What United Parcel Service Inc Q2 Earnings Mean to FedEx Corporation Investors

United Parcel Service Inc.'s (NYSE: UPS) set of second-quarter earnings gave FedEx Corporation (NYSE: FDX) investors a lot of color on industry trends and what to expect when the latter reports. The rivals give earnings in the middle of each other's reporting periods so anything they say is highly informative regarding the other's quarter. Let's take a look at the key things UPS reported that matter to FedEx as it enters its fiscal 2017.

Macro outlook

Before getting into the specifics of operating performance, let's look at clues to the macro outlook. UPS CFO Richard Peretz's commentary on the performance of each segment is particularly telling: "The international segment outperformed while U.S. domestic was on target. And finally, supply chain and freight was slightly below expectations."

The international segment did well largely as a consequence of internal productivity improvements -- a fact that augurs well for FedEx's takeover of TNT Express -- rather than from external help from the economy. Meanwhile,the weakness in supply chain and freight is largely due to a weakening economy.

In short, there wasn't anything from UPS's macro outlook to suggest that overall economic conditions were improving. However, as we shall see below, there are some positive industry-specific trends that helped UPS's U.S. domestic segment, and look likely to help FedEx, too.

E-commerce and B2C growth

As global growth expectations have been reduced throughout 2016, both companies have seen strong e-commerce and business-to-consumer (B2C) growth help offset weakness elsewhere. While the direction of the trend has been established for some time, the divergence in growth between B2C and business to business (B2B) appears to be widening. For example, UPS reported that B2C growth is "outpacing business delivery growth more than five to one."

UPS's commentary on the ongoing strength of e-commerce and B2C growth is an indication that FedEx will also be more than able to offset weakness in B2B deliveries when it gives results.

Demand for premium services

Since the last recession, UPS and FedEx have both seen customers shifting their preferences toward slower, lower-cost deliveries -- a particularly unfavorable trend for FedEx due to the historical importance of its premium express services. The following chart shows how the relative importance of the less expensive ground services has increased since 2008 for FedEx.

DATA SOURCE: FEDEX CORPORATION PRESENTATIONS.

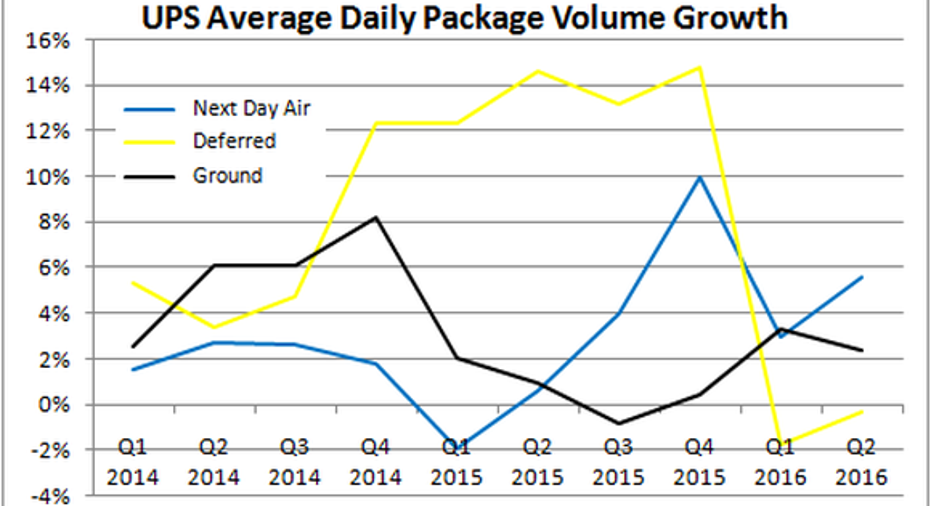

However, in recent quarters, UPS has started to report a pick-up in volume growth in its premium next-day-air deliveries. For reference, UPS's next-day-air average revenue per piece in its second-quarter was $19.51 compared to $8.11 for its ground packages. As you can see below, next-day-air has been doing well recently.

DATA SOURCE: UNITED PARCEL SERVICE PRESENTATIONS.

UPS CFO Peretz addressed the issue on the earnings call: "The next-day-air gains were produced by customers of all sizes. Demand was consumer based as more online retailers are providing faster delivery options to stay competitive."

Is that a sign that customers are starting to be more willing to pay for quicker, more expensive deliveries? If so, it would be good news for FedEx Corporation.

FedEx ground margin

While strong e-commerce and B2C growth obviously creates a revenue growth opportunity in ground, it also creates some challenges. For example, UPS CCO Alan Gershernhorn talked of "changes in the customers and product mix and specifically the package characteristics as we bring more light weight into the business." Throw in the negative impact of lower fuel surcharges, and UPS struggled to eke out a slight increase in U.S. domestic package margin.

Turning back to FedEx, on the fourth-quarter earnings call, CFO Alan Graf outlined expectations for ground revenue and operating income to increase in FedEx's fiscal 2017. That's the good news, but he also signaled that ground margin would "be negatively impacted by higher operating costs in FY17, driven again by network expansion. Other operational costs may also impact margins as residential volumes grow from e-commerce."

In other words, it's far from clear if FedEx ground margin will increase in the first quarter -- something to look out for.

Expanding services

As readers already know, UPS management recently outlined plans to offer new technology features for My Choice and expand its Access Point locations. Such actions are a response to the strength of e-commerce-led B2C demand.

On its last earnings call, FedEx management spoke of leveraging certain services to help "heavy demand during peak," and don't be surprised if FedEx follows UPS in expanding services conducive to B2C demand. For example FedEx Delivery Manager helps customers schedule deliveries in a similar way to UPS's My Choice, and Hold at FedEx Location offers similar benefits to UPS Access Point.

The bottom line

All told, based on UPS's earnings presentations, it looks likely that there are enough positive trends for FedEx to be able to offset weakness in the economy and B2B market. It will be interesting to see if FedEx's premium services expand, and whether ground margin will improve. Meanwhile, it's possible management will seek to expand its B2C service offerings.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of and recommends FedEx. The Motley Fool recommends United Parcel Service. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.