Williams Companies, Inc.'s Best Move in 2015

Williams Companies' initial strategic plan to drive growth was to combine with its master limited partnership,Williams Partners , to form a formidable energy infrastructure C-Corp. However, rival Energy Transfer Equity had a better idea and repeatedly asked Williams to join its family instead. After reviewing all its options and seeing the worsening of the energy markets, it relented after realizing that becoming part of the largest energy midstream franchise in the world was a better idea, especially in a business where scale matters. It's by far the best move the company made in 2015.

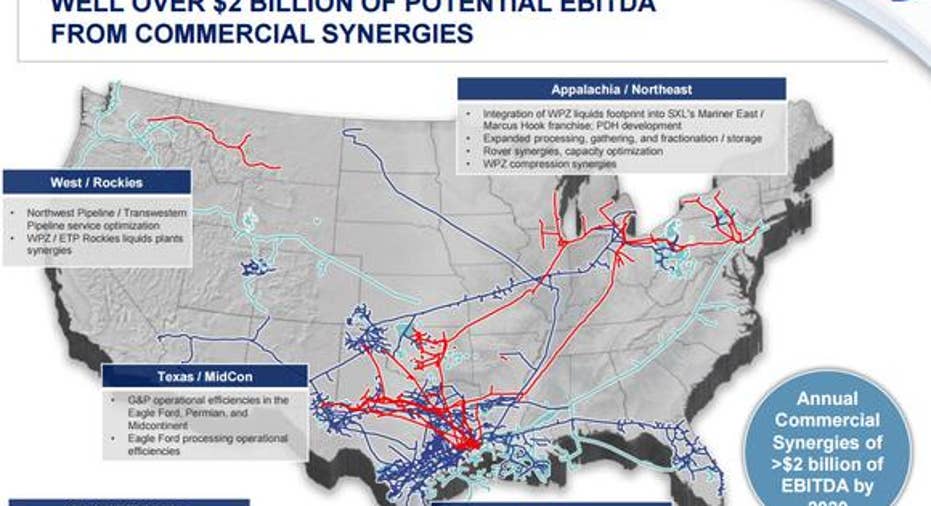

Sizing up the opportunityThe Williams-Energy Transfer Equity combination has very real scale advantages that are clearly visible on the horizon. Energy Transfer Equity has already identified a significant amount of commercial synergies that will now be possible including new revenue opportunities, improved operational efficiently, new capital opportunities, and the prioritization of existing capital projects.

Data source: Williams Companies investor presentation.

The companies have already identified $5 billion of incremental capital investments that can be made resulting from the combination. These investments are expected to generate more than $2 billion of annual EBITDA by 2020, or 20% of the company's current EBITDA.

On top of that, the Energy Transfer Equity sees material costs savings and synergies of more than $400 million on an annualized basis for Williams Partners once it joins the company's shared service model. In addition to that, there are some less visible opportunities, including asset transfers between Energy Transfer Equity's other entities that could further improve operational synergies at Williams Partners and drive incremental growth.

Why scale mattersThe potential beyond what is clearly visible could be even greater. Once the deal closes in 2016, Energy Transfer Equity will be one of the top five largest global energy companies. That size enables it to participate in projects that are beyond the capability of its smaller rivals. In other words, it opens up new doors for future growth that wouldn't have been possible if Williams remained independent.

For example, Williams has a small but growing chemicals group that benefits from low commodity prices. The company's primary petrochemical asset is its Geismar plant, which produces both ethylene and polymer grade propylene. It's a business that the company would like to continue growing, with plans for a Geismar 2 plant as well as two PDH plants that make polymer-grade propylene. However, with its larger scale it could now undertake a real word-scale chemicals project that it might not have had the capabilities to undertake prior to the combination.

Thanks to cheap shale gas, petrochemical expansion opportunities abound, but the price tag can be quite hefty. Dow Chemical for example, is in the midst of a $4 billion expansion project that will boost its capacity to make the chemical building blocks ethylene, polyethylene, and propylene, which are key to making plastics and other products. Among Dow Chemical's projects is a $1.7 billion ethylene cracker. Meanwhile, South African energy and chemicals giant Sasol is moving ahead with an $8.1 billion cracker plant that will make ethylene. The Sasol plant is a much larger-scale plant than the one Dow Chemical is building, which shows the potential size of a plant that Williams will have the scale to pursue. With such an abundance of shale gas, the U.S. is poised to become a petrochemical powerhouse, which could open a whole new growth platform for the Williams-Energy Transfer Equity family.

Investor takeawayWilliams Companies' decision to merge with Energy Transfer Partners has the potential to pay off down the road as the energy industry recovers. Not only can the companies capture significant synergies by combining assets today, but the greater scale will enable them to capture new opportunities that will appear due to lower prices. The most compelling of which are large-scale, demand-driven projects such as those being built by petrochemical companies. Those are projects that would have likely been out of Williams' reach but now could be.

The article Williams Companies, Inc.'s Best Move in 2015 originally appeared on Fool.com.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool recommends Sasol. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.