Credit card debt is surging at a record-high rate, NY Fed reports

Here's how to pay off credit card debt and potentially save money

If you're just making the minimum payments on your credit cards, it may be worthwhile to consider one of these debt repayment strategies. (iStock)

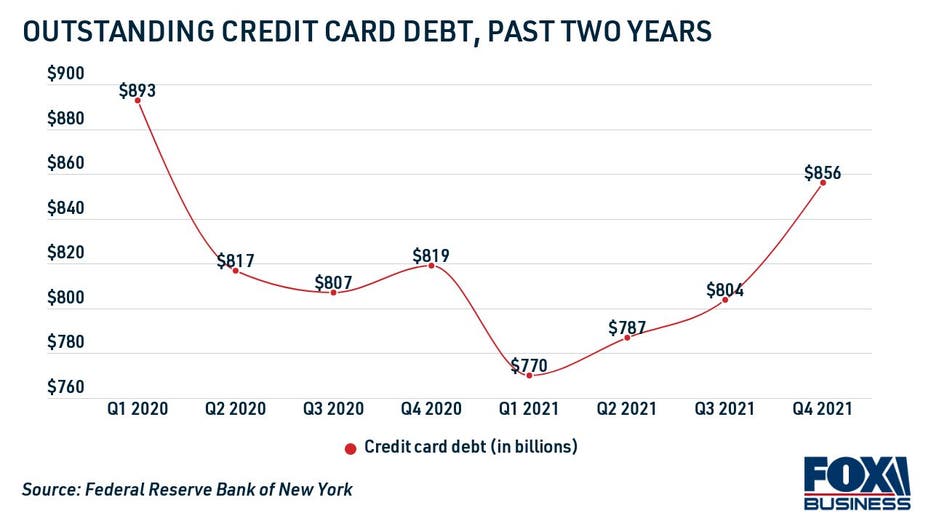

Americans are racking up credit card debt at a record-setting pace, according to the Federal Reserve Bank of New York.

Credit card balances grew to $856 billion in the fourth quarter of 2021, up $52 billion (6.5%) from the previous quarter. That's the largest quarterly increase observed since the NY Fed began collecting this data 22 years ago.

Outstanding credit card debt is still about 7.7% lower than it was at the end of 2019, when it hit an all-time high of $927 billion. That's because consumers paid down their credit card balances at the onset of the coronavirus pandemic — although they now appear to be resuming pre-pandemic spending habits.

If you're struggling to repay high-interest credit card debt, keep reading to learn about three strategies that could help you get out of debt fast. You can also compare a variety of financial products, from balance transfer cards to debt consolidation loans, on Credible's online marketplace.

DEBT SNOWBALL METHOD VS. DEBT AVALANCHE: WHAT'S THE DIFFERENCE?

3 ways to get out of credit card debt

If you're among the millions of American consumers who added to their credit card balances at the end of 2021, you may be looking for ways to pay off your debt. Here are three debt repayment strategies that can help you slash your credit card balances fast:

Read more about each method for paying off credit card debt in the sections below.

1. Nonprofit credit counseling

Credit counseling agencies offer free or low-cost debt relief services to consumers who are struggling to manage their finances. A credit counselor may help you by:

- Analyzing your income, expenses and outstanding debts to create a budget

- Negotiating with creditors to lower your interest rates and waive fees

- Signing you up for a debt management plan (DMP)

Under a DMP, a nonprofit credit counselor will work with your creditors on your behalf to consolidate your debts into a single monthly payment. Enrolling in a DMP typically comes with a monthly fee, which may be waived or lowered depending on your financial situation.

You can find a certified credit counselor through trade groups like the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). You can also see a full list of accredited nonprofit credit counseling agencies on the Department of Justice website.

BEST CREDIT CARD CONSOLIDATION LOANS

2. Balance transfer cards

While credit counseling may be the preferred option for debtors with fair or bad credit, consumers with good credit can consider alternative debt repayment methods like credit card balance transfers.

A balance transfer is when you move your current credit card debt to a new account with better terms, such as a lower interest rate. You may be able to transfer the balance of one or more credit cards onto a single card using this method, although you may have to pay a balance transfer fee of 3-5% of the total amount.

As an added bonus, some credit card companies offer introductory 0% APR periods for balance transfers, which would effectively allow applicants to avoid paying interest on their credit card debt for that period of time. These offers typically last up to 18 months and are reserved for borrowers with very good to excellent credit, defined by the FICO model as a credit score of 740 or higher.

You can compare balance transfer credit cards, including ones with zero-interest offers, for free by visiting Credible.

BANKRUPTCY FILINGS CONTINUE TO DECLINE DESPITE SKYROCKETING CREDIT BALANCES

3. Debt consolidation loans

Debt consolidation loans are another popular way to pay off credit card balances. A debt consolidation loan is a type of unsecured, lump-sum personal loan that's repaid in monthly installments at a fixed interest rate.

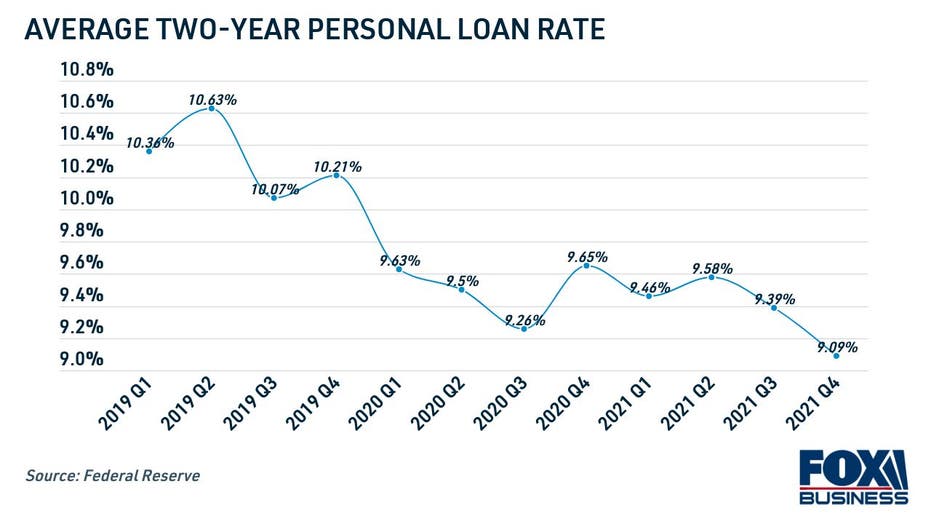

The average rate on a two-year personal loan is 9.09%, according to the Federal Reserve. This is the lowest that personal loan rates have been in the history of the Fed's data. In comparison, the average credit card interest rate is 16.44%.

Thanks to lower interest rates and a consistent repayment schedule, credit card consolidation can save some borrowers thousands of dollars over time. Applicants with a good credit score will qualify for the lowest personal loan rates available, but debt consolidation loans may not be worthwhile for borrowers with bad or fair credit.

Personal loan interest rates can vary from one lender to another, so it's important to compare multiple offers if you're considering debt consolidation. You can browse current personal loan rates in the table below, and visit Credible to compare offers across multiple personal loan lenders at once without impacting your credit score.

WILL A NEW CREDIT CARD AFFECT MY MORTGAGE APPLICATION?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.