The Spin Zone

It turns out that breaking up is not all that hard to do -- at least for corporate America.

And for some investors, breakups bring blissful returns. They buy up pieces of big corporations which are spun off to shareholders through new stock issuance or a sale. This generally results in the creation of separate, publicly-traded companies.

Big firms are divesting the assets that are not central to their main business to shareholders. It frees up capital at the parent company and allows them to focus on streamlining profitability. The process also gives the smaller units more autonomy to grow their business and unlock value that may have been overshadowed by other, larger operations within a bigger firm.

Portfolio manager John Keeley, whose Keeley Asset Management oversees $5 billion in assets, has been investing in spinoffs for two decades. Keeley says he likes the focus and fiscal flexibility the newly independent companies often display.

“Rather than being part of a conglomerate, they run their own show. They have access to capital markets, options on their business, and the incentive (for greater profitability) is there.”

Keeley and like-minded investors are cashing in on a corporate spin cycle that picked up speed last year.

The value of completed global spinoff transactions surged to $107.6 billion in 2011, double the prior year’s totals, according to data from Dealogic. It was the largest amount since the recent peak in 2008. The 79 completed deals last year were the most since that same number closed in 2008.

But it’s not just big firms casting off unwanted parts. Ralcorp (NYSE:RAH) just completed its tax-free spinoff of Post Holdings (NASDAQ:POST). Some other household names divested well-known brands during the past year: Cablevision (NYSE:CVC) spun out its AMC Networks (NASDAQ:AMCX) cable network, Marathon Oil (NYSE:MRO) cut ties with Marathon Petroleum (NYSE:MPC), and Expedia (NASDAQ:EXPE) sent TripAdvisor (NASDAQ:TRIP) packing.

The strategy of buying these newly independent public companies has historically paid dividends, figuratively if not literally, in most cases.

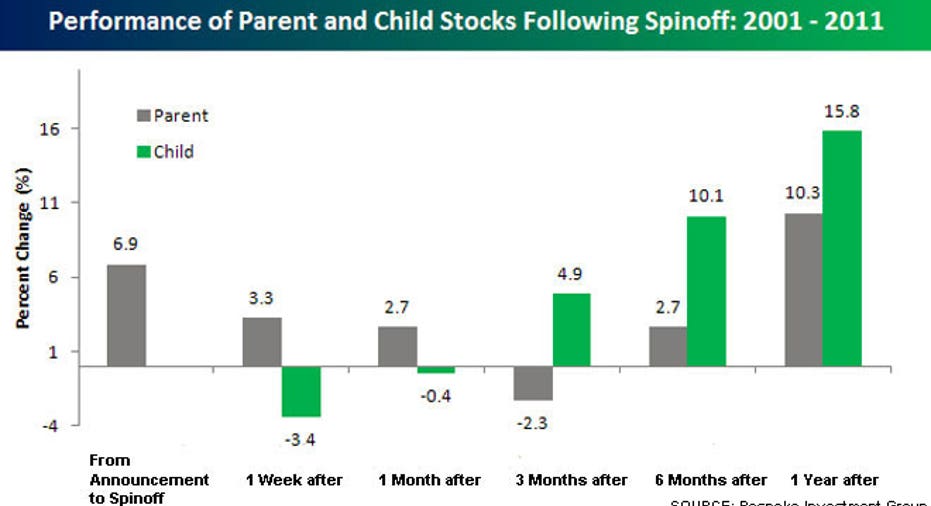

Paul Hickey of research firm Bespoke Investment Group conducted a study of spinoff returns for FOX Business. He found a clear pattern emerged over the past decade. When a company announces a spinoff its shares rally an average of nearly 7% into the completion date, according to the Bespoke data. Initially, the newly created stock tends to underperform the parent stock, as Bespoke found the parent rose 3.3% in the first week while the child stock fell 3.4% in its first five days on the market.

These nascent stocks are often dumped by fund managers who are mandated to own certain types of companies or members of specific indexes. The new issues are often in different lines of business from the mother company and rarely would be immediately added to a major benchmark such as the S&P 500.

But spinoff proponents say this flush opens the window to buy the shares and creates possible arbitrage opportunities.

Hedge fund analysts say they like these under-the-radar spinoff stocks because there is little Wall Street analysis and coverage on the new companies. These analysts say it gives them an advantage to invest in companies that are trying to unlock hidden value for a new class of investors.

And intrepid investors such as Keeley eagerly snap up the shares early on.

“The opportunity it gives is to professionals. The individual has a difficult time because the big brokerage firms are not going to recommend them. They’re not controversial but they’re harder to sell. A lot of people won’t buy stocks unless there are 15 analyst notes on it, and by that time, it’s fully valued.”

Hickey notes the tide tends to change fairly quickly. “The further you get from the actual completion of the spinoff, the better the child stock does on an absolute basis as well as a relative basis (to the parent stock). So the strategy with a spinoff would generally be to wait a few weeks following the completion of the spinoff before wading into the new stock.”

The Bespoke study revealed the child stock showed gains (+4.9%) after three months while the parent’s return slid to negative 2.3%.

Joe Cornell, president of Spin-Off Advisors, agrees that the so-called child company is generally more valuable. “Historically, the most bang for the buck is with the child, but it is deal dependent.”

Cornell’s firm specializes in this corner of the market, advising mutual and hedge fund managers on which deals to buy. “We do sum of the parts analysis and provide price targets.”

Spin-Off Advisors’ report on the Ralcorp deal values the parent stock 5% lower, and sees 9% upside for the Post stock. It also mentions ConAgra’s failed takeover bid for Post and reminds investors that this spin-off “may trigger further M&A activity.”

The spinoff pipeline has a number of deals already on tap for this year. ConocoPhilips (NYSE:COP), Abbott (NYSE:ABT) and Kraft Foods (NYSE:KFT) headline announced spin-offs.

Tom Burnett, who follows corporate deal activity for Wall St. Access, expects a busy year for spinoffs, and is watching for some that have not yet been announced.

“We’ll see something in Yahoo (NASDAQ:YHOO),” Burnett predicts. “There’s too much value locked in its Asian assets. That’s one to focus on. But that transaction will be six months of nail-biting because there’s no guarantee the IRS will bless it and it can’t go forward without it."

Burnett is also closely watching Bank of America (NYSE:BAC) for a potential spin move. “They have tremendous problems with (mortgage unit) Countrywide Financial, but Merrill Lynch is performing very well. You can give shareholders a chance to get a piece of Merrill from existing shares and reduce the share count (at Bank of America).”

As investors consider a new class of initial public offerings being led out of that pipeline by Facebook, they may want to consider these new shares of familiar names instead of flashy new names to the exchange lists.

University of Florida Finance Professor Jay Ritter has studied the returns of spinoffs versus other IPOs and found that corporate carveouts from larger companies were the best bets among new offerings from 1980-2009, while small IPOs were the worst.

“The larger spinoffs (which would usually be from larger companies) do better than the smaller spinoffs,” he says, adding, “In general spinoffs do better than other IPOs.”