Yes, Kinder Morgan Is Still a Buy

The second largest pipeline and energy infrastructure in North America, Kinder Morgan (NYSE: KMI), continues to see its share price languish amid a sector-wide downturn and the gradual reduction of the company's sizable debt load. Despite its size and prevalence in the North American oil and gas pipeline market, its shares have struggled (falling over 40% over the past five years) behind peers such as Enbridge Inc. (NYSE: ENB) and Enterprise Products Partners (NYSE: EPD). Investors have been, rightly, timid about Kinder Morgan ever since it announced in December 2015 that it was reducing its dividend by three-fourths. This blow was once thought to be impossible due to Kinder Morgan's stable cash flow generation.

The market is correct in its assessment that things could be better for KMI, but long-term investors are going to be glad to own Kinder -- maybe sooner than most believe. The situation has continued to improve. Kinder Morgan's shares rightly fell after the dividend cut, which was essentially an admission that the company had become overleveraged. However, these problems are in the process of being corrected, which will lead to a revaluation to historical levels.

Image source: Getty Images.

Recent history

Fourth-quarter results were decent but unspectacular. Revenue fell year over year to $3.39 billion due to the sale of its 50% stake in the Southern Natural Gas pipeline system. However, KMI's balance sheet deleveraging is progressing: Interest expense fell 20% year over year, to $422 million. The first quarter of fiscal year 2017 saw revenue of $3.42 billion, net income of $440 million, and free cash flow of $218 million. Management noted that these figures were above its January guidance. Investors yawned, sending shares down 5% in the two days after the release. Still, free cash flow, the all-important figure for both management and investors, continues to fill the company's coffers. All in all, it was a decent quarter, but investors expecting a quick pop in the shares are likely to be disappointed. Kinder Morgan's recent quarterly results, which arguably left investors underwhelmed, are unsurprising for a company in the midst of the deleveraging process.

Management knows what it's doing

What is now known as Kinder Morgan was formed in 1997, when a group of investors led by businessmen Richard Kinder (the company's current chairman) and William Morgan acquired the general partnership interest in a pipeline then controlled by Enron. Through scores of mergers, acquisitions, and expansions, Kinder Morgan grew to become one of the largest energy infrastructure owner-operators in the U.S., with interests in some 84,000 miles of pipelines and 155 terminals.

Kinder Morgan truly hit its stride in the late 2000s, as the U.S. shale-drilling boom led to an explosion of domestic oil and natural gas production. Producers needed pipelines in order to transport ever-increasing amounts of fuels, and KMI was there to help. Co-founder and current Executive Chairman Richard Kinderstepped down from daily operations in June 2015, and handed the reins off to Steve Kean, KMI's COO at the time, who had been groomed for the role.

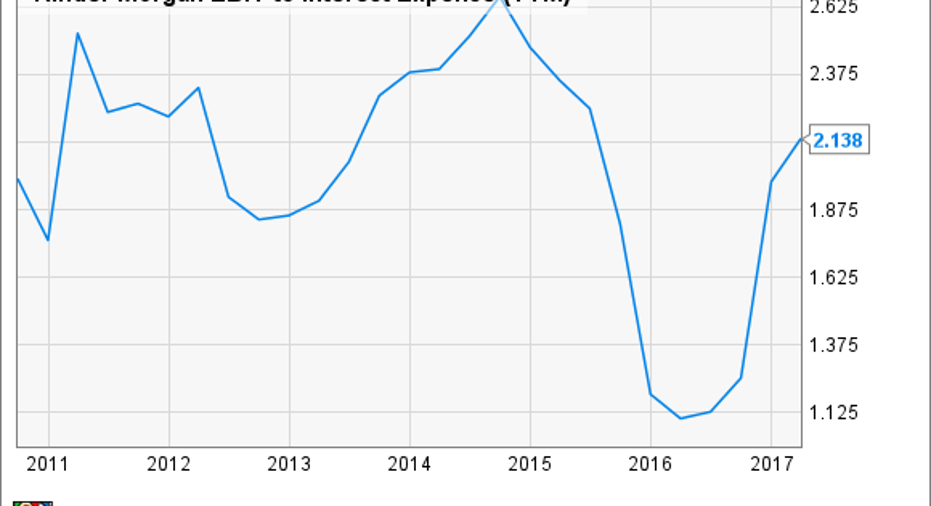

Kean has implemented the company's deleveraging perfectly. The shale boom is arguably over, but the U.S. continues to be a major producer of oil and, perhaps even more so, natural gas. KMI is ideally suited for this reality. The market is simply wondering when KMI's rock-solid cash flow will pay dividends once again. Kinder Morgan's problems stem from overleveraging, not from a fundamental business problem. Its EBITDA-to-interest expense ratio of 2.1 over the last 12 months, compared with Enbridge's 3.9, is just too low. Fortunately, fixing this requires one thing: time.

KMI EBIT to Interest Expense (TTM) data by YCharts.

The company's interest coverage ratios are well on their way to normalizing, and management believes it will even be able to restore KMI's dividend to its former glory by 2018. It appears that KMI's management simply needs a few more quarters to right the ship, but a bright future requires continued growth in commodity markets -- and the kindness of investors.

What the naysayers believe

There are two bear cases surrounding KMI. First, in order to expand and pay dividends, it will always need Wall Street -- making future dividend increases uncertain. Second, commodity prices could always dive again, reducing demand and rates for pipelines. Both are fair points. It may be years before shareholders stop viewing KMI as the dividend stock that got ahead of itself and had to cut its payout. Production of carbon fuels could always fall, thanks to everything from demand drops to price declines. Given the inherent uncertainty of commodity prices, and KMI's dependence on the kindness of strangers (on Wall Street), naysayers no doubt believe that Kinder is undeserving of a premium valuation.

Foolish final thoughts

Detractors have some fair points, and Kinder Morgan probably isn't for every portfolio. However, Kinder Morgan's ability to generate billions in cash flow, even through the downturn in oil and gas production since 2014, will always warrant attention. Natural gas also has a future. Those in the bear camp regarding Kinder Morgan are not unreasonable, but the company's ubiquity in America's energy infrastructure network, coupled with its consistent ability to throw off cash, is just too good to pass up. Interest coverage ratios will normalize in the second half of 2017, and management expects to have more than enough resources to expand, continue to repurchase shares, and increase KMI's payout. Foolish investors looking for a beaten-down stock, experiencing what is arguably self-inflicted and short-term problems, would do well to give Kinder consideration. Management is top-notch, and it's not often one can buy a regulated monopoly for a song.

10 stocks we like better than Kinder MorganWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Kinder Morgan wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Sean O'Reilly has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Enbridge and Kinder Morgan. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.