Wall Street is Undervaluing Enterprise Products Partners, Here's Why They're Wrong

Source: Kinder Morgan.

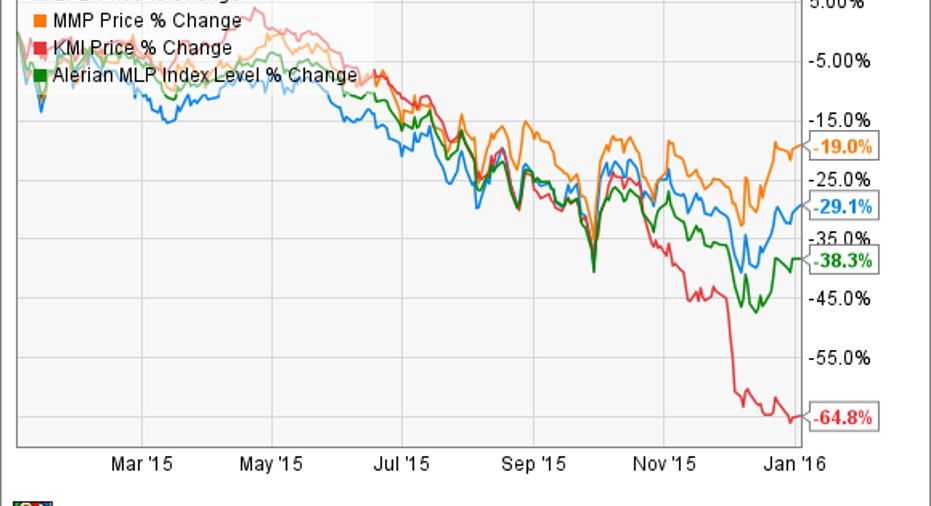

The oil crash has devastated all energy stocks this year and caused evenmidstream juggernaut Kinder Morgan (NYSE: KMI) to slash its dividend by 75%. Given that Kinder Morganwas able to continue growing its dividend even during the financialcrisis, many investors apparently believe that the security ofall midstream MLPs' distributionsare now in doubt, even those of such blue-chip names as Enterprise Products Partners (NYSE: EPD), andMagellan Midstream Partners (NYSE: MMP).

Yet the fact is that Enterprise Products Partners, despite a yield nearly double that of Kinder Morgan, still represents one of America's best, andsafest,long-term income growth opportunities over the next decade or two.

Let's explore three reasons Wall Street is dead wrong about Enterprise and how your diversified income portfolio could benefit from its mistake.

It's too darned cheap!

| Company | Yield | 5 Year Average Yield | Price/Operating Cash Flow | 5 Year Average Price/Operating Cash Flow |

| Enterprise Products Partners | 5.9% | 4.7% | 13.3 | 14.9 |

| Magellan Midstream Partners | 4.5% | 3.9% | 15.6 | 16.1 |

| Kinder Morgan | 3.3% | 4.6% | 7.2 | 10.3 |

Sources: Ycharts, Yahoo Finance, Fastgraphs

For an MLP of Enterprise Product Partners' caliber, the current yield represents a gross mispricing by Wall Street. Enterprise represents immense quality, cash flow-generating energy transportation and storage assetson sale. From the perspective of long-term dividend investors looking for a safe, growing yield, andstronggrowth potential over the next five to 20 years, it represents a fantastic opportunity.

One of America's best payout profilesDespite whatjust happened to Kinder Morgan's dividend, the assets owned by these midstream MLPs remain some of America's best long-term cash flow generators. Kinder's painful decision was not due to an inability to maintain its dividend, but rathera wise long-term decision to use its distributable cash flow (DCF) to fund future growth and retain its investor grade credit rating which keeps its debt costs lower.This could result in much higher dividends in a few years, once energy prices inevitably recover.

| Company | YTD Payout Coverage Ratio | YTD Excess DCF | 5 Year Analyst Payout Growth Projections |

| Enterprise Products Partners | 2.0 | $2.72 billion | 5.5% |

| Magellan Midstream Partners | 1.4 | $196 million | 10.2% |

| Kinder Morgan | 4.2 | $2.64 billion | 2.7% |

Sources: company 10-Qs, 10K's, author calculations

Note that Kinder Morgan's distribution coverage ratio and excess DCF takes into account the new reduced divided. All three pipeline operators' payouts are currently highly sustainable, and they are generating strong excess cash with which to invest into future growth while greatly reducing how much capital they need to raise from debt or equity markets.

Kinder's high debt levels and lack of access to equity growth capital is another reason it had to reduce its dividend. However, neither Enterprise nor Magellan Midstream is likely to share a similar fate because of much stronger balance sheets and an ongoing ability to sell additional units at prices that allow for accretive investment (meaning that DCF per unit increases despite a higher unit count).

This ability to generate and invest excess DCF is what makes Enterprise's current high yield such an appealing investment opportunity. The MLP's track record of growing its payout -- 45 consecutive quarterly distribution increases -- no matter what energy prices are doing is courtesy of its business model in which almost all DCF is derived from long-term fixed-fee contracts with guaranteed volumes.This tollbooth business model and rivers of excess DCF makes Enterprise a true "widows and orphans" dividend stock for the next few decades.

Source: Enterprise Products Partners investor presentation.

Why Enterprise isn't likely to share Kinder's fateKinder Morgan's dividend cut serves as a cautionary tale for midstream MLP investors. No matter how wonderful and cash flow rich acompany's assets, excessive debt can make any payout incompatible with continued growth.

Year to dateEnterprise Products Partners hasinvested $3.7 billion on growth projects and acquisitions, has $1.8 billion in additional projects coming online in Q4 ,and planstoinvest$7.8 billion into growth projects through the end of 2017. With the MLP spending so heavily what is the risk of Enterprise becoming over levered and running into the same problems as Kinder?

| Company/MLP | Debt/EBITDA (Leverage) Ratio | Current (Liquidity) Ratio |

| Enterprise Products Partners | 4.5 | 0.7 |

| Magellan Midstream Partners | 2.9 | 0.8 |

| Kinder Morgan | 7.6 | 0.5 |

Source: Morningstar

As you can see both Enterprise and Magellan have much stronger balance sheets than Kinder, with far more manageable relative debt levels. This is thanks to their more conservative managements, who have been careful to grow distributions slower than DCF per share in order to create large coverage ratios that ensure plenty of excess cash flow.Thisallows more capital expendituresto be funded internally and not become dependent on debt markets for growth funding.

Bottom line Enterprise Products Partners and Magellan Midstream Partners are much better positioned to continue funding growth projects with far less reliance on debt and equity markets. With some of the strongest coverage ratios in the industry representing massive ability to generate excess DCF, their generous payouts represent some of America's most sustainable high-yield distributions.

In my opinion, because of both its current and futureportfolio of massively diversified cash flow-generating assets,Enterprise Products Partnersin particular is trading at absurdlyundervaluedprices.As one of America's highest-quality dividend growth opportunities, itdeservesat least a place on every dividend investor's radar, if not in their portfolios.

The article Wall Street is Undervaluing Enterprise Products Partners, Here's Why They're Wrong originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan. The Motley Fool recommends Enterprise Products Partners and Magellan Midstream Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.