Today's 30-year mortgage refinance rates plunge to 14-day low | Nov. 30, 2021

Drops in 3 key rates push average mortgage refinance rate to two-week low

Check out the mortgage refinancing rates for Nov. 30, 2021, which are mostly down from yesterday. (iStock)

Based on data compiled by Credible, current mortgage refinance rates fell for the three longest terms and held steady for the shortest term compared to yesterday.

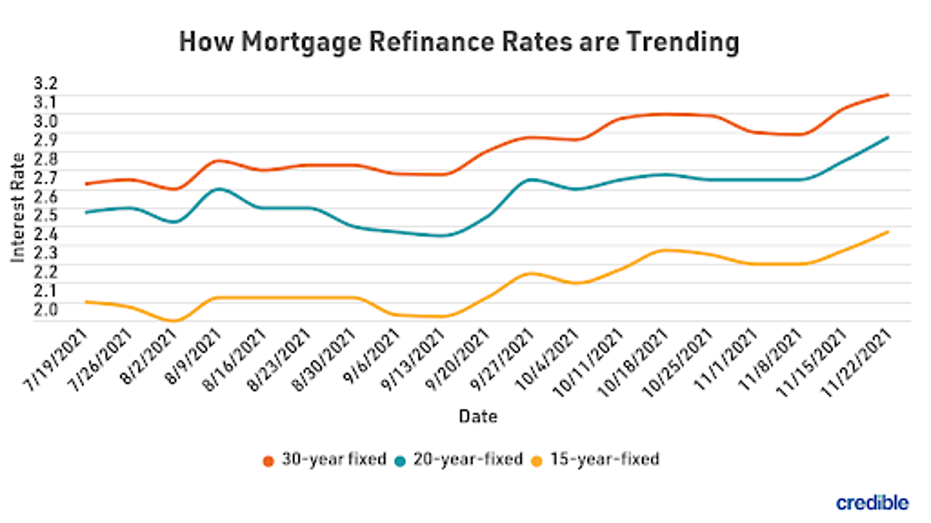

- 30-year fixed-rate refinance: 3.050%, down from 3.250%, -0.200

- 20-year fixed-rate refinance: 2.750%, down from 2.875%, -0.125

- 15-year fixed-rate refinance: 2.375%, down from 2.500%, -0.125

- 10-year fixed-rate refinance: 2.375%, unchanged

Rates last updated on Nov. 30, 2021. These rates are based on the assumptions shown here. Actual rates may vary.

Despite mortgage experts’ predictions that rates will continue to rise at the end of the year, rates dropped for three out of four terms today. Homeowners who are considering a refinance might want to act quickly to lock in a money-saving rate. Rates for a 30-year refinance, which is the most common term, sank to their lowest level in 14 days. Rates also fell for 20-year and 10-year terms. Homeowners who can swing a higher monthly payment might opt for a shorter term to realize even more interest savings over the life of their mortgage.

These rates are based on the assumptions shown here. Actual rates may vary.

If you’re thinking of refinancing your home mortgage, consider using Credible. Whether you're interested in saving money on your monthly mortgage payments or considering a cash-out refinance, Credible's free online tool will let you compare rates from multiple mortgage lenders. You can see prequalified rates in as little as three minutes.

Current 30-year fixed refinance rates

The current rate for a 30-year fixed-rate refinance is 3.050%. This is down from yesterday. Refinancing a 30-year mortgage into a new 30-year mortgage could lower your interest rate, but may not have much effect on your total interest costs or monthly payment. Refinancing a shorter-term mortgage into a 30-year refinance could result in a lower monthly payment but higher total interest costs.

Current 20-year fixed refinance rates

The current rate for a 20-year fixed-rate refinance is 2.750%. This is down from yesterday. By refinancing a 30-year loan into a 20-year refinance, you could secure a lower interest rate and reduce total interest costs over the life of your mortgage. But you may get a higher monthly payment.

Current 15-year fixed refinance rates

The current rate for a 15-year fixed-rate refinance is 2.375%. This is down from yesterday. A 15-year refinance could be a good choice for homeowners looking to strike a balance between lowering interest costs and retaining a manageable monthly payment.

Current 10-year fixed refinance rates

The current rate for a 10-year fixed-rate refinance is 2.375%. This is the same as yesterday. A 10-year refinance will help you pay off your mortgage sooner and maximize your interest savings. But you could also end up with a bigger monthly mortgage payment.

You can explore your mortgage refinance options in minutes by visiting Credible to compare rates and lenders. Check out Credible and get prequalified today.

Rates last updated on Nov. 30, 2021. These rates are based on the assumptions shown here. Actual rates may vary.

What is the average cost of a refinance?

Refinancing a mortgage can yield significant interest savings over the life of a loan. But all those savings don’t come for free. Generally, you’ll encounter costs — $5,000 on average, according to Freddie Mac — when refinancing your mortgage.

Your exact refinancing costs will depend on multiple factors, including the size of your loan and where you live. Typical refinancing costs include:

- The cost of recording your new mortgage

- Appraisal fees

- Attorney fees

- Lender fees, such as origination or underwriting

- Title service fees

- Credit report fees

- Mortgage points

- Prepaid interest charges

Keep in mind there’s no such thing as a truly no-cost refinance. Lenders who market "no-cost loans" typically charge a higher interest rate and roll the costs into the loan — which means you’ll pay more interest over the life of the loan.

How to get your lowest mortgage refinance rate

If you’re interested in refinancing your mortgage, improving your credit score and paying down any other debt could secure you a lower rate. It’s also a good idea to compare rates from different lenders if you're hoping to refinance so you can find the best rate for your situation.

Borrowers can save $1,500 on average over the life of their loan by shopping for just one additional rate quote, and an average of $3,000 by comparing five rate quotes, according to research from Freddie Mac.

Be sure to shop around and compare rates from multiple mortgage lenders if you decide to refinance your mortgage. You can do this easily with Credible’s free online tool and see your prequalified rates in only three minutes.

How does Credible calculate refinance rates?

Changing economic conditions, central bank policy decisions, investor sentiment and other factors influence the movement of mortgage refinance rates. Credible average mortgage refinance rates are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage refinance rates will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

Is now a good time to refinance?

Mortgage refinance rates have been at historic lows all year. It’s unlikely they’ll go much lower and extremely possible they’ll begin to rise in the coming months. But low rates aren’t the only factors that determine whether now is a good time for you to refinance your home loan.

Everyone’s situation is different, but generally, it may be a good time to refinance if:

- You’ll be able to get a lower interest rate than you currently have.

- Refinancing will save you money over the life of your home loan.

- Your savings from refinancing will ultimately exceed closing costs.

- You know you’ll be staying in your home long enough to recoup the costs of refinancing.

- You have sufficient equity in your home to avoid private mortgage insurance (PMI).

If your home needs significant, costly repairs it might be a good time to refinance in order to withdraw some equity to pay for those repairs. Just be aware that lenders generally limit the amount you can take from your home in a cash-out refinance.

Credible is also partnered with a home insurance broker. If you're looking for a better rate on home insurance and are considering switching providers, consider using an online broker. You can compare quotes from top-rated insurance carriers in your area — it's fast, easy and the whole process can be completed entirely online.

Think it might be the right time to refinance? To understand just how much you could save on monthly mortgage payments by refinancing now, crunch the numbers and compare rates using Credible's free online tool. Within minutes, you can see what multiple mortgage lenders are offering.

Rates last updated on Nov. 30, 2021. These rates are based on the assumptions shown here. Actual rates may vary.

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.

As a Credible authority on mortgages and personal finance, Chris Jennings has covered topics that include mortgage loans, mortgage refinancing, and more. He’s been an editor and editorial assistant in the online personal finance space for four years. His work has been featured by MSN, AOL, Yahoo Finance, and more.