Unpaid medical bills account for 58% of debt in collections: CFPB report

43M Americans have unpaid medical bills on their credit report

Medical debt is an issue for millions of Americans who have hospital bills in collections. Here's what the CFPB plans to do about medical credit reporting and how you can get rid of unpaid medical debt. (iStock)

The majority (58%) of debt in collections stems from medical bills, according to a new report from the Consumer Financial Protection Bureau (CFPB). Roughly 43 million Americans have medical bills on their credit report, with a total outstanding medical debt of $88 billion.

CFPB Director Rohit Chopra said during a press conference that the bureau is taking steps to clarify the role of medical bills in credit reporting, and may even consider banning the major credit bureaus from including medical debt when calculating credit scores.

"Even when a patient tries to battle to get an accurate bill or an insurance claim paid, medical debt collectors have a weapon that is hard to fight against: the credit report," Chopra said.

Past-due medical bills on a patient's credit report can lower their credit score, making it harder to qualify for favorable loan terms on mortgages, student loans and other credit products. Medical debt in collections can eventually result in late fees, costly legal proceedings, wage garnishment and often bankruptcy.

"Having a medical debt collection mark on a credit record can make it harder to get credit, rent or buy a home, or find a job," Chopra said. "Families are pushed into bankruptcy by medical debts that they cannot pay."

Keep reading about how the CFPB plans to increase consumer protections when it comes to medical bills in credit reporting, as well as how you can pay off medical debt in collections. If you're struggling with unpaid medical bills, you can enroll in free credit monitoring services on Credible to get notifications of changes to your credit report.

MEDICAL DEBT IS THE LEADING CAUSE OF BANKRUPTCY, DATA SHOWS

CFPB director unveils plan to evaluate medical debt reporting

In light of its recent report of the impacts of unpaid medical bills in credit reporting, the CFPB is taking several steps to address the issue:

- Revisit the inclusion of medical debt in credit reporting.

The CFPB is working with government agencies and the medical community to determine whether it's appropriate for unpaid medical bills to be included on credit reports. Debt collectors often use "coercive credit reporting" and the threat of negative credit impacts to strong-arm patients into paying their medical debt.

"Many in the health care community have already taken steps to avoid this behavior and to work constructively with patients before launching an assault on their credit report," Chopra said.

The bureau may consider blocking debt collectors from reporting past-due medical bills to the credit bureaus altogether.

- Expand access to medical billing financial aid programs.

Nonprofit hospitals are required by federal law to offer financial assistance programs, such as payment plans and reduced-cost care. The CFPB is determining the best practices for facilitating patients' access to financial aid.

Additionally, the bureau is partnering with the Department of Health and Human Services (DHHS) "to ensure patients are not charged and do not pay illegal surcharges for medical care," Chopra said. This is in compliance with the No Surprises Act, which aims to protect patients against surprise medical bills.

- Investigate medical debt reporting practices by credit bureaus.

Credit reporting agencies are required to identify inaccurate reports of debt owed per The Fair Credit Reporting Act (FCRA). This is a top concern for the CFPB, as Chopra said the medical billing and collections system is "error-plagued" and confusing for patients to navigate.

To aid patients who often struggle to determine the validity of their medical bills, the CFPB will be closely monitoring the reporting practices of Equifax, Experian and TransUnion. This will ensure that credit reports aren't "being used as a tool to coerce and extort patients on medical bills they may not even owe," Chopra said.

NEARLY 1 IN 5 AMERICANS HAS UNPAID MEDICAL DEBT, STUDY FINDS

How to pay off medical debt in collections

Past-due medical bills can hurt your credit score and have serious financial consequences over time. Here are a few strategies for managing medical debt in collections:

- Dispute medical debt on your credit report

- Negotiate a settlement with the debt collector

- Get in touch with a credit counseling agency

- Repay the debt with a 0% APR credit card offer

- Consolidate your debts with a fixed-rate loan

Read more about each strategy in the sections below.

Dispute medical debt on your credit report

The major credit bureaus must wait 180 days before including medical debt on your credit report, according to Experian. This grace period gives consumers six months to resolve medical billing errors, enroll in a payment plan or pay off the debt.

To determine if you were billed inaccurately, look for common medical billing errors like double-billing and incorrect coding. Also request an Explanation of Benefits (EOB) from your health insurance company to determine if you were charged for a service that should have been covered by insurance.

If you've been billed in error, you can file a dispute through the credit reporting agency directly. You can also enroll in Experian credit monitoring services on Credible to identify and address errors on your credit report in a timely manner.

HOW LONG DO NEGATIVE ITEMS STAY ON YOUR CREDIT REPORT?

Negotiate a settlement with the debt collector

If your unpaid medical bill is a legitimate charge, it may be possible to settle the debt for less or enroll in a payment plan. The CFPB offers a few tips for negotiating debt settlement with a collector:

- Get more information about the debt, such as its origin and how much money you owe. If you don't recognize the debt, you can ask the collector for more information about the original creditor.

- Make a realistic debt settlement or repayment proposal. Determine how much you could afford to pay on the debt each month or the total amount you're willing to pay to settle the debt. If your debt is old, you may want to contact a lawyer first to see if it has reached your state's statute of limitations.

- Explain your current financial situation and proposed repayment plan to the debt collector. You may have more room to negotiate with a debt collections agency than you did with the original creditor. Take detailed notes and record your conversation if necessary.

Be sure to get any debt settlement agreement in writing before you make a payment.

Get in touch with a credit counseling agency

It may seem intimidating to negotiate high levels of medical debt with a third-party debt collector. To ensure the process is completed to your advantage, you could consider credit counseling services.

A credit counselor may be able to negotiate with your creditors on your behalf. This can include reaching a debt settlement agreement, waiving late fees and enrolling you in a debt management plan (DMP). Credit counseling is often free, but some services may come at a low cost.

Nonprofit credit counseling agencies are regulated by federal law. You can see a full list of accredited credit counselors on the Department of Justice website.

Repay the debt with a 0% APR credit card offer

Some credit card issuers offer an introductory 0% APR period of up to 21 months for consumers who open a new card. It may be possible to pay off your medical bills in collections with a credit card, then chip away at the debt in monthly payments during the zero-interest period.

If you repay the debt in full by the time the 0% APR offer expires, you can effectively avoid paying interest on your medical bills altogether. Any remaining balance after the zero-interest period will be charged regular purchase APR, which can often be high.

These promotional offers are typically reserved for applicants with very good or excellent credit, defined by the FICO scoring model as 740 or higher. To see if you meet the eligibility requirements, you can visit Credible to compare credit cards with zero-interest introductory periods.

15 BEST DEBT CONSOLIDATION LOANS FOR FAIR CREDIT

Consolidate your debts with a fixed-rate loan

Another common way to repay medical bills is with a debt consolidation loan. This is a type of fixed-rate personal loan that you repay in fixed monthly payments over a set period of time, typically a few years.

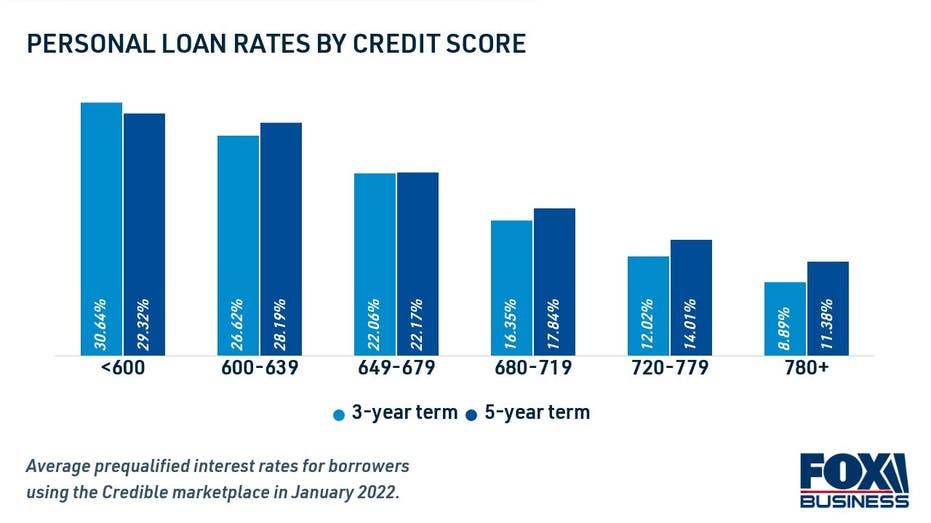

Since personal loans are typically unsecured and don't require collateral, lenders determine your eligibility and interest rate based on your credit history and debt-to-income ratio. Applicants with good credit will qualify for the lowest personal loan rates, while those with bad credit may see high interest rates — if they qualify at all.

Because you'll pay interest charges for borrowing a debt consolidation loan, this may be a last resort after debt settlement and medical bill negotiation. But if you've exhausted your alternative medical debt relief options, personal loans can provide a fast funding option to help you pay off debt in collections on a predictable repayment schedule.

You can use a personal loan calculator to estimate your monthly payments using this debt consolidation strategy. If you decide to borrow a debt consolidation loan, be sure to compare rates across multiple lenders on an online marketplace like Credible to shop for the lowest rate possible for your financial situation.

HOW TO GET RID OF MEDICAL DEBT WITHOUT DAMAGING YOUR CREDIT

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.