Why DryShips Inc. Stock Growth Is No Sure Thing

When DryShips (NASDAQ: DRYS) reported its first-quarter results earlier this month, the company tried to spin the results the best it could. On one hand, the results were atrocious because the company spent nearly $2 for every $1 in revenue it pulled in, leading it to record negative $7.4 million in adjusted EBITDA. However, the shipper did note that its recently rebuilt fleet has the capacity to deliver significant earnings growth over the next year. That said, there's a big "if" attached to those projections given that the bulk of its hope lies in shipping rates holding firm, which, given the history of the sector, is no sure thing.

Charting the course

DryShips has been on two divergent paths over the past few years. During 2015 and 2016, the focus was on dismantling its fleet to shore up thebalance sheet. However, with its financials back on solid ground to start this year, DryShips has been aggressively rebuilding its fleet and has already agreed to buy 17 vessels for $765.5 million. These ships, according to the company's projections, have the potential to generate $77 million of annual EBITDA, which would be a remarkable turn in earnings for a company that has been bleeding cash for quite a while.

Image source: Getty Images.

The company based its projection on two factors. First, it has acquired several vessels that it has employed under time charters, which means they'll generate stable revenue as long as customers hold up their end of the bargain. For example, the company bought four Very Large Gas Carriers for $334 million that came with long-term, fixed-rate time charters. If customers exercise all of the options on those contracts, the company stands to collect about $390 million in revenue over the next eight to 10 years. In another example, the company bought a Newcastlemax dry bulk vessel that it subsequently chartered for one year at $7.1 million, or about $19,450 per day. As a result, the clearly visible revenue from these contracts provides the company with a sound foundation for its earnings projection.

Meanwhile, the second leg of the company's forecast is the projected employment rates for the rest of its ships on the spot market, which is the going market rate. That said, while the spot market can fluctuate wildly, the company used the following day rates to build its EBITDA projection:

- Newcastlemax: $16,000 per day

- Kamsarmax: $12,000 per day

- Panamax: $10,000 per day

- Aframax: $18,000 per day

- Suezmax: $25,000 per day

- Very Large Crude Carriers (VLCC): $30,000 per day

The company used these rates in its projections because that's what these ships could fetch in the current market. Because of that, it has upside if rates rise in the future. That said, it also has downside should they sink, which is where the company could run into problems.

Choppy seas ahead?

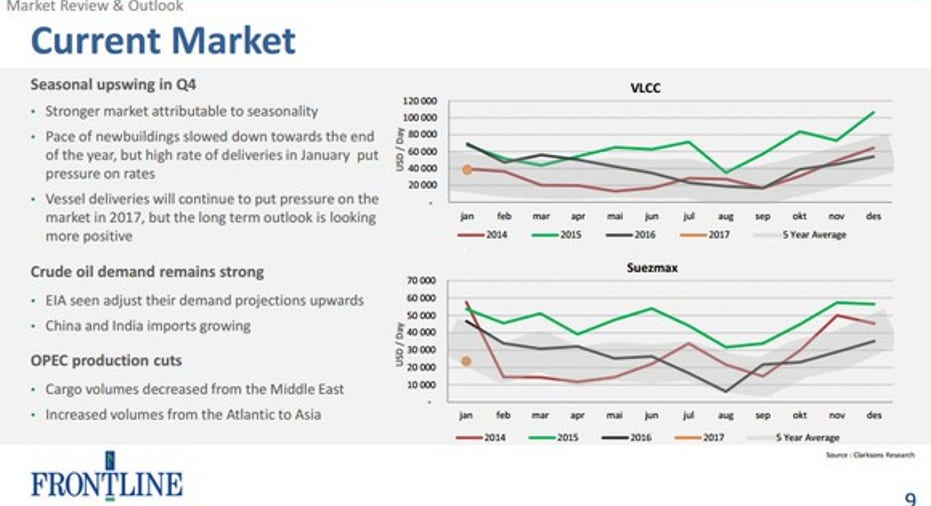

Given where spot market rates were at the time DryShips made those projections, it's easy to see why it chose those numbers. Take the rates for the Suezmax and VLCCs, which, as the following charts from leading oil tanker company Frontline (NYSE: FRO) show, are in line with the five-year average:

Image source: Frontline Investor Presentation.

That said, what this chart also clearly shows is that tanker spot rates have fluctuated wildly over the past few years. Suezmax rates, for example, were below $10,000 per day as recently as last September, while the rates for VLCCs were below $20,000 per day for much of last summer. That downside volatility has proven problematic for Frontline in the past because its cash breakeven levels for Suezmax and VLCCs are $17,300 and $22,300 per day, respectively. That means the company lost money operating these vessels when day rates plunged.

Meanwhile, day rates for dry bulk vessels have been just as volatile. For example, Star Bulk Carriers (NASDAQ: SBLK) currently has several Karmsarmax carriers signed to fixed-rate charters that range from $7,250 to $9,150 per day. Meanwhile, Star Bulk has a Panamax vessel under a time charter at just $7,750 per day. While the company signed those agreements when rates were lower than they are now, they do demonstrate how volatile the market has been over the past few years.

Investor takeaway

DryShips is putting a lot of faith in day rates holding up to drive its bullish growth projection. Because of that, the company might not grow nearly as fast as it forecasts if rates were to plunge. Although, that volatility does go both ways, because rates could just as well rise, which could make the company's projections seem conservative. This variability is something investors need to be able to handle before jumping into DryShips' stock, because its fortunes will rise and fall alongside shipping rates, which have proven to be a challenge for shippers to navigate over the past few years.

10 stocks we like better than DryShipsWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and DryShips wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.