Why I'm Bullish on 3M But Not Chemours

Chemical companies' mistakes can cause problems decades down the line. Image source: Getty Images.

It's not easy being a chemical company these days, especially not a chemical company with a long history. And both3M (NYSE: MMM) andChemours(NYSE: CC) fall into that category.There's one particular chemical that's causing looming legal headaches for both companies right now -- however, 3M is better equipped to weather the storm than Chemours. Here's why.

A long and bumpy road

3M was founded in 1902, andDuPont(NYSE: DD) -- which spun off Chemours in 2015 -- is exactly 100 years older. Either way, that's plenty of time to make mistakes that have unintended consequences for your company down the line. And when those mistakes involve chemicals, they can be costly.

A company can use a chemical or substance for years, even decades, before its harmful effects become apparent. Take asbestos, for example. Asbestos is a naturally occurring fibrous mineral that is both strong and heat-resistant. As a result, it was used for decades in building materials, fabrics, and automotive parts.

It wasn't until the 1970s that it became apparent that asbestos was hazardous to human health. The strong, rigid fibers are easily inhaled, and can cause damage to the lungs, or even mesothelioma, a rare and aggressive cancer.

Both 3M and Chemours are facing asbestos-related lawsuits. At the time it was spun off from DuPont, Chemours was facing about 2,400 of them. But 3M, which manufactured a disposable respirator that allegedly failed to filter out asbestos particles, has had more than 300,000 lawsuits filed against it, for more than $300 million in damages.

But that's just a drop in the bucket compared to the potential liabilities for both companies from a chemical called PFOA.

PFOA spells trouble

PFOA is a chemical compound that 3M manufactured and that was used in the production of DuPont's (now Chemours') Teflon products for decades.Additionally, while it didn't contain PFOA, 3M's original formula of ScotchGard broke down into PFOA.

Recent studies have established a "probable link'' between PFOA and several serious health conditions, including cancer and thyroid disease.PFOA has been found in the bloodstreams of people and animals around the globe.

As of the end of 2015, DuPont estimated it was facing approximately 3,500 PFOA-related lawsuits. The first two of these to go to trial,Bartlett v. DuPont andFreeman v. DuPont,resulted in a combined $7.2 million in judgments against the company. DuPont is, of course, appealing both cases, but if this kind of multimillion-dollar judgment against the company becomes the norm, costs could easily skyrocket into the billions.

That's bad for Chemours, which -- as part of its spinoff from DuPont -- agreed to indemnify DuPont for "uncapped amounts" in all PFOA-related matters.And there are two new PFOA class action lawsuits against DuPont coming up in November 2016 and January 2017.

3M has a pair of PFOA lawsuits of its own to contend with. In June and September, two separate PFOA class action lawsuits were filed against the company in Pennsylvania and Alabama.

Why 3M is in better shape

Nobody -- not DuPont, not Chemours, not 3M -- knows how much money PFOA litigation will cost the companies."[A]range of such liabilities, if any, cannot be reasonably estimated at this time" noted DuPont in its 2015 10-K. If very low levels of PFOA in people's bloodstreams are found to be hazardous, the combined companies could be on the hook for a lot of money in damages.

But 3M is in the best shape to weather any potential financial difficulties resulting from these lawsuits. The company is far larger than Chemours, with annual revenue of $30.3 billion compared to $5.7 billion.It's alsoprofitable, with solid cash flowandsports a robust R&D pipeline, spending5.7% of its net sales on R&D, with fully a third of the company's sales coming from products invented in the last five years. And while it has been taking on debt to finance share buybacks and its dividend, on the whole its balance sheet is strong.

Chemours' balance sheet, on the other hand, is an absolute mess. WhenDuPont spun off Chemours, it loaded up the new company with five times its EBITDA in net debt -- about $4 billion -- as well as numerous environmental cleanup liabilities and, of course, the aforementioned PFOA and asbestos liability.At the end of Q2 2016, the company still had $3.8 billion in long-term debt and only $383 million in cash on hand.It also sports a paltry 0.8% current dividend yield, and spends a meager 1.6% of its sales on R&D.

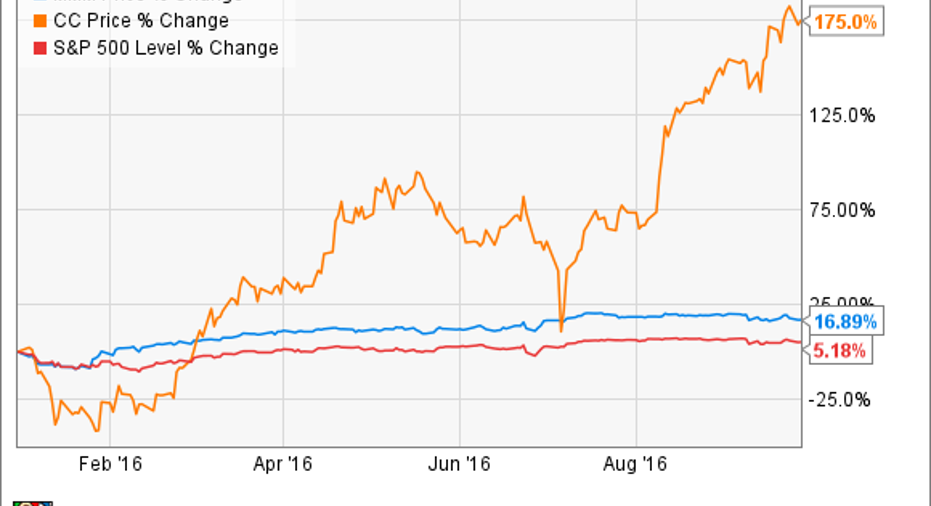

In spite of all this, Chemours' stock has had an incredible run this year (after a terrible 2015), while 3M's performance has been merely good:

Investor takeaway

PFOA litigation is a headache that isn't going away anytime soon for any of the companies that were involved in its manufacture. And it carries serious risks for investors, given the potential amounts of the damages that might be awarded to the numerous plaintiffs.However, the risk is far higher for Chemours investors than for 3M investors.

Chemours investors may want to take this opportunity to sell the stock after its recent run-up but before the next round of PFOA class action litigation begins in November. Perhaps they might be interested in buying 3M, with its strong balance sheet and 2.5% current dividend yield.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

John Bromels has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.