Will Lower Production Lead to the Turnaround These Shale Producers Desperately Need?

A year into the oil bust, and prices haven't improved. They've gotten worse.

Where can an energy sector investor look for hope?

The answer is the Energy Information Agency's (EIA) monthly Drilling Productivity Reports which are forecasting a very steep drop in U.S. shale production. The cumulative decline in production that the EIA believes is now taking place in the U.S. shale industry may be enough to impact global oil prices, which would go a long way to help US producers such as Continental Resources and EOG Resources .

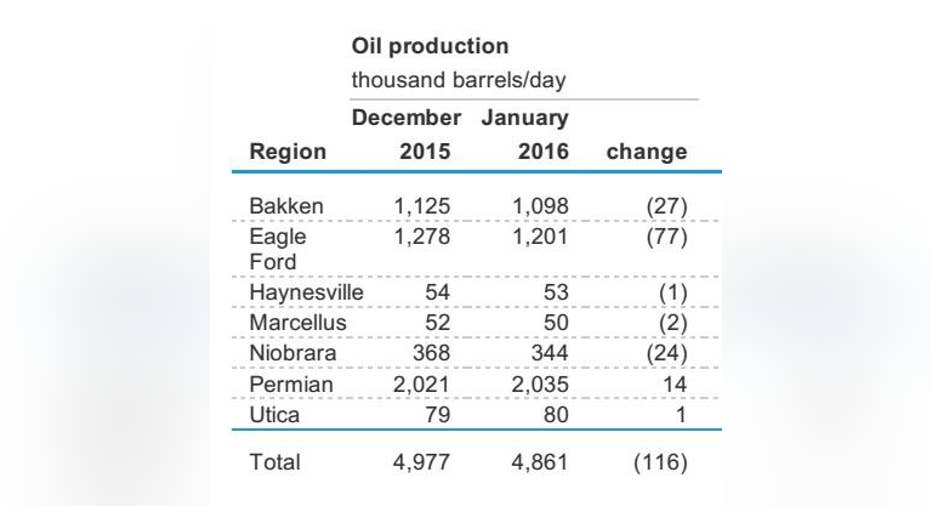

The EIA View-Shale Production Is Rolling Over HardThe EIA just released the January 2016 version of the Drilling Productivity Report. This is a forward-looking report that forecasts where production is going from the major U.S. shale plays. Here's what the EIA thinks is going to happen to U.S. shale oil production in January:

Source: US Energy Information Administration

The EIA is calling for a January decline in U.S. shale production of 116,000 barrels per day. That's a big drop for just one month, and it follows drops that they EIA believes started in October:

- October: shale production down 72,000 barrels per day.

- November: shale production down 83,000 barrels per day.

- December: shale production down 105,000 barrels per day.

- January: shale production down 116,000 barrels per day.

With the way real-time oil reporting data works, the market really doesn't know for certain what has happened until several months after the fact. If October production was the real kickoff of the shale production declines, the market is really just going to start seeing that in the weeks ahead. It is possible that the market is fully aware of these Drilling Productivity Reports and simply doesn't believe them. It may take verification from those delayed actual numbers for the accelerated shale decline (if true) to impact oil prices.

The EIA believes shale production peaked in March at 5.48 million barrels per day. For January, the EIA sees that production level going all the way down to 4.86 million barrels per day.

The Drop In Cash Available For Drilling Is IncredibleIf shale production is really going to slide starting in Q4 2015, then we should be able to see it in Continental Resources and EOG Resources' results

Looking at Continental Resources'third-quarter 2015 earnings reportdoes provide some useful information. Production for Continental was 228,278 boe per day. In the press release, Continental provided 2015 exit production guidance of 210,000 boe per day. That's a drop of 18,000 barrels per day quarter on quarter, or 8%.

Drilling into Continental's cash flow statement clearly shows why the company has had to throttle back on drilling. In the first nine months of 2014 Continental generated $2.3 billion of cash flow. This year that number has dropped by 40% to just $1.4 billion. Despite that, through the first nine months of 2015 Continental spent $2.6 billion on capex which is $1.2 billion or almost twice as much cash as the business generated.

That spending in excess of what cash flows from the business generated was funded by debt. So far in 2015 Continental's long term debt has increased by $1.1 billion. The reason that Continental's production has held up as well as is due to the company living well beyond its means. Continually adding debt in this low price environment is not a sustainable strategy. That is likely why Continental indicated in its third quarter earnings release that plans to balance cash flows with debt going forward.

EOG Resources meanwhile hasn't yet shown a decline in production, but a closer look at its cash inflows and outflows are revealing.

Early on in the oil price collapse EOG stated that it had no interest in growing production into a depressed oil price environment. When you consider how front-end loaded production from shale wells are that is a strategy that makes a lot of sense. Since a large percentage of the oil that will ever be recovered by a shale well happens in the first year of its life it is important that those barrels are recovered at a sufficient oil price.

While EOG is considered the "best in class" independent shale producer, when you drill into the numbers you can see that EOG is burning a lot of cash, too. Through the first nine months of 2015 EOG generated $2.9 billion in cash flow but spent $4.5 billion in capex. EOG's debt only increased by $400 million, but the company's cash balance has dropped by more than $1.2 billion during the year. While outspending cash flow by $1.6 billion EOG has only managed to keep production "flattish".

Both EOG and Continental spent more in the first quarter than they did in Q2 and Q3. EOG's capital spending split was ($1.8 bil, $1.0 bil and $1.7 bil) while Continental was ($1.2 bil, $700 mil and $700 mil). While there is no exact science to it, with the general lag between a well being drilled and when it is fracked and completed it would make sense that the lower Q2 on spending is only impacting production in late Q3 and into Q4.

Growing debt while not growing production is not a successful long term planIf companies like EOG and Continental are going to stop allowing their balance sheets to deteriorate and start to live within cash flow at current oil prices; it is going to be challenging. As we roll into 2016 things are only getting tougher. Oil hedges that were put on at much higher prices for most companies are expiring and cash flows that are already depressed are going to get worse.

This should further pressure production for all of these companies and help contributed to balancing daily oil supply and demand. The shale boom has been incredible but we can't forget that it took high oil prices to unleash it. Without those high oil prices the shale boom is going to become more of a whimper.

The article Will Lower Production Lead to the Turnaround These Shale Producers Desperately Need? originally appeared on Fool.com.

Chritopher Malcolmhas no position in any stocks mentioned. The Motley Fool owns shares of EOG Resources, Inc.. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.