How to pay off $300K in student loan debt

If you have more than $300K in student loans, you can pay this debt off with the right repayment strategies

If you’re wondering how to pay off $300K in student loan debt, here are 4 repayment strategies you can use. (Shutterstock)

Leaving college with six figure student loans can be overwhelming, but it is possible to pay off that debt. With the right repayment strategies, you don’t have to struggle with a lifetime of student loan debt.

Refinancing is an option to help pay off your debt. By visiting Credible, you can learn more about student loan refinancing and compare rates from multiple private student loan lenders.

- How much does $300,000 of debt cost?

- How to pay off $300K in student loans

- How long will it take to pay off $300K in student loans?

How much does $300,000 of debt cost?

When you take out a loan, your principal, interest rate, and repayment terms will affect how much that debt ends up costing you. For example, if you have a high interest rate or longer repayment term, you’ll end up paying more in interest over the life of the loan.

Student loan debt can be complicated because most borrowers take out multiple loans to pay for their education. And you may have a combination of multiple federal and private loans at varying interest rates.

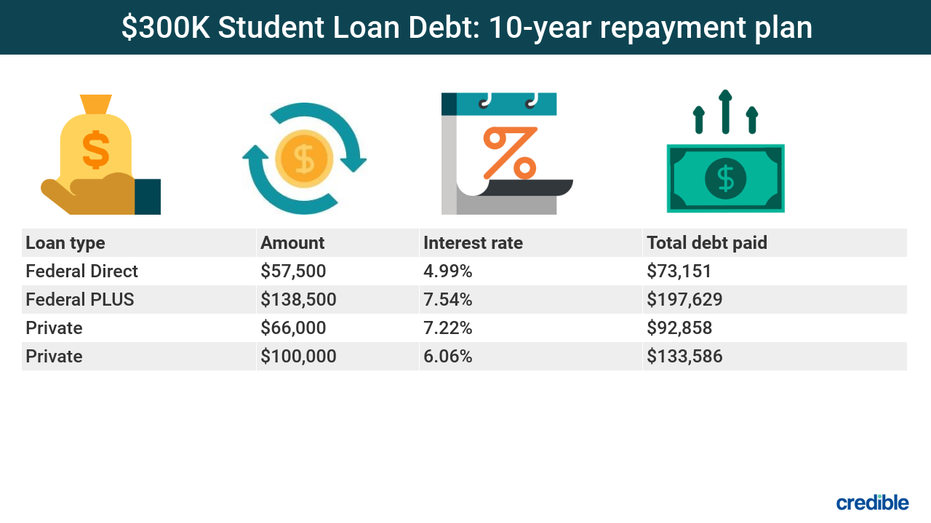

Here’s an overview of what you could expect to pay for $300,000 in total student loan debt with all your loans on a 10-year repayment plan:

In this scenario, with $362,000 in student loan debt at these varying interest rates, your total cost would be $497,224. Paying off these loans as soon as possible will help minimize the interest costs.

BIDEN CANCELS $10K IN STUDENT LOAN DEBT PER BORROWER — WHAT TO KNOW

How to pay off $300K in student loans

When you take out student loans, the interest costs can quickly add up. If you’re looking for ways to pay off more than $300,000 in student loan debt, here are four strategies you can implement.

Debt avalanche method

The debt avalanche method focuses on paying off the debt with the largest interest rate first. The goal is to reduce the total amount of interest you end up paying.

Using the previous student loan example, you’ll start by putting any extra money you have toward the $138,000 debt. That debt happens to be the largest, but you’ll make extra payments on it because it has the highest interest rate.

You’ll continue to make minimum payments on your other three loans. Once that loan is paid off, you’ll put that money toward the loan with the next-highest interest rate, which is the loan for $66,000.

DEBT SNOWBALL METHOD VS. DEBT AVALANCHE: WHAT’S THE DIFFERENCE?

Debt snowball method

The debt snowball method focuses on paying off your smallest debt first. So using the example above, you’d start by putting any extra money you have toward the $57,500 student loan and making minimum payments on the rest.

Once that loan has been repaid, you’ll put that money toward the $66,000 loan. The idea is that you create a snowball effect and will see progress more quickly as you pay off the smallest debt first. But you may end up paying more in interest with this method.

Consider refinancing your debt for a lower interest rate. You can easily compare prequalified rates from multiple lenders using Credible.

Loan forgiveness

Certain federal loan borrowers may qualify for student loan forgiveness. When your loans are forgiven, you’re no longer required to repay the balance. Several different types of loan forgiveness are available:

- Public Service Loan Forgiveness (PSLF): PSLF is available to federal student loan borrowers who are employed full-time by a government or not-for-profit organization. Once you’ve made 120 qualifying payments, your remaining loan balance is forgiven.

- Teacher Loan Forgiveness: The Teacher Loan Forgiveness Program is available to teachers who work full-time for five consecutive years in a low-income school. If you qualify, you could receive up to $17,500 in loan forgiveness.

- Borrower Defense to Repayment: If you took out loans and attended a school that misled you or engaged in some type of misconduct, you may be eligible to have those loans forgiven through the Borrower Defense to Repayment.

Refinancing

One of the challenges that comes with student loan repayment is having multiple loans at varying interest rates. One way to deal with this is by refinancing your loans into a single loan with a lower interest rate.

But keep in mind that if you refinance federal loans into a private loan, you’ll lose access to certain borrower protections, including income-driven repayment (IDR) plans and loan forgiveness. And if you have a poor credit score, you may need to apply with a cosigner.

HOW TO RELEASE A COSIGNER FROM YOUR STUDENT LOANS

How long will it take to pay off $300K in student loans?

All federal student loans start off with a standard 10-year repayment term unless you enroll in a different repayment plan. IDR plans, for example, allow you to extend your repayment term and receive a more manageable monthly payment.

However, by extending the repayment term you could end up paying more in interest. The repayment term you receive on private loans will depend on your lender.

Repaying six figures in student loan debt can feel like a daunting task, but you can find ways to do it. By refinancing to a shorter term and making extra payments, you can pay your loans off faster and reduce the total amount paid in interest. If you have federal student loans, you should see if you qualify for loan forgiveness.

To get started on refinancing your student loans, visit Credible and compare prequalified rates from multiple lenders.