What Is Williams Companies Inc.'s Greatest Risk?

Image source: Getty Images.

Williams Companies (NYSE: WMB) has announced several strategic initiatives designed to mitigate some of the risks that have impacted the company in recent years. However, there is one significant risk that remains: the gap between the capital resources and projected growth spending at its master limited partnership,Williams Partners (NYSE: WPZ). The company needs to close this gap without diluting its growth by overpaying for the money it needs so that it gets the most value from that growth going forward.

Minding the gap

Williams Companies has made three important strategic decisions since its merger with Energy Transfer Equity (NYSE: ETE) fell through a couple of months ago. First, it cut its dividend and plans to reinvest that cash to support Williams Partners. Second, both companies sold their Canadian operations, which brought in roughly $1 billion in cash to fund capex. Finally, both companies are exploring strategic options for their stake in the Geismar plant, which could bring in additional capital or stabilize that plant's cash flow.

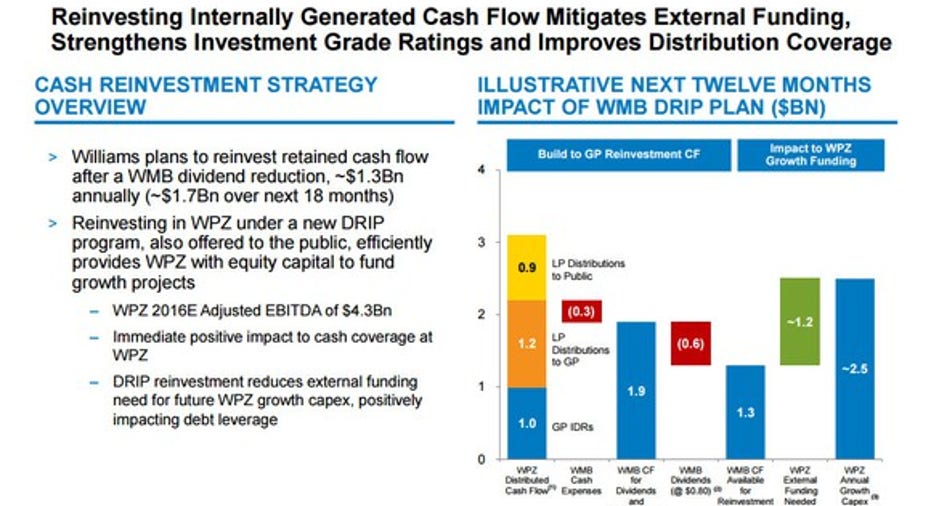

Despite all this progress, Williams Partners still has a pretty wide gap between its capital resources and growth capex over the next two years:

Data source: Williams Companies investor presentation.

As that slide notes, Williams Partners has roughly $2.5 billion in annual capex requirements. After factoring in Williams' support, it still needs to find another $1.2 billion in capital annually to cover that spending, though the recent Canadian asset sale reduced that gap quite a bit. That said, the company still projects to have a pretty wide shortfall between capital and capex in 2017. The risk is that the company will not be able to source that capital on attractive terms.

What might Williams do?

Williams Partners intends to use several options to fund this gap over the next year. One of the primary vehicles is its recently established distribution reinvestment program (DRIP), which would allow common unitholders to join Williams Companies in taking additional units instead of cash. If a significant portion of unitholders take this option, it will enable Williams Partners to retain more of its internally generated cash flow to fund growth. Another option is to use its at-the-money (ATM) program to issue equity to outside investors strategically. Finally, the company would like to tap the debt markets to issue additional bonds as long as it can maintain its investment-grade credit rating.

The concern with these options is the price the company has to pay for this funding. For example, given its current unit price Williams Partners is paying a high price to issue equity, even if that equity is to existing investors. Furthermore, its weaker credit rating compared to rivals forces it to pay a higher interest rate on new debt. For example, earlier this year, the company's Transco subsidiary needed to pay a 7.875% interest rate to issue $1 billion of 10-year senior notes to fund growth projects and repay maturing debt. Contrast this with Energy Transfer Equity's MLP Energy Transfer Partners (NYSE: ETP), which was able to issue $1 billion 10-year debt in mid-2015 at just 4.75%. Theincreased cost of capital at Williams is a concern because more of the cash flow from its growth projects will go toward interest payments instead of shareholder distributions.

Because of this, Williams Partners might need to get creative to fund some of its growth projects. That is something Energy Transfer Partners did earlier this year by obtaining project-level financing from a syndicate of banks for one of its primary pipeline projects to provide it with all the remaining capital it needed to complete the project. Also, Energy Transfer Partners sold a stake in that project to additional joint venture partners, which will allow it to redeploy that capital toward debt reduction as well as funding its other growth projects. Creative options such as these could help Williams Partners lower its cost of capital as it closes its funding gap.

Investor takeaway

Williams Companies' greatest risk right now is that its MLP pays too high a cost to obtain capital for growth projects. Doing so would not only dilute its stake in the entity but result in too much of the incremental cash flow from these projects going to credit investors or outside unitholders instead of Williams. To mitigate this risk, Williams Companies needs to get creative to find funding for its MLP so that it can keep more of the value created by its future growth.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.