Why 2017 Could Be Different for Shake Shack

2016 was an up-and-down year for Shake Shack (NYSE: SHAK) stock, and in the end, shares finished up a respectable 7%. Eventually, though, investors need more for enduring the roller coaster that the stock has offered up thus far in its young life. 2017 could be the year in which that happens.

Data by YCharts.

2016 from the better burger's point of view

An investor looking at the company's stock could easily draw the wrong conclusion about the business. Revenue is actually up double digits -- 39.9% to be exact -- through the first three quarters of 2016 as compared to the nine-month period in the previous year.

Shake Shack's lineup of burgers and chicken sandwiches pleases diners. Image source: Shake Shack.

That big bump has been the result of two efforts: opening new Shacks and increasing traffic at existing ones. The company hit a milestone in the third quarter when it opened its 100thlocation, and foot traffic has been on the rise as the chain captures diner interest with new menu items like its Chicken Shack sandwich and a revolving lineup of shake flavors.

Chart by author. Data source: Shake Shack quarterly earnings reports.

Same-shack sales have started to slow as of late, but the company continues to drive the top line with a steady rollout of new locations. While profitability isn't of prime importance during this period of expansion, the bottom line increased in 2016, as well. Through the Q3 report, the most recent one, net income was at $8.5 million versus a loss of $10 million the same time the previous year.

Why more of the same is a good thing

The company plans to continue on the same course in the year ahead, and that's good news for investors. Shake Shack's strategy of slowly working its way into new markets, while broadening its reach with more openings in existing ones, has been doing the trick.

Most Shacks are clustered on the East Coast, especially in the company's hometown of New York City, but new markets are on the docket. California will be a big push in the next few years. A few have already been opened in the Los Angeles area, but the company is looking to expand further with one planned in San Diego early this year.

Image source: Shake Shack.

Overall, the company sees as many as 22 new Shacks stateside in 2017, each generating an average of $3.2 million annually in sales. Outside of the U.S., as many as 10 new Shacks are expected from the company's franchise partners.

On the subject of foot traffic and existing-restaurant sales, the company sees 2% to 3% growth ahead. A price hike is planned this month, which will contribute a percent or two, but management sees foot traffic growing, as well, with more menu rollouts and the recent launch of the Shake Shack app in a few test stores giving customers the ability to order ahead.

Following its own recipe for success, Shake Shack is set to have another successful year of business growth in 2017.

What might this mean for the stock?

Remember when Shake Shack's stock broke the $90 range in the summer of 2015? And then investors' excessive exuberance was tempered by management's plan for more measured expansion.

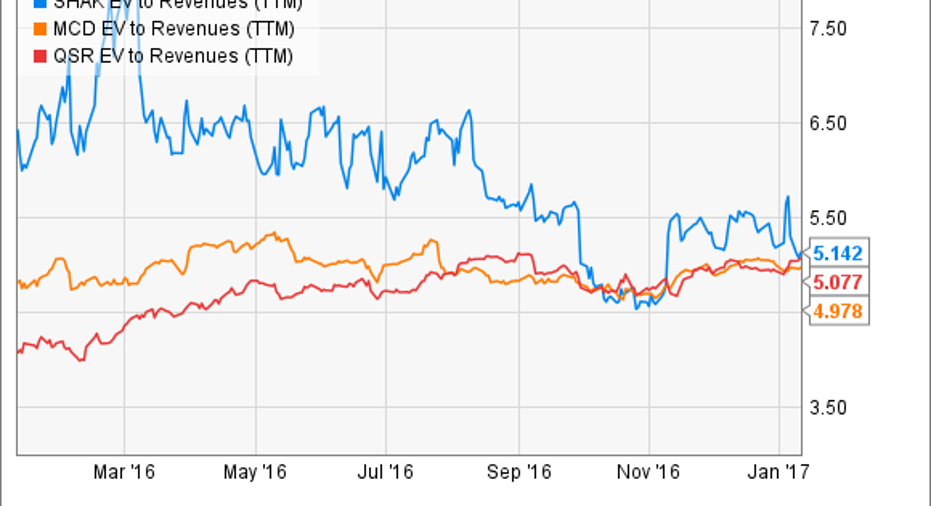

Fast-forward to today's mid-$30 stock price, and the stock hardly looks like a value when using price-to-earnings (PE) ratios. The forward P/E is at a lofty 65 as of this writing. But remember -- the bottom line is being sacrificed for growth right now. A better metric to watch might be enterprise value to revenue, a measure of a company's valuation to total sales. Here is Shake Shack compared with two larger burger joints -- McDonald's and Burger King parent Restaurant Brands International in terms of EV to revenue.

Data by YCharts..

Business growth is just beginning to catch up with share price for Shake Shack. If Shake Shack continues to win on its expansion plans, share prices should eventually gain some positive traction. With the company expecting a solid year ahead, 2017 could bring better times for shareholders.

10 stocks we like better than Shake Shack When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Shake Shack wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Nicholas Rossolillo has no position in any stocks mentioned. The Motley Fool is short Shake Shack. The Motley Fool has a disclosure policy.