Housing affordability unlikely to return to more favorable levels of the past, economist says

About 70% of existing homeowners hold mortgage rates below 5%, freezing turnover to its lowest level in roughly 40 years

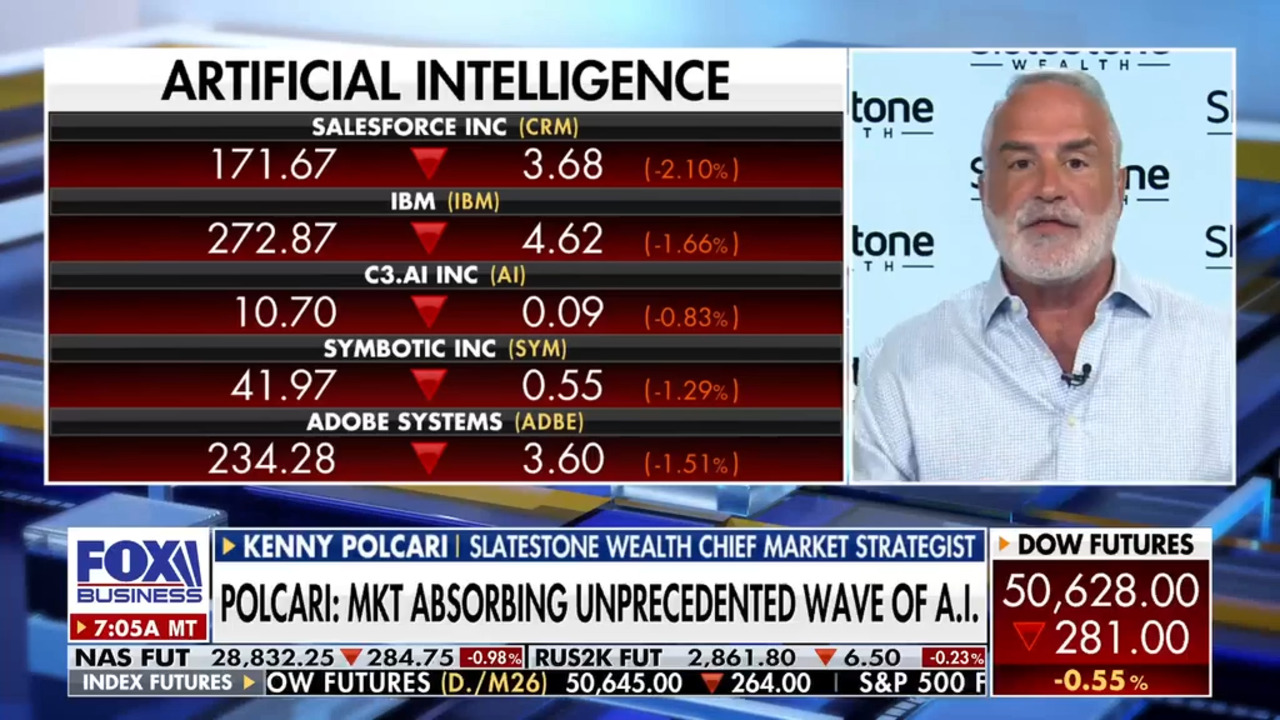

Investors should never be dependent on one sector or theme, Kenny Polcari says

SlateStone Wealth chief market strategist Kenny Polcari discusses whether investors are too dependent on AI, Space X's IPO and his outlook for the markets on 'Varney & Co.'

The affordability of the U.S. housing market may not improve significantly over time for would-be homebuyers, with a new report suggesting that they shouldn't wait in the hopes of affordability measures returning to their pre-2022 levels.

Sarah Wolfe, a senior economist and strategist at Morgan Stanley, said in a report that while housing affordability could improve modestly over time, it is "unlikely to return to more favorable levels of the past, as the market adjusts to a higher-cost, tighter-supply environment."

Wolfe noted that there was a brief period of optimism in February when mortgage rates briefly dipped below 6%, but it was short-lived as they returned to around 6.5% and have remained over 6% since then – which sapped the potential momentum for the housing market before it could gather steam.

"That recent episode is telling. In today's market, small changes in rates have outsized effects on affordability, which remains historically strained, due in part to this rate-sensitivity," Wolfe wrote.

INCOME NEEDED TO AFFORD A MEDIAN-PRICED HOME HAS NEARLY DOUBLED SINCE 2020, REPORT FINDS

Housing turnover has slowed significantly amid higher mortgage rates, Morgan Stanley noted. (Daniel Acker/Bloomberg via Getty Images)

She said that in looking at the housing market from 1990 to 2021, it was less affordable than it currently is about 15% of the time.

That implies that even modest improvements in the affordability of the current housing market would be considered tight in comparison to prior cycles in the last few decades.

To illustrate the present affordability challenges, an estimate by Morgan Stanley Research found that the buyer of a median-priced home faces a monthly payment of about $2,000 – which is roughly double the carrying cost from five years ago.

MIDWEST AND SOUTHERN STATES DOMINATE HOUSING REPORT CARDS: SEE HOW YOURS SCORED

The housing sector may not return to pre-2022 affordability levels, Morgan Stanley's analysis found. (Angus Mordant/Bloomberg via Getty Images)

Homeowners who have lower interest rates on their mortgages have been reluctant to sell and take on a new mortgage with a higher interest rate, which has exacerbated affordability for new buyers.

"The jump in financing costs is also freezing sellers. Of existing homeowners, about 70% have mortgage rates below 5%, and one-half have rates below 4%. These homeowners often find it too costly to move and take on a new mortgage at current higher rates. The result is a collapse in housing turnover to the lowest level in roughly 40 years," Wolfe said.

Due to the lack of turnover in the market for existing homes, new construction has played an increasingly important role on the supply side of the housing market. The report notes that the pace of price appreciation has slowed in some areas and scarcity has been persistent in others, with supply not improving fast enough to "meaningfully lower the barrier to entry."

MEDIAN US HOME PRICE PROJECTED TO HIT $1 MILLION BY 2050 – RIGHT AS MILLENNIALS RETIRE

New home construction is helping support housing market supply, but isn't occurring fast enough to significantly improve affordability. (David Paul Morris/Bloomberg via Getty Images)

The affordability challenges in the housing market have also contributed to changes in the characteristics of first-time homebuyers. While the average age remains around 36, the average credit score has risen to 734 from 718 in 2019.

First-time homebuyers are also carrying larger mortgage balances, which rose to an average of $334,000 in 2024 – an increase from $240,000 in 2019 and $195,000 in 2014. That growth has outpaced inflation by more than two-fold, the report noted, while buyers have also shifted to more affordable zip codes to buy their first home.

Wolfe went on to say that there could be some modest improvement in housing affordability when rates stabilize and the pace of home price growth eases, with the firm projecting rates will moderate to around 5%, lowering mortgage payments from about 24% of household income to about 21% in the next decade – though that remains above the 15% that followed the 2007-2009 financial crisis.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

"In all of the scenarios that Morgan Stanley Wealth Management modeled – whether mortgage rates settle closer to 4%, 5% or 6% – affordability does not return to prior peaks. And the likelihood of mortgage rates settling closer to 6% than 5% has been rising," Wolfe wrote. "In short, the market is not broken, but it is resetting to a more constrained equilibrium."

Wolfe added that "waiting on the sidelines for prices to revert to the affordability of the two decades before 2022 may prove to be the wrong strategy. The better approach may instead be to buy when it makes sense for your financial situation – and when the right opportunity presents itself."