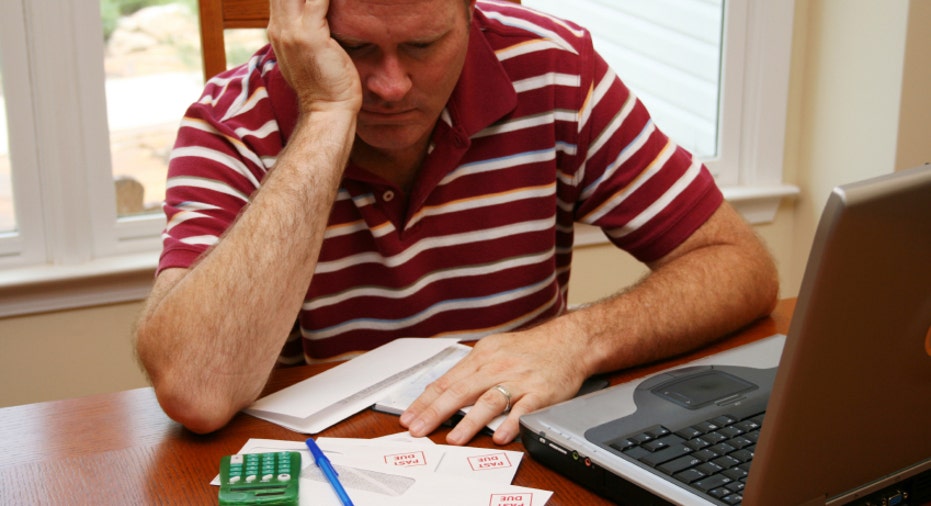

Can't Pay Your Taxes? 10 Steps to Take Now

If you’ve just finished filing your taxes and can’t afford the amount you owe Uncle Sam, don’t panic -- you have some options.

“The best tax planning is to always owe something to the government," says Mike Robbins, CPA and principal-in-charge of the tax department at Rehmann.“People wrongfully think that a refund is the government giving them free money. There’s no such thing. It’s actually them giving you your money back that you just loaned them tax free.”

Upper-income filers are facing higher taxes this year due to taxes associated with the Affordable Care Act, but tax experts say it’s common for individuals to be surprised when they have to cut the IRS a check.

If it comes down to paying your mortgage or credit card bill or the IRS, Stephen DeFilippis, an enrolled agent at DeFilippis Financial Group, recommends choosing the latter. “You don’t want to have the IRS as a creditor. They have a lot of power: they can garnish wages, levy bank accounts and put liens on properties.”

Filers have a variety of options if they can’t afford their tax bill, but experts agree the key is taking action.

File Anyway. Even if you can’t afford the bill, file your tax return, advises Laura Blasberg, tax attorney and partner at Meltzer, Lippe, Goldstein & Breitstone in New York. “The penalties for not filing are 10 times as much for not paying. You can get the penalties removed pretty easily for not paying on time, but the IRS almost never removes charges for not filing on time.”

Keep in mind that if you file an extension, you will only be granted more time to file the return, not pay the bill.

Re-evaluate Your Withholdings. Robbins says owing money to the IRS is normally a sign of the wrong number of withholdings on a W-4. Employers deduct taxes based on the allowances on this form; if you have too little withheld, you will most likely end up owing the IRS money.

Robbins recommends reading the form’s instructions carefully. “Mistakes on W-4s are common because employees don’t get a lot of guidance from employers on how to fill them out. Use the worksheet and plug in your information to get the proper withholding exemptions to avoid tax day surprises.”

Pay What You Can. If you can’t afford the entire bill, pay what you can.

“Even if you make a partial payment, let’s say you owe $4,000 and you pay $1,000, that will limit the interest and failure to pay penalty that you will get hit with,” says DeFilippis.

Sell Assets. If you don’t have the funds sitting in your bank account to cover your tax bill, Robbins says it’s time to evaluate your discretionary assets. “Do you have a boat, art, a vacation cottage, stocks or any other tangible asset that you can sell?”

Work with the IRS. The IRS offers repayment plans, so don’t be afraid to reach out. “If you approach them, they will generally work with you, but you need to give them the chance to work with you and find the right plan,” says Blasberg.

The IRS offers installment programs that allow you to set up monthly payment plans to pay down the debt. If you owe less than $50,000 you can apply online, if you owe more than that, you must submit Form 433-A. The maximum term for an installment agreement is 72 months, and there are fees for setting up the agreement.

The IRS also has Offers in Compromise plans, but DeFilippis says this option is only for extreme situations. “You must prove not only do you not have the ability to pay now, but you won’t have the ability to pay in the future.” There is a statute of limitations that limits the IRS from collecting owed taxes that have been outstanding for more than 10 years. “They will weigh their chances of whether they will ever be able to collect what is owed. If it looks extremely unlikely, then they will take a percentage since it’s better than nothing. “

When calling the IRS, Blasberg warns to set a lot of time aside. “Plan to be on the phone and on hold with the IRS for at least an hour. This isn’t something you can do walking out the door.” She also recommends having the appropriate financial documents including bank account statements, paycheck stubs, asset information and bills readily available.

Put it on Plastic. Putting the bill on a credit card only makes sense when the interest rate on the card is lower than the IRS’ penalty. "Sometimes you can get a deal with a 0% interest rate for a set period of time, which is smaller than the interest and failure to pay penalty coming from the IRS. If you can pay off the debt in that period, it’s not a bad option,” says DeFilippis.

He adds that some companies do not allow users to charge their tax bill, and that you must go through one of the IRS’ approved e-pay service providers.

Ask Family Members for Help. If a family member is willing to loan you the money, the experts all agree to put the loan terms in writing.

Robbins adds that the IRS doesn’t allow loans to be made at below-market rates, a number it publishes every month. “Under normal circumstances, it’s likely they won’t know you got an interest-free loan, but if you get audited, it could come up and you are in more hot water.”

Tap Your Home Equity Line. DeFilippis says if you have a home equity line of credit available, it might make financial sense to tap it. “The one benefit there is that if the amount of credit line you borrow is under $100,000, you can deduct the interest on home equity debt.”

Consider Borrowing from Your 401(k). If you are younger than retirement age (59 ½ ) any funds taken out of your 401(k) will be taxable and hit with a 10% penalty. “The interest on installment agreements could be less,” says Robbins. “When you see people rob their 401(k) for their tax situation, that often means their retirement is going to be cut short since they often don’t put the money back. If you take this route, you better pay it back.”

Blasberg says borrowing from a 401(k) can be a much better option. “If you borrow from your account, you are paying interest to yourself and it doesn’t show up on your credit report.”

Be Watchful of Scams. Radio and TV are filled with “tax professionals” claiming they can reduce the amount you owe to the IRS to pennies on the dollar, but Blasberg warns to be leery of professional making promises that sound too good to be true.

“People panic and they are just looking for any help, but you need to take a step back and do your homework and research a company and its workers before committing to work with them,” she says.