Why Lower Taxes Could Cost Citigroup $13 Billion

How is it possible that lower taxes might cost Citigroup money? Image source: iStock/Thinkstock.

One of the cornerstones of the incoming Trump administration's economic policy is to cut corporate income taxes, which analysts believe could drop from a maximum rate of 35% today down to 25%. But while this would increase profits at most companies, a handful of the nation's biggest banks would also see a downside, and none more so than Citigroup (NYSE: C).

Citigroup's deferred tax assets

You have to go back to the financial crisis to understand why this is the case. In 2008, the low point, Citigroup recorded a pre-tax net loss of $52.4 billion. Things improved the following year, but the bank nevertheless suffered a $7.8 billion pre-tax loss in 2009.

This matters today because the magnitude of Citigroup's losses in those two years was so substantial that the bank didn't have enough income in either year to claim the entirety of the losses as deductions. It therefore elected to carry the losses forward by way of deferred tax assets, which allow it to use the losses from 2008 and 2009 to offset income in the future for the purposes of income taxes.

This is what Citigroup has done ever since. Last year, for example, it used $1.5 billion worth of its deferred tax assets to reduce its income tax liability. It's even been suggested that this was why Citigroup, working in tandem with Visa, could underbid American Express for the exclusive right to issue credit cards to Costco customers.

The problem for Citigroup, however, is that it has a limited amount of time in which it can use these assets before they expire -- they're currently valued at $45.4 billion. As of its latest 10-K (see page 122), its most comprehensive annual regulatory filing, roughly a third of the assets consist of foreign tax credits and must be used within 10 years of their creation. The remainder, domestic tax credits, last twice as long.

This means that Citigroup must generate an enormous amount of qualified income over the coming years to absorb the deferred tax assets, something the bank feels confident it can do -- or at least it did at the end of last year. According to its 2015 10-K:

With this in mind, the problem with a reduction in the top corporate income tax rate is that it will reduce the amount of taxes Citigroup would otherwise have to pay. It would thus take longer for the bank to work through its deferred tax assets. And if it takes too long, then it could cause a portion of the assets to expire.

A $13 billion writedown?

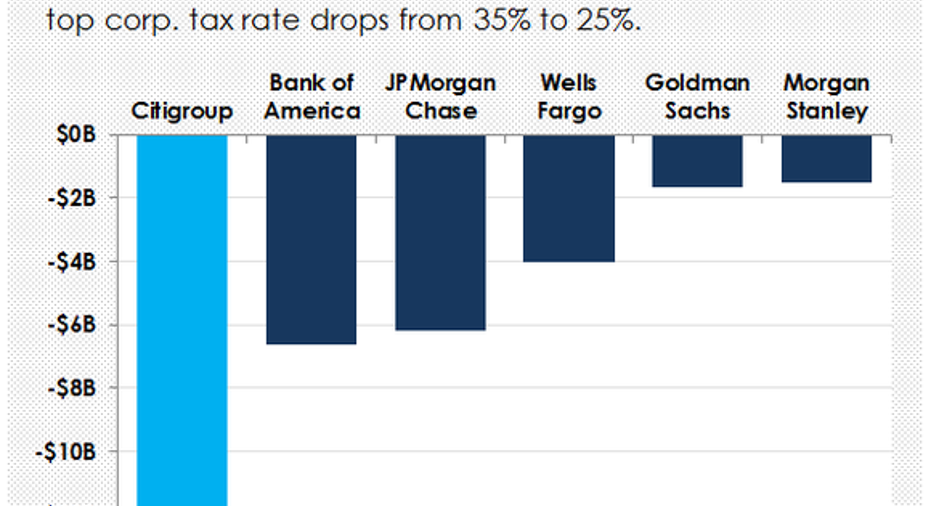

This is essentially what analysts at Keefe, Bruyette & Woods predict will happen. It released a report at the end of last month that gauged the impact of a corporate income tax reduction on the value of deferred tax assets at a handful of the nation's biggest banks. According to KBW's math, the change could lead to a one-time $13 billion drop in the value of Citigroup's deferred tax assets, which would have to be written off next year (assuming taxes are lowered in 2017).

Data source: Keefe, Bruyette & Woods. Chart by author.

This would have a big impact on Citigroup's tangible book value, which dictates its share price. KBW estimates that the write-off would cause the bank's tangible book value to fall by $12 billion. This helps explain why Citigroup's shares trade for the lowest multiple to tangible book value among large-cap bank stocks.

The good news is that Citigroup's earnings per share would thereafter increase, seeing as though it would face a lower effective tax rate. KBW estimates that this would boost Citigroup's earnings per share in 2018 (the year after the tax cut) by 7.3%. In other words, there is a silver lining to this story.

In sum, while there's no question that the incoming administration's tax proposals would provide a boost to corporate earnings, it's important for bank investors to appreciate that they would also trigger a one-time hit to the value of bank balance sheets and Citigroup's in particular.

10 stocks we like better than Citigroup When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Citigroup wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

John Maxfield has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Costco Wholesale and Visa. The Motley Fool recommends American Express. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.