Weyerhaeuser: Merger Synergies to Tide Investors Over Until Market Recovery

On Nov. 8, Weyerhaeuser announced that it would acquire Plum Creek Timber for the cost of 1.6 Weyerhaeuser shares per Plum Creek share. Even before this announcement, Weyerhaeuser was the largest timberland REIT, and Plum Creek the second-largest. Together they create a behemoth, with 12.9 million acres of trees across the U.S., 323,000 in Uruguay, and long-term licenses for 13.9 million acres in Canada(where timberland is almost exclusively owned by the provinces).

Timber investment benefits from geographic diversity: Storms, disease, mill shutdowns, and even demand are local phenomena. The combined company will have a presence in most of America's lumbering areas, but with strong exposure to the South (7.3 million acres) and Pacific Northwest (3.0 million), which are the most attractive regions from both a sylvicultural perspective (species, growth rates) and a commercial one (strong local markets, access to export termini). Fortunately for both companies, 92.7% of the Canadian acreage is in regions unaffected by the mountain pine beetle, which has done considerable damage to British Columbian forests.

On the day of the announcement, Weyerhaeuser also reported that it is "exploring strategic alternatives" (i.e., seeking a buyer) for its fiber division, a $1.9 billion business that earned $291 million pre-tax in 2014. It's a healthy business that would fit more naturally with a paper manufacturer. If both transactions are completed, the new company will be a purer forestry play than Weyerhaeuser was. Based on the companies' combined 2014 revenue, selling the fiber business would reduce their exposure to forest product-consuming businesses by 21.8%. Weyerhaeuser does more lumber milling than Plum Creek. This segment consumes forest products, too, but it adds limited value to them. Often, ownership just ensures that there is a mill within economical distance of production, and most of the timber processed comes from their own properties. In 2014, milled products accounted for 48.9% of the companies' revenue.

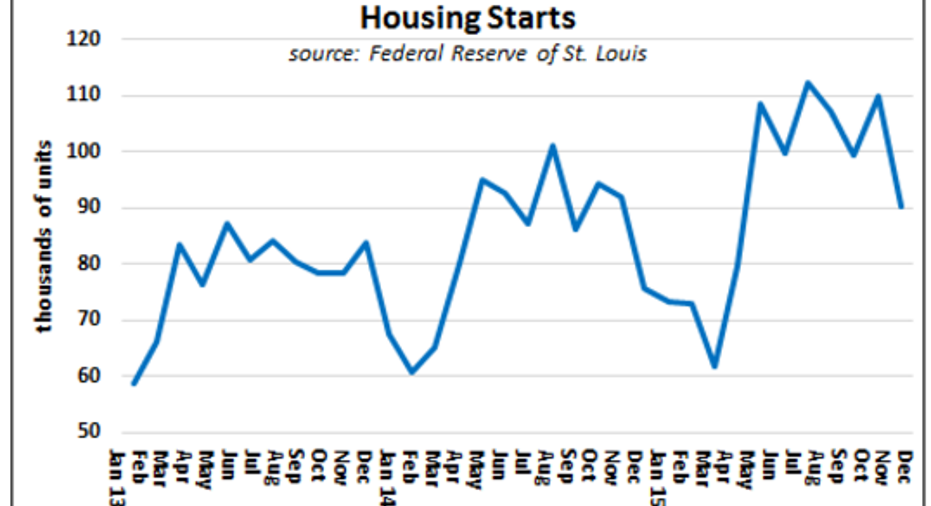

"Purity" is valuable because unfelled timber is an attractive asset. It's a renewable resource that can be "stored on the stump," continuing to gain tonnage and value per ton. The prices of forest products are determined by housing starts, as well as demand from paper makers and for biofuel pellets. Assuming both planned transactions are completed, about half of the new company's revenues will come from stumpage -- the sale of standing timber -- and half from lumber, plywood, chipboard, and fiberboard (some mills sell to each other; fiberboard is made from sawdust). In 2014, 59.3% of the stumpage Weyerhaeuser earned was from sales to its own mills. Plum Creek's percentage was lower.

Weyerhaeuser expects to reduce operating costs by $100 million, or 1.5%, within a year of closing. These savings will mostly come from headquarters consolidation, but there are doubtless other areas where costs can be trimmed. Some acreage will probably be sold. Forestry is pretty much the lowest-value use for land, and Weyerhaeuser aggressively seeks "Higher and Better Use" land. Trees often stand on mineral resources, electrical transmission or pipeline rights-of-way, wind turbine sites, or locations suited to recreation or vacation homes. In particular, Weyerhaeuser may regard some of Plum Creek's 792,000 acres in Georgia as candidates for sale.

Logs to be milled into building materials provide most timberland revenue. Pulp and pellets are, in most cases, secondary revenue sources. Lumber consumption depends on housing activity. Recovery from the recession has been desultory, but it would have sufficed to support lumber prices if dollar strength had not reduced export competitiveness and attracted imports from Canada and South America. Considering the amount of lumber being thrown onto the U.S. market, price declines have been less severe than might be expected. This suggests that U.S. timberland owners are harvesting conservatively.

Data source: Federal Reserve of St. Louis.

Data source: RandomLengths.com.

A significant price recovery is unlikely to occur soon. However, in 2016, holders of the combined companies have cost savings to look forward to, and possibly the proceeds from sale of the fiber unit. Weyerhaeuser has also committed to maintaining its dividend, which currently provides a 4.07% yield. It will also repurchase $2.5 billion in shares after the Plum Creek acquisition closes. Longer term, Weyerhaeuser will likely be a powerhouse, and investors are being paid pretty well to wait until conditions allow it to flex its muscles.

The article Weyerhaeuser: Merger Synergies to Tide Investors Over Until Market Recovery originally appeared on Fool.com.

John Abbink has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.