Why Under Armour, Inc. Shareholders Have Something to Worry About

The ground is shifting below Under Armour's (NYSE: UA) (NYSE: UAA) cleat-studded feet. An awesome streak of market-thumping sales and profit growth was interrupted when shareholders in the past year witnessed both a significant downgrade of the long-term earnings outlook and the lowering of management's revenue expectations. That one-two punch recently pushed shares down to a three-year low.

That stock price slump reduces the risk of additional big declines ahead. But investors should still be concerned about the weakening business fundamentals -- and whether the sports apparel retailer has the right plans in place to address them.

What went wrong

Under Armour's struggles really started in the second half of 2016, when CEO Kevin Plank and his executive team stepped away from their long-term profit forecast. Less than a year earlier, management had projected a doubling of annual operating income to $800 within three years. By late October, though, it was clear that this target was too aggressive.

Image source: Getty Images.

Under Armour explained that the U.S. market was showing surprising weakness, which was forcing the company to sacrifice profit margins to stay competitive. That was bad news, but not a huge surprise. Rival Nike (NYSE: NKE) was dealing with the same profitability struggles and inventory overhang in the U.S. that ultimately contributed to its finishing dead-last among the 30 members of the Dow in 2016 stock performance.

Importantly, Under Armour believed its long-run sales growth forecast was still achievable heading into the holiday quarter, since executives saw faster gains in international markets and in categories like footwear balancing out the slight slowdown in the domestic apparel market.

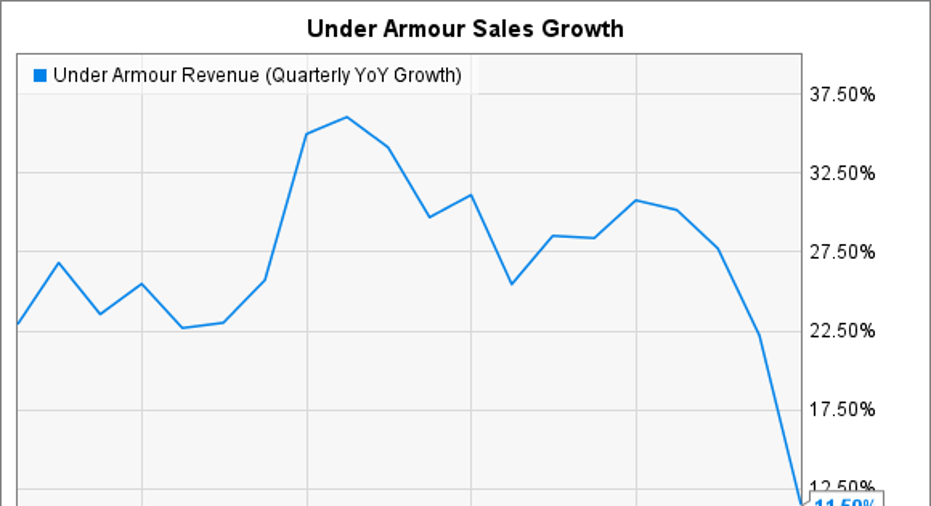

UA Revenue (Quarterly YoY Growth) data by YCharts.

That sunny outlook was wiped out a few months later when Under Armour in late January posted its first quarter of sub-20% sales growth in nearly seven years. Now, rather than growing at the roughly 22% annual pace it had expected through 2018, the retailer projects gains of just 12% this year even as gross profit margins continue to decline.

Where Under Armour goes from here

Executives believe they have a firm grasp on what went so wrong over the holiday quarter, and it boils down to a poorly targeted product portfolio. Its apparel and footwear offerings weren't innovative or fresh enough to stand out from the competition. And, where the products did capture market share, in many cases, it was on the lower end of the market, which hurt profit margins both for Under Armour and its retailing partners.

The major task at hand involves shifting the product development and selling strategies to keep the company firmly on the premium side of the industry across all of its categories. As the fastest-growing brand in the U.S. industry for the past two decades, the brand clearly has strength that Under Armour can lean on to recover sales momentum.

Yet competition is likely to hurt the company more than rivals. With 85% of its business coming from the U.S. market, Under Armour is significantly more exposed than Nike, which generates just 50% of revenue domestically.

Plank called the current business environment an "inflection point" that offers the company an opportunity to build a better foundation for profitable growth in the U.S. while continuing to invest in attractive categories like footwear, wearables, and international expansion. "Our growth story is intact," he argued.

The good news is that expectations have come way down to give management room to make big tweaks to its strategy while still hitting broader targets. But investors will want to see progress through the year to back up Plank's claim that this slowdown isn't a threat to its broader market or profit potential.

10 stocks we like better than Under Armour (C shares)When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Under Armour (C shares) wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

Demitrios Kalogeropoulos owns shares of Nike and Under Armour (A shares). The Motley Fool owns shares of and recommends Nike and Under Armour (A and C shares). The Motley Fool has a disclosure policy.