Why Kinder Morgan Is Still the Best Pipeline Stock Despite Its Low Yield

Image source: Getty Images.

It has been a long road forKinder Morgan (NYSE: KMI)since it decided to cut its dividend a year ago. The fateful decision was not made lightly, and was only made out of prudence-- when a company cannot count on capital markets to fund intrinsicallyprofitable expansions, it must live within its means. The bond market was tightening up amid a major secular downturn in the oil and gas industry, and Kinder Morgan had a substantial backlog of profitable projects. It would have been irresponsible not to try to remedy the situation. However, that doesn't soothe the pain of the cut.A year later, shareholders now sit more or less where they were in late 2015, wondering when the dividend will return to its previous level and if it was all worth it. While it's extremely difficult to think long term while bathing in a sea of red ink, Kinder Morgan's shareholders can feel assured that the future is bright. As I will show, Kinder Morgan is the ideal pipeline operator for investors to own heading into the new year.

Valuation

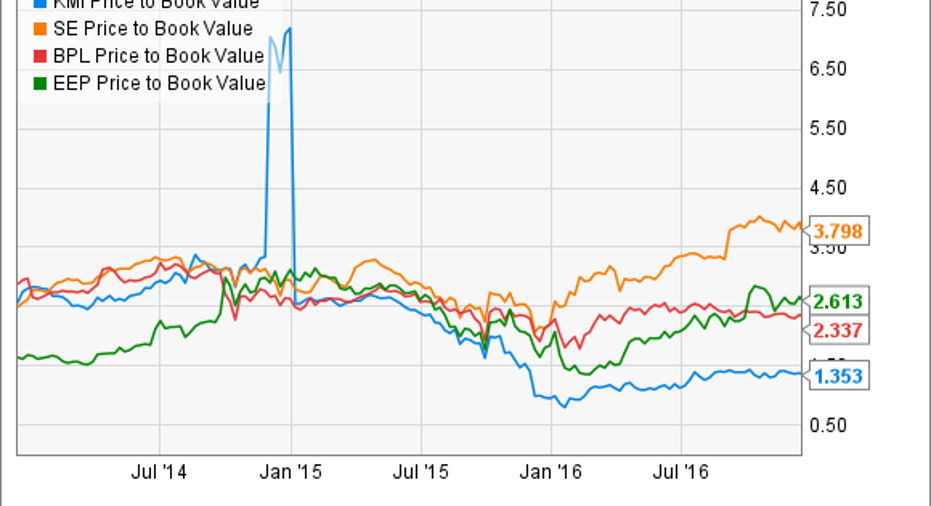

Kinder Morgan happens to be one of the few premier midstream oil and gas operators in the United States. Its peers include companies like Spectra Energy (NYSE: SE), Buckeye Partners (NYSE: BPL), and Enbridge Energy Partners (NYSE: EEP). While there are obviously a few differences between these and other companies in the space, it is extremely valuable to note that Kinder Morgan trades at a sizable discount to its peers in terms of its book value:

KMI Price to Book Value data by YCharts.

Over the past five years, according to data from S&P Global Market Intelligence, Kinder Morgan has traded at an average of 2.87 times its tangible book value. This figure is in line with the valuation assigned to its peers, as seen above. Obviously, Kinder Morgan currently trades at a discount because of its year-old dividend cut and concerns over its balance sheet, but once the company normalizes its payout, the valuation assigned to its shares will normalize -- and likely reward patient shareholders in the process.

Which leads to my next point: Kinder Morgan cut its dividend in order to fund its capital budget -- and this move will almost certainly bear fruit in the years ahead.

Thinking long term

It is difficult to see past the present day, but it is highly likely that in five years shareholders won't remember the difficulties that Kinder Morgan is going through now. The dividend will have normalized. As a result, a reasonable price-to-book multiple will have been assigned to its shares. And the multitude of projects that are currently in progress will begin to send excess cash flow to the company's headquarters.This is what the reduced dividend is "buying "shareholders. According to arecent announcement, the company plans to spend $3.2 billion next year for expansions of its network. Once these initiatives are paid for, the company expects to increase its dividend in fiscal year 2018. This is all occurring while the company slowly works to complete its $13 billion project backlog. The importance of this promise of future growth cannot be understated. This backlog includes a recently approvedmassive $5.4 billion pipeline system that will transportheavy crude from the oil sands in Alberta, Canada, to Vancouver's ports on the Pacific coast.

What a Fool believes

Shareholders of Spectra Energy and Buckeye Partners will certainly do well in the years ahead. After all, it's hard to argue with a current 5% dividend yield. However, shares in these companies are priced to reflect the expectation of good times ahead. But it seems highly likely that investors willing to wait patiently as Kinder Morgan works through its product backlog, and pays for these projects with current cash flow (which, to its credit, will not require tapping the capital markets for a single cent), will be rewarded.

10 stocks we like better than Kinder Morgan When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Kinder Morgan wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Sean O'Reilly has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan and Spectra Energy. The Motley Fool recommends Enbridge Energy Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.