Why Rising Gold Prices Aren't Helping Freeport-McMoRan Inc.

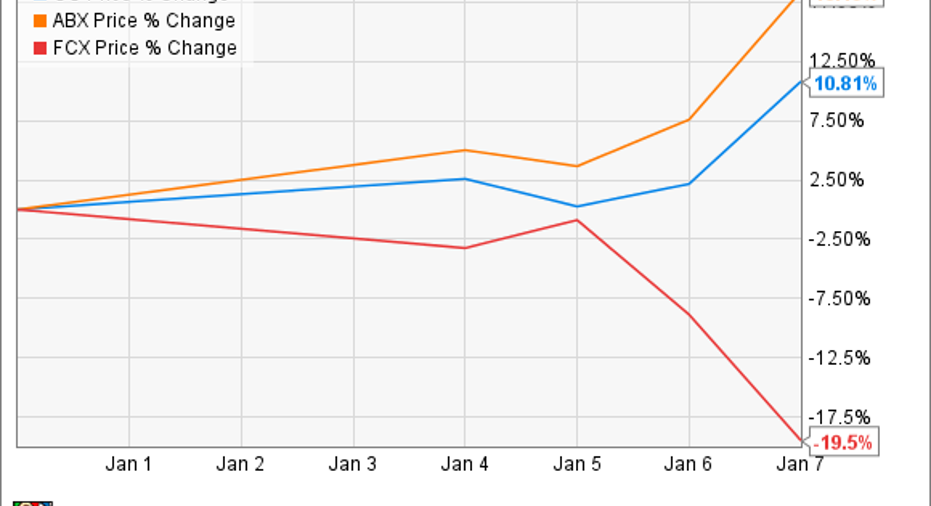

Prior to its now ill-fated move to diversify into oil and gas, Freeport-McMoRan was known as Freeport-McMoRan Copper & Gold. That was due in large part to the fact that those two commodities were the primary drivers of its business. The company's gold production, however, has become an afterthought in recent years. Not only had the price of gold fallen quite dramatically, but Freeport has focused on growing its copper and oil production. That said, with global economic jitters recently roiling the market, it sent the price of gold up by more than $50 an ounce to just over $1,100 per ounce in just a few trading days. That sparked a rally in gold stockswith miners likeGoldcorp and Barrick Gold bounding higher. It's a rally, however, that Freeport-McMoRan hasn't joined:

Here's why the recent gold price rally isn't helping Freeport.

Golden cash flows Commodity producers are highly levered to the price of the commodities they produce. For example, in Goldcorp's case, every $100-per-ounce change in the price of gold from the $1,200-per-ounce level results in a $267 million change in free cash flow on an annual basis. To put that into perspective, Goldcorp was estimated to produce roughly $1.5 billion in operating cash flow in 2015, so the recent rally implies that its cash flow won't trail off quite so steeply in 2016 as it would have if gold remained lower. Barrick Gold's free cash flow, on the other hand, would change by $79 million on an annual basis for each $100 change in the price of gold from the $1,125-per-ounce level. For a company that produced $866 million in free cash flow last quarter, the recent change in the price of gold would still have a meaningful impact on 2016 cash flow if it holds.

Unfortunately for a more diversified company like Freeport-McMoRan, the recent rally in the price of gold is just a drop in the bucket.

Starting from a bad baseOn the following slide, Freeport-McMoRan projects its potential cash flow and EBITDA in 2016 and 2017 based on a range of copper prices, because copper is its main driver of cash flow:

Data source: Freeport-McMoRan investor presentation.

While it projected a range of copper prices, it kept the price of its three other commodities locked in at $1,200 for gold, $6 for molybdenum, and $56 for oil. At the moment, those prices all look way too bullish given that gold is currently $1,100 an ounce while molybdenum is $5.50 a pound, oil is $32 per barrel, and copper has recently fallen below $2 per pound.

Those prices, should they hold through the year, would have a significant impact on the company's cash flow given its current sensitives, which are detailed on the slide below:

Data source: Freeport-McMoRan investor presentation.

As that slide notes, every $50 change in the price of gold is worth $65 million to its cash flow. So, while gold has rallied that much to start the year, it's still $100 per ounce below the company's baseline projection. What that means is that if the current gold price holds Freeport's cash flow will be $130 million less than projected, and that's if all the other commodities were to rally back to its initial projections. In fact, given where things stand right now, its cash flow will be roughly $1.5 billion less than what's projected on that first slide. To put that into perspective, for a gold price rally alone to make up the difference it's price would need to nearly double. Needless to say, that's unlikely to happen.

Investor takeawayWhile Freeport-McMoRan is a diversified resource company, its main cash flow drivers are copper and oil, not gold. That's why it's stock isn't joining the gold-miner rally this year. Instead, its sinking along with copper and oil prices, which seem to have fallen in a bottomless pit in 2016.

The article Why Rising Gold Prices Aren't Helping Freeport-McMoRan Inc. originally appeared on Fool.com.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool owns shares of Freeport-McMoRan Copper & Gold. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.