The big retirement savings mistakes Americans are making

Americans are making key mistakes when it comes to saving for their retirement, according to a survey conducted by MagnifyMoney.

Nearly half of the people surveyed have withdrawn money from their employer-sponsored retirement savings account, and nearly one-fifth of those surveyed are not contributing the proper amount in order to maximize their employer's match.

"The most damning finding of all is that 27% of those surveyed have never thought about how much they’ll need in retirement," the survey report states. "And while 'ignorance is bliss' may hold true when it comes to some things in life, this expression should not apply to your retirement plans."

The survey did not distinguish whether the people replenished their 401(k)s after withdrawing money from them by taking a loan.

Since retirement savings are intended to be used during retirement, withdrawing them earlier than intended can be detrimental down the line, which could lead to people working longer than expected in order to be able to financially support themselves.

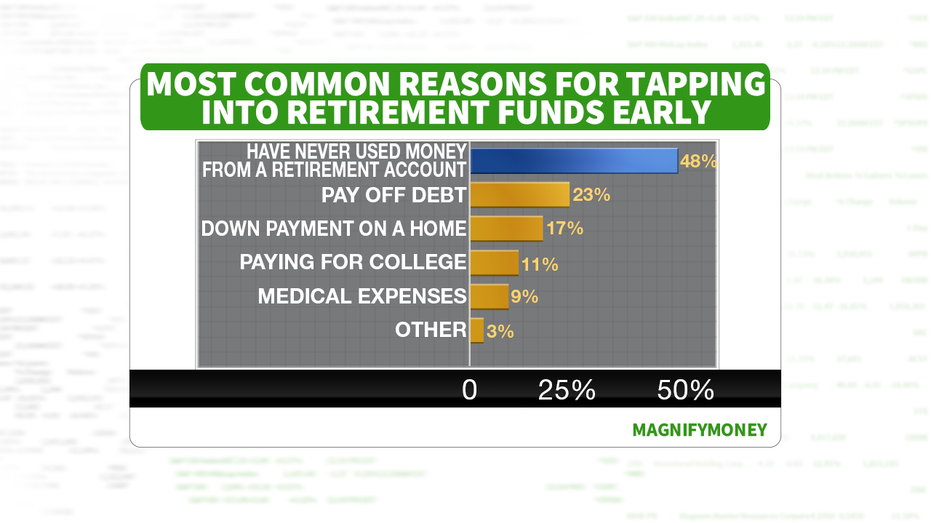

Most of the people surveyed have withdrawn money from their retirement plan to either pay off debt or to help buy a home, and a fifth are not setting aside enough money to reap the benefits of an employer-sponsored match.

Most common reasons for a retirement savings withdrawal

Buying a home

Experts still recommend people put down at least 20% in a down payment when it comes to buying a home in order to optimize your mortgage payments. Student loans and credit card debt loom over many younger generations, which is why some millennials are withdrawing their retirement savings in order to accomplish what they consider to be their dreams of owning a home or paying down their debt.

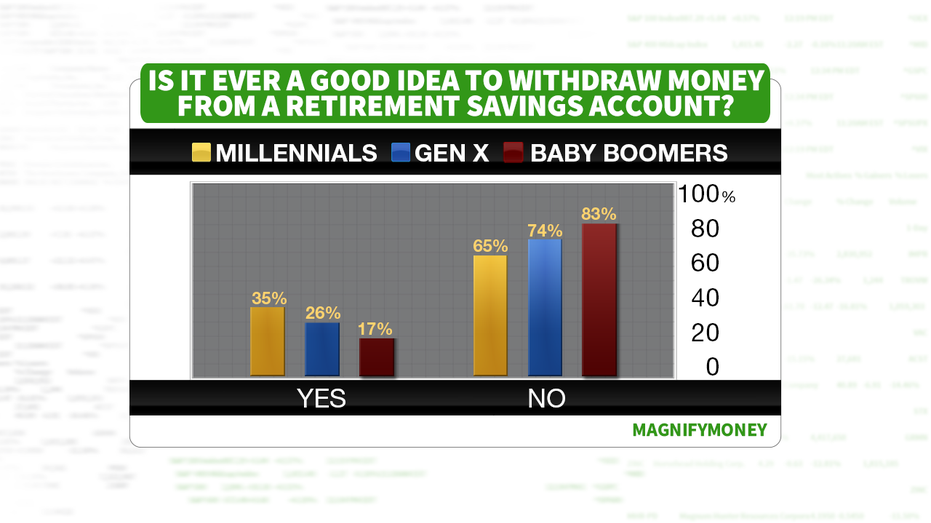

In general, more than one-third of millennials (36%) found it acceptable to withdraw from their retirement savings, versus only 26% of Gen Xers finding that to be an appropriate action. Not surprisingly, only 17% of baby boomers felt withdrawing from their retirement savings to be acceptable.

Withdrawing your retirement funds before the appropriate age to do so will inevitably result in financial penalties, including fees and taxes.

The breakdown between the generations on retirement savings withdrawals

Maximizing employer matches

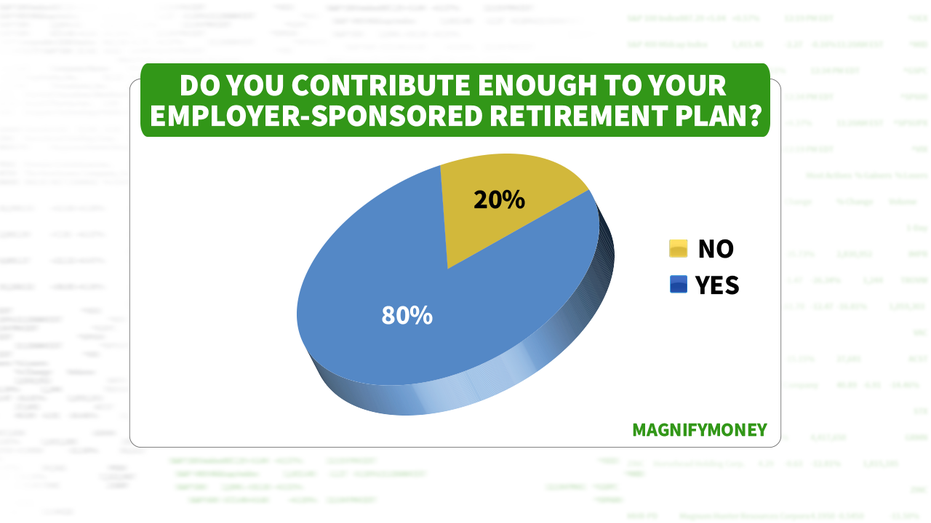

While 80% of those surveyed contribute the proper amount to their employer-sponsored savings plan, 20% admitted they don't maximize the opportunity given to them by contributing enough money to earn employer-sponsored matches. Losing out on the "free money" your company gives you in their match program is a critical financial mistake.

Experts find it's crucial to save early and save often in a person's career in order to ensure retirement is financially achievable. Let's say your employer matches 100% of your contribution up to 3% of your salary and matches 50% of your contribution up to 5% of your salary, maximizing that contribution can make or break someone's retirement savings.

Contributions to employer-sponsored retirement plan

Using numbers to better understand these percentages, if you make $3,000 per paycheck and you contribute 10% of your salary to your 401(k), then $300 of your own money is put into your 401(k) and your employer would deposit an additional $120 per paycheck to your 401(k). This means if you don't maximize how much your employer is willing to match, you are missing out on an additional 4% of so-called "free money" if you don't contribute at least 5% of your salary to your 401(k).

This survey also showed other retirement savings mistakes, including 35% saying they aren't saving enough for retirement. Financial experts reiterate it's crucial to contribute to your retirement plan as soon as possible, as a smaller amount invested earlier will compound to a larger amount later.

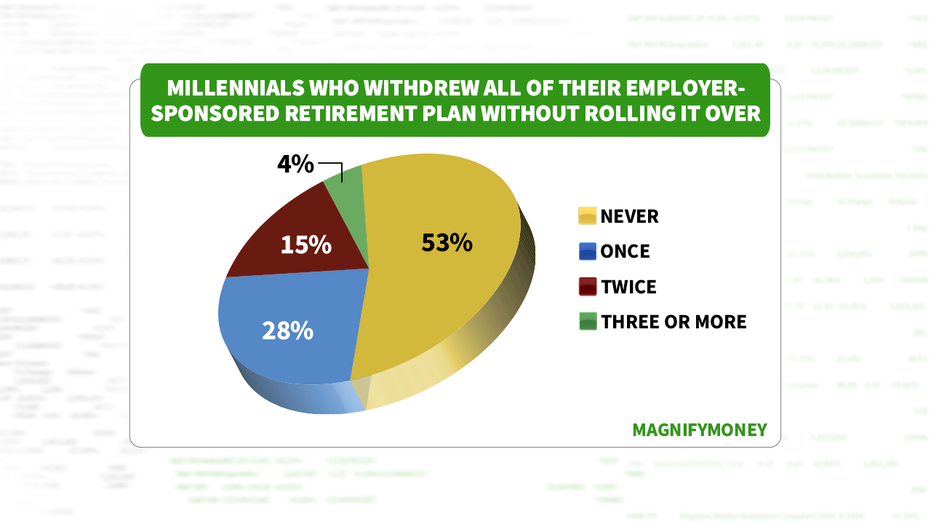

And when changing jobs, instead of rolling over their retirement savings plan from one company to another, nearly one-third of people surveyed said they withdrew the balance.

Withdrawing employer-sponsored savings plan without rolling over