15-Year Fixed Refinance Rates

Refinancing to a 15-year mortgage has plenty of perks, but it’s not the right move for everyone.

Considering refinancing your mortgage? It could be the right time to look into 15-year refinance rates. (Shutterstock)

Homeowners interested in getting a lower interest rate and paying off their mortgages faster might consider a 15-year mortgage refinance. In the second quarter of 2021, 30% of borrowers shortened their loan term when refinancing, according to Freddie Mac.

If you’re thinking about refinancing, here’s what you need to know about 15-year refinance rates.

Credible lets you compare mortgage refinance rates from various lenders, all in one place.

- Today's 15-year mortgage refinance rate trends

- Historical mortgage rates

- How Credible mortgage refinance rates are calculated

- Pros of a 15-year mortgage refinance

- Cons of a 15-year mortgage refinance

- When is the right time to refinance?

- How to get your lowest mortgage refinance rate

- What is the average cost of a refinance?

- What credit score do you need to get a good 15-year refinance rate?

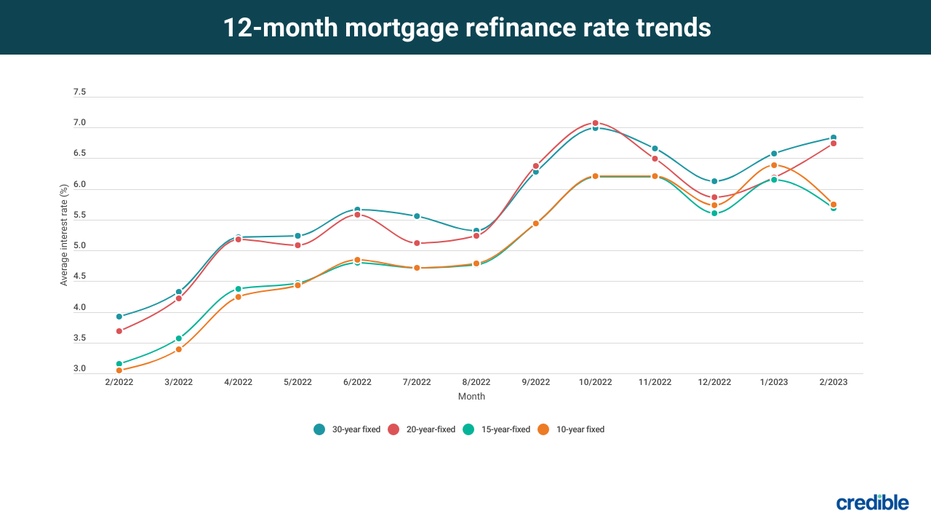

Today’s 15-year mortgage refinance rate trends

Here’s how mortgage refinance rates have been trending over the past 12 months.

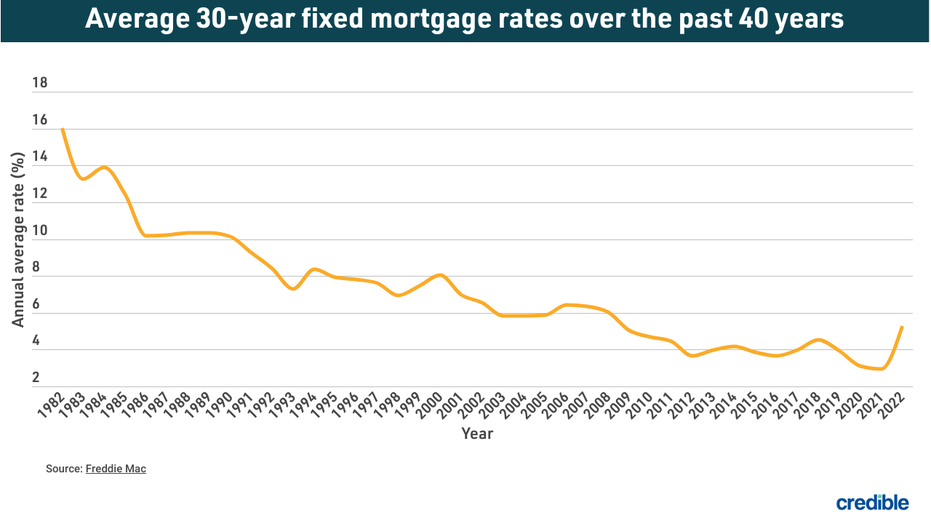

Historical mortgage rates

Here’s what the annual average mortgage interest rate has looked like over the past 39 years.

How Credible mortgage refinance rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment, and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional home loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

Pros of a 15-year mortgage refinance

While a 15-year mortgage refinance isn’t nearly as popular as a 30-year refinance, it does have several advantages:

- Pay less interest. On average, you’ll pay less total interest over the life of the loan. Because you’re paying off your mortgage sooner, you’ll shave years off your interest payments.

- Build equity faster. The 15-year term allows you to build equity much faster than with a 20- or 30-year loan.

- Pay off your loan sooner. When compared to a 30-year loan, a 15-year loan lets you pay off your loan in half the time and own your home outright faster.

Cons of a 15-year mortgage refinance

A 15-year mortgage refinance also has some downsides to consider:

- Your monthly payment may be higher. If you’re refinancing to a shorter loan term, you’ll face higher monthly mortgage payments.

- You may have less money to put toward other goals. A higher monthly payment may prevent you from building up your emergency fund or putting money away for retirement. You may be "house rich," but you could end up "cash poor."

- You’ll pay refinancing fees. It’s not uncommon to pay from 3% to 6% of the total loan amount in refinancing fees, but these costs vary from one lender to the next.

When is the right time to refinance?

Refinancing can be the right move if your interest rate is much higher than the current interest rate for a 15-year refinance.

Consider whether or not the monthly savings you gain from refinancing add up to more than the closing costs you’ll pay when obtaining a new home loan. These costs vary but can include loan origination and application fees, home appraisal costs, credit report fees, title search and insurance fees, mortgage points, and a settlement fee.

But when you refinance, you also have the opportunity to save on your monthly payment, qualify for a lower interest rate, shorten your loan term, or even cancel your mortgage insurance payments (if you’ve built up enough equity in your home).

With Credible, you can compare mortgage refinance rates from multiple lenders without affecting your credit.

How to get your lowest mortgage refinance rate

www.foxbusiness.com/personal-finance/refinancing-requirements-what-to-know you’ll get are out of your control. But you can take several steps to ensure you secure the best refinance rate available to you. Here are some to consider:

Save for closing costs

In addition to saving for a down payment, it’s also a good idea to save for closing costs, which can average $5,000, according to Freddie Mac.

Polish your credit

Just as when you bought your home, your credit score and history affect your refinance rate, so it’s a good idea to make sure your credit is in the best possible shape.

Check your credit report for errors, such as incorrect information or duplicated accounts. Pay off as much other debt as you can to improve your debt-to-income ratio, and pay down credit card balances to reduce your credit utilization.

Comparison shop

Just as you’d compare quotes from multiple vendors for an expensive home repair, you should look at loans and mortgage interest rates from multiple lenders. In fact, getting five rate quotes could save you $3,000 over the life of your mortgage, according to a Freddie Mac survey.

What is the average cost of a refinance?

Your exact refinancing costs will depend on multiple factors, including the size of your loan and where you live. Typical refinancing costs include:

- The cost of recording your new mortgage

- Appraisal fees

- Attorney fees

- Lender fees, such as origination or underwriting

- Title service fees

- Credit report fees

- Mortgage points

- Prepaid interest charges

Keep in mind there’s no such thing as a truly no-cost refinance. Lenders who market "no-cost loans" typically charge a higher interest rate and roll the costs into the loan — which means you’ll pay more interest over the life of the loan.

What credit score do you need to get a good 15-year refinance rate?

The ideal credit score to get a good 15-year mortgage refinance can vary. FICO rates credit scores on a range:

- Exceptional — 800 or above

- Very good — 740 to 799

- Good — 670 to 739

- Fair — 580 to 669

- Poor — 579 or below

To get a good 15-year refinance rate for a conventional loan, you’ll typically need a minimum credit score of 620, but this varies by lender. For an FHA rate-and-term or cash-out refinance, you may qualify with a credit score between 500 and 580.

On the other hand, VA loans, FHA Streamline Refinance loans, and USDA loans don’t have minimum credit score requirements.

Lenders also look at factors beyond your credit score when offering a refinance rate, including your debt-to-income ratio — the percentage of your gross monthly income that goes toward paying your debt. Other factors include your loan-to-value ratio (the percentage of your home’s value you plan to finance) and the type of mortgage program.

You can compare mortgage refinance rates from various lenders in minutes with Credible.