Payday loan borrowers charged steep rollover fees despite consumer protections: CFPB

Debt consolidation may help you break the payday loan cycle

Payday loan lenders offer short-term loans and cash advances, but these products come with high interest rates that often lead to a debt trap, the CFPB found. (iStock)

Payday lenders provide small-dollar loans that are repaid in a single lump-sum installment, typically on the borrower's next payday. While these loans may offer fast funding without a credit check, they often trap consumers in a cycle of debt due to the short repayment term and high annual percentage rate (APR).

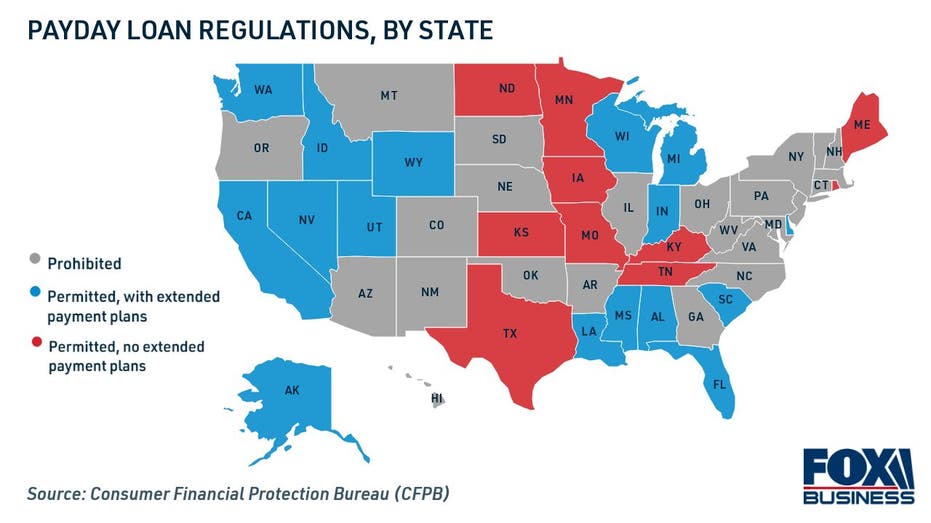

Out of the 26 states that permit payday lending, 16 of them require lenders to offer free extended payment plans to deter re-borrowing. But even in the states that implemented these consumer protections, payday loan borrowers continue to pay steep rollover fees, according to a new report from the Consumer Financial Protection Bureau (CFPB).

SEEKING DEBT RELIEF? HERE’S HOW CREDIT COUNSELING CAN HELP

"Our research suggests that state laws that require payday lenders to offer no-cost extended repayment plans are not working as intended," CFPB Director Rohit Chopra said. "Payday lenders have a powerful incentive to protect their revenue by steering borrowers into costly re-borrowing."

Keep reading to learn more about the CFPB's recent study, as well as how you can break the cycle of payday loan debt. One option to consider is consolidating payday loans into a fixed-rate personal loan. You can visit Credible to compare debt consolidation loans for free without impacting your credit score.

DEBT CONSOLIDATION VS. DEBT SETTLEMENT: WHAT'S THE DIFFERENCE?

Extended payment plans can save borrowers money, but many don't use them

If a borrower can't repay their payday loan, they have a few options: roll over their loan for another two weeks, default on their loan or enroll in an extended payment plan — at least in the 16 states that require them.

On a typical $300 payday loan, borrowers can see substantial savings by utilizing a payment extension rather than rolling over the loan. The CFPB estimates that a borrower would incur $360 in rollover fees over the course of four months, compared to a one-time $45 fee for an extended payment plan.

Despite the obvious benefits, extended repayment plan usage rates in the states that offer this option are still much lower than payday loan rollover rates. In other words, payday loan borrowers were far more likely to roll over their loans rather than utilize an extended repayment plan.

For example, the rollover rate was 16.4% in Wisconsin last year, compared to the extended payment plan usage rate of just 2%. And just 0.4% payday borrowers in Florida utilize payment plan extensions, while more than a quarter (26%) have 10 or more loans.

If you're struggling to repay multiple payday loans, you might consider consolidating into a single personal loan. Unlike payday loans, personal loans offer fixed interest rates and longer, more predictable repayment terms. You can learn more about payday loan consolidation on Credible.

WHAT ARE CREDIT UNION LOANS AND HOW DO YOU GET ONE?

Eligibility criteria may contribute to low extended payment plan usage rates

One reason for the low usage of extended repayment plans is "a substantial variation in eligibility requirements" payday loan borrowers must meet per state regulations, the CFPB found.

Alaska's law requires borrowers to repay at least 5% of the outstanding loan balance before they can qualify for a payment plan extension. Utah allows lenders to charge a 20% initial payment if a borrower enters an extended payment plan after default.

In Florida, borrowers must enroll in credit counseling services to be eligible for an extended grace period. This can pose a potential time-consuming roadblock for borrowers who feel the urgency of missing a loan payment.

Just seven of the 16 states that require extended payment plans require lenders to make borrowers aware of this repayment option before they take out a loan. And in most states, borrowers can only utilize one extended repayment plan in a 12-month period.

As an alternative to payday loan rollovers and extended payment plans, some borrowers might consider repaying their debt with a fixed-rate personal loan. Debt consolidation may help you spread out your debt payments over a longer period of time. You can compare current rates in the table below, and use Credible's personal loan calculator to estimate your monthly payment.

5 SMART WAYS TO CONSOLIDATE CREDIT CARD DEBT

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.