Maybe Stock Bulls Don't Need a Weak Dollar After All

To determine whether the S&P 500 is up or down on any given day, some traders know they often need look no further than the currency markets -- because a stronger dollar tends to lead to lower stock prices.

That’s part of the reason why many have grown bearish on the U.S. equity markets during the intensifying European sovereign debt mess, which has sent the greenback surging almost 6% against the embattled euro this month alone.

But some say the belief that higher stock prices require a weaker U.S. dollar is flawed, as the high degree of negative correlation of the past decade was based on extreme circumstances. Indeed, that simple relationship could soon come to an end.

“We have still found little connection between dollar strength and overall stock market weakness,” Brian Belski, chief investment strategist at BMO Capital Markets, wrote in a research note. “In fact, it appears that current investor worries regarding dollar strength are warranted only in extreme circumstances.”

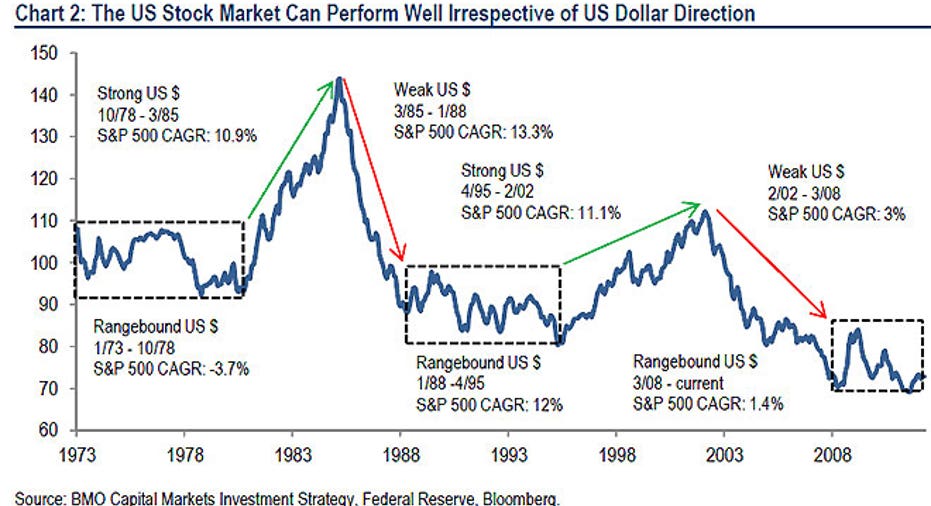

BMO reviewed all rolling 12-month returns for the S&P 500 since 1974 and found that the broad index actually performed better on average during periods of dollar strength than weakness.

“We have been surprised by those investors who have argued that continued stock market momentum requires a weaker U.S. dollar. Based on our work, this is simply not true,” said Belski.

Weak Dollar Boosts Exports

To be sure, there are concrete reasons why bullish equity investors don’t like to see the dollar rise in value. A weaker greenback makes American products and services less attractive abroad, hurting overall exports. That’s become especially important because U.S. companies are increasingly global, relying on faster growing emerging economies like China and Brazil as the developed world (see: Europe) slow.

Over the past decade there has been a close negative correlation between the value of the U.S. dollar and the S&P 500. This period has seen soaring emerging market economic growth, leaping commodity prices and underperformance for the U.S. economy.

All of these characteristics are “clearly U.S. dollar negatives and unsustainable in the long run, in our view,” Belski said.

It's All Relative

The winds have been shifting of late as emerging markets, led by China, have slowed significantly and commodity prices have retreated. Since surging to $109.77 a barrel in late February, crude oil has tumbled almost 20%.

Likewise, while the U.S. recovery remains disappointing, the domestic economy is outperforming some peers like those in Europe. That means, relatively speaking, growth rates at home are improving, a seemingly bullish development for the U.S. markets.

“GDP continues to prod along, and we see no reason for this to be interrupted,” said Belski. “Emerging market growth rates are no longer growing at a feverish pace, while other developed nations are either in or are teetering on recession,” said Belski.

The recent plunge in the value of the euro remains unsettling for many investors. Drowning in fears of a Greek exit and a Spanish banking crisis, the common currency landed below $1.25 on Wednesday -- its lowest level since July 2010 and marking 5.6% slide on the month.

Belski concedes that dramatic moves for the greenback do in fact influence the markets. A 10% or more appreciation for the dollar has led to an average 12-month return of -4.8% for the S&P 500, he said. Conversely, a 10% or more decrease in the greenback has led to average returns of 12.1% for the market.

Still, Belski stresses that “dollar moves of such magnitude have not occurred too often” and the greenback remains up less than 5% so far on the year, far shy of that 10% threshold.

Underlying Reasons Matter

Marc Pado, U.S. market strategist at investment advisory DowBull, said it’s crucial for investors to “decipher the reason why the dollar is moving.”

For example, if the greenback is rising because growth is accelerating, that’s clearly supportive for the markets.

On the other hand, a stronger dollar due to struggles in other parts of the globe isn’t necessarily a good thing for stock prices because it will hurt exports by both making goods less attractive overseas and lowering demand for them.

“You have to delve deeper into the reasons why,” said Pado. Investors today “are not looking at this recent bout of strength [for the dollar] as reflecting a good economic environment,” he said.

Buying Opportunities?

Still, Belski argues that a recent over-reliance on the currency picture has “created certain investment opportunities.”

By focusing on companies with significant foreign exposure but strong underlying fundamentals, Belski lists a slew of stocks he believes have been “adversely and unjustly affected by recent dollar-strength worries.”

His roster of multinationals includes Apple (NASDAQ:AAPL), BlackRock (NYSE:BLK), Eli Lilly (NYSE:LLY), NYSE Euronext (NYSE:NYX), Prudential (NYSE:PRU) and United Technologies (NYSE:UTC).