Why Analysts Expect NVIDIA's Earnings Growth to Grind to a Halt Next Year

Image source: NVIDIA.

Graphics chip company NVIDIA (NASDAQ: NVDA) has had a tremendous run over the past year. Revenue and earnings have soared, driven by the company's gaming GPU dominance and its push into the enterprise and automotive markets. Analysts expect the company to produce $6.11 billion of revenue and $1.85 in per-share adjusted earnings this year, up 22% and 71%, respectively.

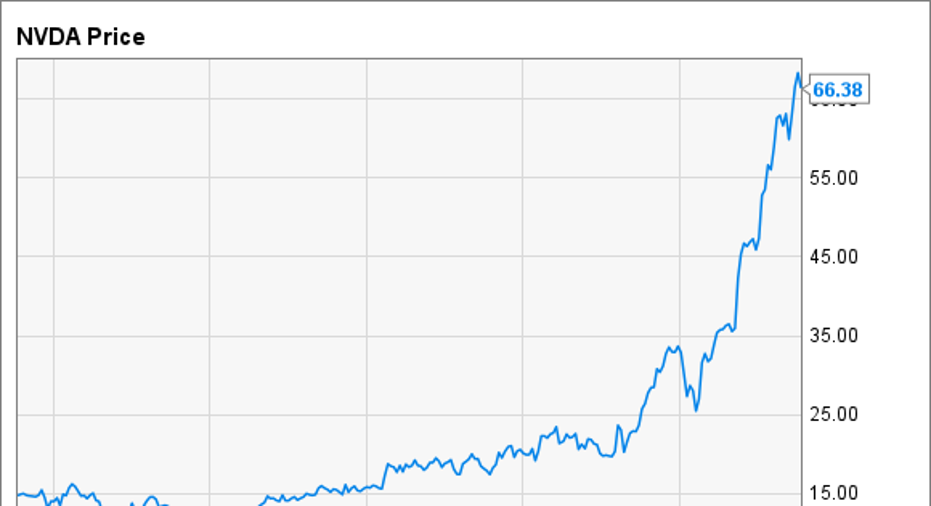

This rapid growth has led investors to pile into the stock, sending shares of NVIDIA surging. The stock is up 155% over the past year alone, and up 350% over the past five years. With a stock price of around $66, NVIDIA trades at an optimistic 36 times analyst estimates for full-year adjusted earnings.

That valuation would be reasonable if NVIDIA could maintain its current level of growth, but analysts are expecting a major slowdown in fiscal 2018, which begins in late January of 2017. Here's what the average analyst estimates look like for fiscal 2017 and 2018:

|

Fiscal 2017 |

Fiscal 2018 |

Growth |

|

|---|---|---|---|

|

Revenue |

$6.11 billion |

$6.55 billion |

7.3% |

|

Adjusted EPS |

$1.85 |

$1.91 |

3.2% |

Average analyst estimates. Data source: Yahoo! Finance.

Analysts still expect high single-digit revenue growth from NVIDIA, but earnings growth will essentially grind to a halt if these estimates are correct. Why are analysts so pessimistic? I think there's one main reason.

A major earnings headwind

In NVIDIA's latest annual report, the company included the following as a risk factor:

Since 2011, NVIDIA has been receiving payments from Intel under a cross-licensing agreement. The last payment was received earlier this year, and the first quarter of fiscal 2018 will be the final quarter in which proceeds from the agreement are recognized as revenue.

Now, $1.5 billion spread across six years may not seem like a huge deal given NVIDIA's annual revenue. But these payments are extremely high margin, mostly flowing through to the bottom line. The potential loss of this revenue could have a substantial negative impact on NVIDIA's profitability.

In fiscal 2016, which ended in January, NVIDIA reported $264 million of revenue from the Intel agreement. Adjusted operating income for the year, excluding restructuring costs, was $878 million. A full 30% of NVIDIA's adjusted operating profit came from the licensing agreement.

This percentage will be lower in fiscal 2017, given the company's earnings growth, but it still represents a significant chunk of NVIDIA's operating profit. That $264 million represents about $0.35 in EPS, using NVIDIA's tax rate from last year and its latest diluted share count.

At this point, it's unclear whether a new licensing agreement will be struck, or if it would involve the same level of payments from Intel to NVIDIA. The worst-case scenario is that this revenue disappears after the first quarter of next year, creating an earnings hole that NVIDIA will need to fill by growing profits in its other businesses. Based on analyst estimates, the consensus appears to be that this revenue is going away.

In the long run, the end of the licensing agreement is just a bump in the road. But NVIDIA being able to continue rapidly growing earnings going forward will be tough. First, the company's market share gains in the PC GPU market are beginning to be reversed as AMD goes after the mainstream portion of the market.

Second, the benefits of NVIDIA's ongoing shift toward the high end of the market will eventually be exhausted. NVIDIA has done a great job pulling customers up to higher price points, particularly with the GTX 970 in 2014. But there are only so many people willing to shell out hundreds of dollars for a high-end graphics card. NVIDIA will eventually reach the limits of its high-end strategy.

NVIDIA may be able to pull a rabbit out of its hat and renew the agreement, but at this point, the safe play is to assume that it won't. In that case, earnings growth will likely grind to a halt next year.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Timothy Green has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Nvidia. The Motley Fool recommends Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.