Why Is Bank of America a Global Systemically Important Bank?

Bank of America's headquarters in Charlotte, North Carolina. Image source: iStock/Thinkstock.

If you follow Bank of America (NYSE: BAC), then you may know that it's considered by regulators to be one of eight U.S.-based global systemically important banks, or G-SIBs. This matters because it impacts the amount of capital Bank of America has to hold, which weighs directly on its profit.

The Federal Reserve, in the middle of last year, finalized the rule that implements the so-called G-SIB capital buffer, which is unique to each G-SIB. In Bank of America's case, this means that it will have to hold 3% more capital than non-G-SIB banks once the rule is fully phased in two-and-a-half years from now.

This isn't as bad as JPMorgan Chase (NYSE: JPM), the nation's biggest bank by assets, which originally faced a 4.5% G-SIB buffer, but has since whittled that down to 3.5%. But it's nevertheless meaningfully higher than one of Bank of America's main competitors in the commercial banking space, Wells Fargo (NYSE: WFC), which faces a 2% G-SIB buffer.

The rule itself does two things. First, it explains why certain banks are classified as G-SIBs. And second, it reveals how the size of a particular bank's G-SIB buffer is calculated.

To determine whether a bank is a G-SIB, the Federal Reserve scores institutions with at least $250 billion worth of assets on their balance sheets according to "five broad categories that are correlated to systemic importance":

- Size

- Interconnectedness

- Substitutability

- Complexity

- Cross-jurisdictional activity

If a bank's score is above a certain threshold, then it's considered by the Fed to be a G-SIB, and thus subject to higher capital requirements. Seven banks, in addition to Bank of America, made the cut:

- JPMorgan Chase

- Bank of America

- Wells Fargo

- Citigroup

- Goldman Sachs

- Morgan Stanley

- Bank of New York Mellon

- State Street

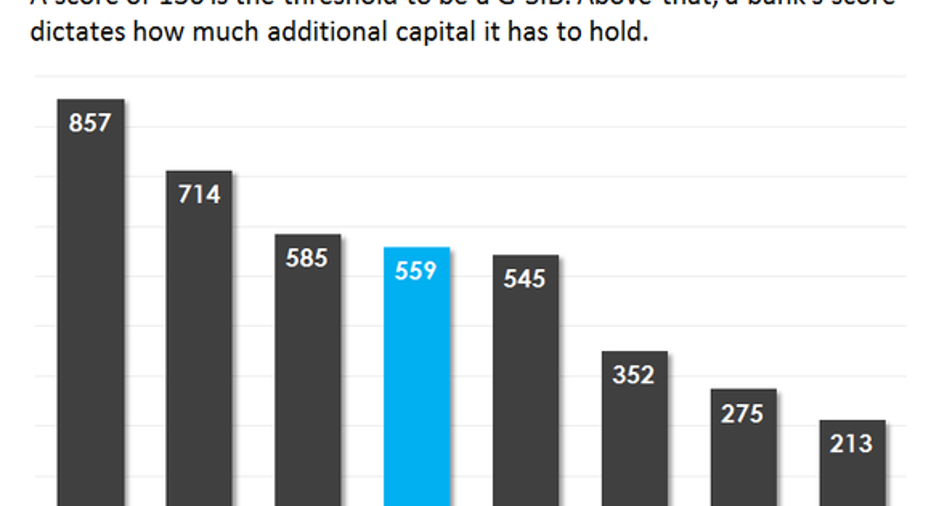

The same score, or a close variation thereof, is then used to calculate a bank's capital surcharge, with higher scores corresponding to higher surcharges. In last year's inaugural version, Bank of America earned a score of 559, ranking it right in the middle of the pack.

Data source: The Federal Reserve.

Bank of America scores high in all five categories. This is due not only to its sheer size, but also to the composition of its businesses -- its trading units, in particular. Based on the Fed's definition of the five categories, as well as the fact that many trading operations rely on short-term funding sources, which similarly factor into the Fed's equation, a bank with a sizable trading operation is destined to face a high G-SIB surcharge.

The takeaway for Bank of America investors is that, nowadays, its size and complexity is almost as much of a burden as it is a benefit.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

John Maxfield owns shares of Bank of America, Goldman Sachs, and Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.