Wall Street's Bull Market Turns Seven, Will Momentum Last?

Seven years after its start, Wall Street’s bull market is blowing out yet another round of candles on its birthday cake. While some celebrate a recent comeback from an extremely rough start to the year – one that saw year-to-date losses of about 11%, and a nearly 20% drop from its recent peak, which almost ended the market’s run – others say the seventh year might be the lead in for the bears.

So far, the bull market, the third-largest in history, has lasted a total of 84 months, and has risen 215% through last May when it notched its all-time high in the middle of the month. For perspective, that performance is better than the average age of 56 months, and a price advance of 144%, according to data compiled by S&P Global Market Intelligence.

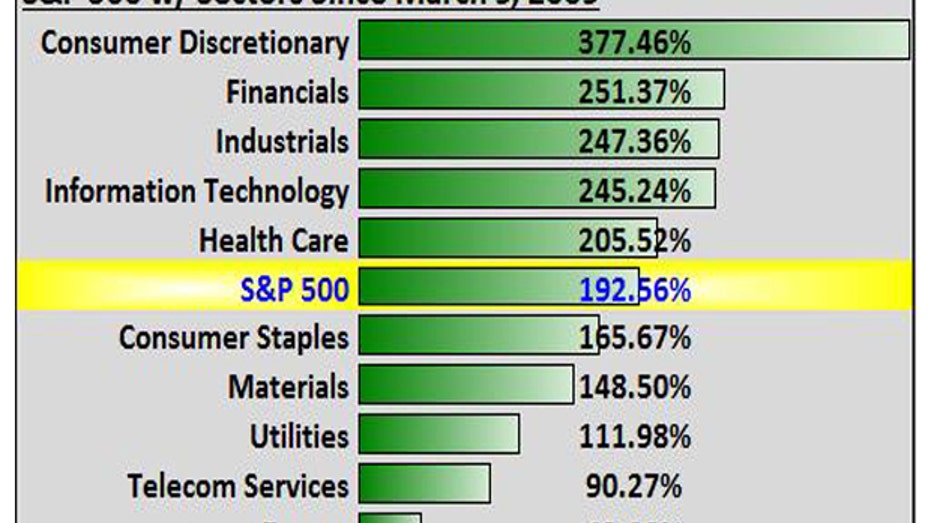

During that time, all 10 S&P 500 sectors rose, led by consumer discretionary, financial, and industrial companies, while energy lagged the most.

Meanwhile, the top S&P 500 winners included General Growth Properties (NYSE:GGP), Regeneron Pharmaceuticals (NASDAQ:REGN), and Under Armour (NYSE:UA), while the top three winners on the Dow have been Apple (NYSE:AAPL), Home Depot (NYSE:HD) and UnitedHealth (NYSE:UNH).

The bull market’s run, however, wasn’t full of just confetti and balloons. During the last year, global stocks have declined 7.6%, while the U.S market fell 4.1%, according to S&P Global Market Intelligence data. Large caps fell the least as they saw a 3.8% decline, while small caps tumbled 5.3% and mid-caps fell 6.2%.

Wall Street was slammed in the first two months of the year thanks to renewed China fears and concern the contagion could spread to the U.S. And investors haven't forgotten about last summer's one-two punch from Greece, which was on the brink of default, and an economic slowdown in China.

David Joy, Ameriprise (NYSE:AMP) Financial’s chief market strategist, said with that in mind, it’s hard to see how the bull market’s run will continue much longer from here.

“I’m skeptical, quite frankly,” he said. “I like the U.S. maybe better than other geography. I think we avoid a recession, but I’m concerned that growth won’t be robust enough to deliver much earnings growth. I think we muddle along. “

Data from the Commerce Department showed fourth-quarter U.S. growth ticked up to a 1% annualized rate. A third reading on 4Q GDP is expected in two weeks, but it’ll be another month after that before investors get a peek at how the global tumult hit the economy in the first three quarters of 2016.

Joy said his optimism on the global economy in general has waned over the last couple of months amid tumult in global markets and no real fiscal reform efforts by nations across the globe.

“Rather than addressing structural problems, they’re resorting to stimulus and re-leveraging, which will probably make problems worse down the road,” he explained. “There’s too much reliance on monetary policy to solve problems it’s ill-equipped to solve.”

To that point, negative interest rate policy has been enacted by several banks across the world including Japan, the eurozone, Sweden, Denmark, and Switzerland. On Thursday, the European Central Bank will conclude its latest policy meeting and is largely expected to slash its deposit rate, currently at -0.3%, by another 0.1% to 0.15%.

Up to this point, the Federal Reserve, which moved to raise interest rates for the first time in nearly a decade in December, has managed to diverge from global central bank policy. However, policymakers have said they are keeping a close eye on both the domestic economy and market developments abroad.

Joy said the biggest threat to the global economy at this point is a deflationary situation, and gone are the days of a significant and sustained boost to equity markets following announcements of fresh rounds of easy-money policies like quantitative easing – a policy in which central banks purchase government bonds or other securities to lower interest rates and increase money supply – and negative rates.

“I think central banks should be focused on encouraging structural reforms rather than convince markets that their toolboxes are full of options.”

“In an environment where most geographies are either commencing or should be commencing the process of deleveraging, it’ll be tough for them even with monetary support to see much growth with the headwinds [across the globe,]” he said. “I think central banks should be focused on encouraging structural reforms rather than convince markets that their toolboxes are full of options.”

To that point, he said the lack of market reaction is likely attributable to an overall understanding that the extraordinary monetary policies are losing their effectiveness and are so well telegraphed to the markets and priced in that unless they do something extremely surprising, the markets will see it as matching expectations.

Before You Close the Book on the Bull Market…

Despite the range of factors threatening to derail the bull market’s longstanding run, there are things in the domestic economy that could give market participants hope for a sustained move higher.

Wells Fargo (NYSE:WFC) Investment Institute global equity strategists Stuart Freeman and Scott Wren, said in a note last week, the odds of a U.S. recession are low. They point to a range of leading indicators including a still-healthy housing market, first-time unemployment claims that continue to trend below 300,000, higher levels of personal income and spending, and better-than-expected retail sales in January.

“We have also seen signs that the manufacturing economy may be stronger than anticipated. For January, the preliminary durable goods orders and capital-goods orders came in ahead of consensus expectations. The prior months’ data for these two leading indicators was revised to levels that were modestly less negative,” they pointed out.

The bottom line, Joy explained is that the U.S. economy and financial markets have come a long way from the bear-market lows notched in the wake of the worst financial crisis since the Great Depression. Essentially, he argued that since the private sector is back on its feet after paying down excessive debts in order to spend again, the public sector needs to follow suit and begin to de-leverage itself after ramping up deficit spending that helped provide economic cover for consumers.