Why Tronox Shares Jumped 30% in February

Lately, titanium dioxide manufacturerTronox(NYSE: TROX) has been flying high. Along with other TiO2 companies likeChemours(NYSE: CC) and Kronos Worldwide (NYSE: KRO), the company had a stellar 2016. Tronox shares rocketed up 146.7% last year as the TiO2 market finally started a long-overdue recovery.

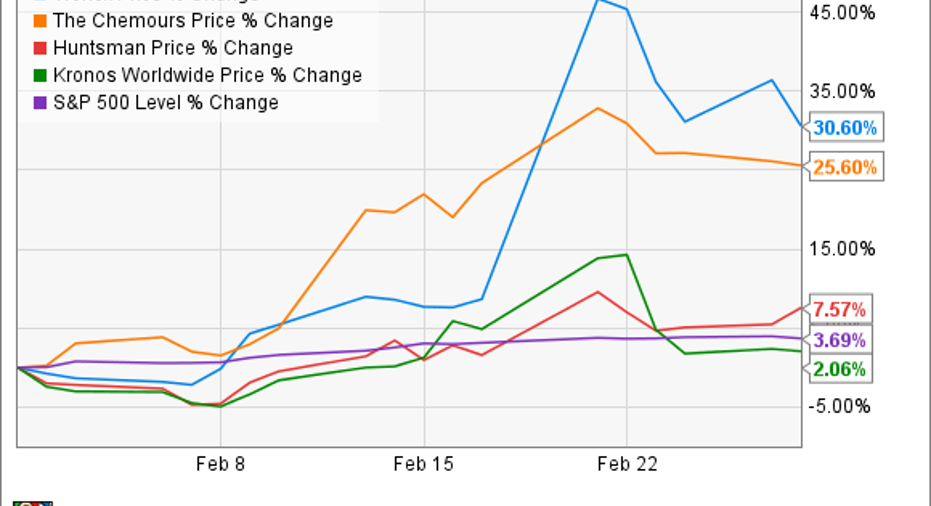

But in February, Tronox shares again soared higher, to the tune of 30.6%. Here's why.

Titanium dioxide's primary use is as a white pigment in paints. Image source: Getty Images

What happened

This time, it wasn't a case of a rising tide lifting all boats: Tronox's performance clearly outpaced its TiO2 rivals':

Only Chemours -- which rose higher on the news that it was settling a series of lawsuits unrelated to its TiO2 operations -- came close to matching Tronox's performance.

Almost all of Tronox's gains came on the heels of its earnings report on Feb. 21, when it reported stronger-than-expected sales, although it still reported an adjusted earnings loss. At the same time, the company announced it planned to sell its alkali business to acquire the privately held TiO2 company Cristal. That deal would create the largest TiO2 pigment supplier in the world.

So what

Tronox's comparatively strong fourth quarter further strengthens the thesis that the TiO2 markets are marching toward a long-term recovery. Tronox CEO Tom Casey said as much in the company's earnings release:

So, it stands to reason that buying a competitor to create the largest supplier of an in-demand commodity is a smart business decision. The new company will haveassets and operations on six continents, including 11 TiO2pigment plants in eight countries with a total annual capacity of 1.3 million metric tons. That will indeed dethrone industry leaderChemours, which currently has annual production capacity of 1.25 million metric tons of the chemical.

The trouble with Tronox

Before you rush out to buy shares, though, you should know that it's not all sunshine and roses at Tronox. The company has posted net losses for each of the past three years, and while 2016's net loss was far smaller than the prior year's, the company still isn't profitable.

The balance sheet, meanwhile, is frightening, with just $248 million in cash and an eye-popping $2.9 billion in debt.About the only bright spot on this front is that the acquisition of Cristal is not expected to add any debt, but it will be funded instead through asset sales -- including the sale of the alkali business -- and Class A stock shares.

Investor takeaway

While the acquisition of Cristal is probably a smart move for the company -- and the timing is particularly good -- Tronox is still a struggling company with a nightmare of a balance sheet. Not to mention, the sale of the alkali business means Tronox will become a one-trick pony, completely dependent on -- and subject to -- the whims of the global titanium market.

While that titanium market is on an upswing, so are Tronox's fortunes, but the underlying issues with the company -- loads of debt, plenty of competitors, and chronic unprofitability -- should convince investors to look elsewhere.

10 stocks we like better than TronoxWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Tronox wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

John Bromels has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.