Is Recession Looming: Depends on Who You Ask

During times of extreme volatility in the stock market and growing global economic fears, retail investors tend to want to pull their money out of the market, sell everything, and call it quits. But often, the ones who win the most are those who stay put and buy low.

“There’s a common impression that volatility is a call to action, but I would say nothing could be further from the truth,” Doug Sandler, chief equity officer at RiverFront Investment Group, said. “Volatility is the worst time to react.”

He said retail investors have perhaps the biggest advantage since their hands aren’t tied with levered positions, which are investments made using borrowed capital.

“There’s no reason mom and dad have to feel like they have to jump into the middle of the shark tank,” he said.

His best advice: Hold still until the volatility subsides, and if you feel like it, buy a few good names at a big discount to add to your portfolio.

It can be easy to lose sight of which way is up when the market feels like it’s upsidedown. Action on Wall Street through the first three weeks of 2016 led to losses on the broader averages of nearly 10%, while the tech-heavy Nasdaq shed more than 11%: The second-worst start to a new year for the S&P 500 ever. To prove the point, according to Goldman Sachs’ (NYSE:GS) economics research, in the first 12 trading days of the year, $1.6 trillion in market value was wiped off the S&P 500.

The rush to the trading floor exit doors has caused a cacophony of concern about whether the U.S. is hurtling toward a recession. But the answer isn’t black and white; there are a number of factors to consider, and several sides to the argument.

What the Manufacturing Sector Could be Indicating

There are a number of economic data points that go into the gross domestic product calculation, a measure of the health and strength of the U.S. economy. Those include spending by consumers and government entities, business and capital expenditures, and net exports.

Economists at Deutsche Bank (NYSE:DB), in a note on Tuesday, said while their forecasts don’t currently call for a recession, they have become more cautious about their outlook due to slowing GDP growth. They pointed specifically to the manufacturing sector, a leading indicator for the broad economy, which has seen several months of contraction. When coupled with weak retail sales and inventories data, they said it paints an even gloomier picture.

Put this way: The three-month change in retail sales, stripped of gasoline sales, sat at about 2.4% in December, the lowest reading since February. Meanwhile, companies accumulated inventory at twice that rate, meaning merchandise sat on sales floors and in warehouses as shoppers bought less than companies expected. That is likely to cause a domino effect on the rest of the sector.

“Hence, we will probably see further inventory liquidation this quarter, which will weigh on production and income. This implies further manufacturing weakness, consistent with last week’s New York Fed Empire Survey,” they explained.

The New York factory gauge fell to -19.4 in January from -6.2 the month prior. It was the lowest reading since March 2009.

As the Deutsche Bank economists explained: Consumer spending doesn’t have to be negative heading into an economic downturn.

“We will probably see further manufacturing weakness, consistent with last week’s New York Fed Empire Survey: The series was down -19.4 in January, the lowest reading since March 2009…The fact that consumption is growing does not necessarily eliminate the recession risk because other, more volatile components of GDP, namely investment and net exports, could precipitate a downturn,” the Deutsche Bank economists warned.

Wells Fargo (NYSE:WFC) Investment Institute strategists Stuart Freeman and Scott Wren said U.S. economic fundamentals point to more moderate job growth, favorable small business sentiment, consumer confidence and lack of inflation to improve growth in 2016.

“While in the near term, the new lows for energy prices will likely impact energy earnings, we continue to believe the resulting ceiling for inflation should particularly benefit the drivers of the domestic consumer economy,” they said in a research note.

Oil: The Elephant on the Trading Floor

As Goldman economists pointed out in their research: Though equity-market selloffs do tend to coincide with most recessions, large selloffs don’t necessarily precede recessions.

They point to the recent and drastic decline in global energy prices, specifically the downturn in the oil market. Prices on Wednesday traded below $27 for the first time since 2003 as worries over global oversupply continued to be a heavy drag on sentiment. Since their July 2008 peak, prices have seen a more than 81% plunge.

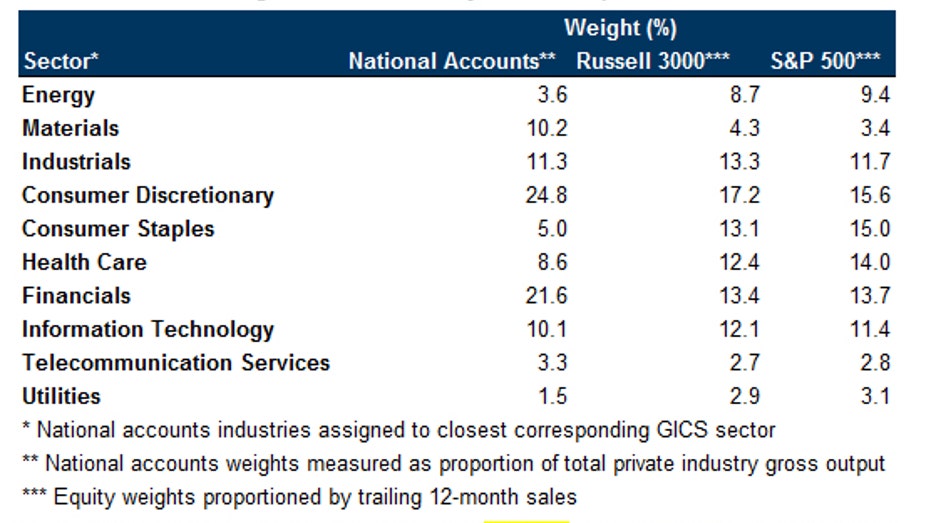

However, it’s important to note the role the oil market plays both in terms of the real economy and the equity markets – and understand how they differ, as Goldman data show in the chart below.

The data showed the energy sector has a much bigger weight in the equity market than it does on the overall U.S. economy (shown as the “national accounts” column).

“Ever since the equity market turmoil first emerged in August of 2015, energy-related equities have been by far the worst performers in the market, at least partially explaining why equities may be suffering more than the real economy as a whole,” the economists explained.

Freeman and Wren added that looking back to 1970, there were 22 times in which the S&P 500 dropped between 9% and 11% over a six-month period. Of those instances, there were 15 times in which the market then rebounded over the following six months.

“We believe that 2016 will also be a year of economic expansion, thus the historical market record lends encouragement,” they said.

Freeman and Wren did issue one warning to investors though: Fourth-quarter earnings season, particularly for energy companies, is likely to be anything but robust.

Still, as with the overall market, they said history points to a bounce back.

“We expect earnings to come in flat to up a touch versus the year-ago period as low oil prices likely led to another disappointing quarter for the energy sector,” they explained. “We had been looking for energy-sector earnings to decline by approximately 55% in 2015, but it appears that the actual results may be worse.”

Outside of energy, Feeman and Wren see “respectable” earnings results, with 2016 earnings for S&P 500 companies to rise by 6% to 67%.

For its part, Citigroup (NYSE:C) said in a note to clients equities have in the past fallen as much as 20%, which would mean the beginning of a bear market, and that had still not been enough to push the economy into recession. While oil price pressure has been significant, exposure to petroleum for banks in developed markets, for example, is on a much smaller scale than the mortgages that precipitated the last financial crisis.

“In sum, for those fearing doom, the grim reaper must indeed deliver. We remain doubtful that the man himself will make an appearance,” the note read.