Understanding Sierra Bancorp in 3 Charts

Bank stocks have been doing quite well since the Donald Trump got elected. The prospect of reduced regulation and increased interest rates has fired the imagination of investors around the globe. Here is the S&P Bank Index (KBE) compared to the better known S&P 500 Index over the past month:

Source: Google Finance

Just buying the bank index will give you exposure to this trend, but individual stocks can give you an even greater return. I know of a well-run small-cap bank that beat even these excellent returns.

A strong balance sheet indicates good management

A greatly improved balance sheet can indicate an undervalued investment: a diamond-in-the-rough. Because of poor performance a few years ago, many investors have written off Sierra Bancorp (NASDAQ: Sierra Bancorp). But recent changes in the type of loans they pursue has greatly increased Sierra Bancorp's loan quality. Once investors focused on banks again, Sierra Bancorp's return beat both the S&P Bank Index and the S&P Regional Bank Index (KRE):

Source: Google Finance

A good way to measure asset quality in banks is non-performing loans. These are loans that are no longer paying interest or principal, and are almost in default. A bank with a large percentage (greater than 1%) of non-performing loans can either sell them at a loss, or modify the loan terms to allow a debtor to extend the maturity of the loan. One costs money and the other costs time. Both reduce the profitability of the bank.

NPLs are down to $6.3 million (0.5% as a percentage of total loans and leases) in Q3 2016. A non-performing loan percentage of 0.5% is very good. Management attributes the improvement to "loan growth... in portfolio segments with low historical loss rates" and "tighter loan underwriting standards implemented subsequent to the recession."

Author created chart. Data source: company 10-Ks and 10-Qs

Sierra Bancorp's improvement from above 7% in 2011 to just 0.5% in 2016 is remarkable. Bank of the Sierra's NPL ratio is well in-line with that of competitors like Bank of Marin and Westamerica Bancorp. Clearly they are in a much better position than they were 2 years ago, a fact that went unrecognized in the first week after the election.

The next question is, was this improvement just luck or due to skilled management?

How Bank of the Sierra improved their business model

Transformation at a bank takes time -- but over the long term, you can see how they've shifted. Here's their loan mix from the worst period for non-performing loans (Q3 2009):

Author created chart. Data source: company 10-Ks and 10-Qs

"Other Construction/Land" and "Small Business Administration Loans" had some of the highest non-performing loan rates, regularly above 10%. Commercial real estate and farmland were doing well -- often around 0.2% even during the height of the Recession. Sierra Bancorp's management changed their loan mix to deal with this. More money was allocated to loan types that were performing well:

Author created chart. Data source: company 10-Ks and 10-Qs

"Other Construction/Land" dropped substantially and "Small Business Administration Loans" disappeared entirely. Commercial real estate and farmland increased.

Also notice the addition of "mortgage warehouse lines". These are short-term lines of credit extended to mortgage bankers while they are selling their mortgages to the final investor. Essentially a borrower gets approved for a loan, then the mortgage originator looks to sell the loan to a larger investor. When the borrower's loan is sold, the mortgage banker pays back the line of credit. This process takes around a month from start to finish.

The short duration of the "mortgage warehouse line" lowers the risk of Sierra Bancorp's loan portfolio. No non-performing loans are reported in this part of the portfolio because they are paid off so quickly. Additionally, they are usually only approved if a mortgage is close to completion. This adds an extra layer of due diligence which lowers risk further.

Admitting your mistakes is a sign of good leadership. Bank of the Sierra's plan to move away from poorly performing sectors is evidence that they could have what it takes to keep up with changing times.

Undervalued

With a balance sheet full of safer assets, Bank of the Sierra should be trading at higher prices than before. But prior to the election that wasn't the case.

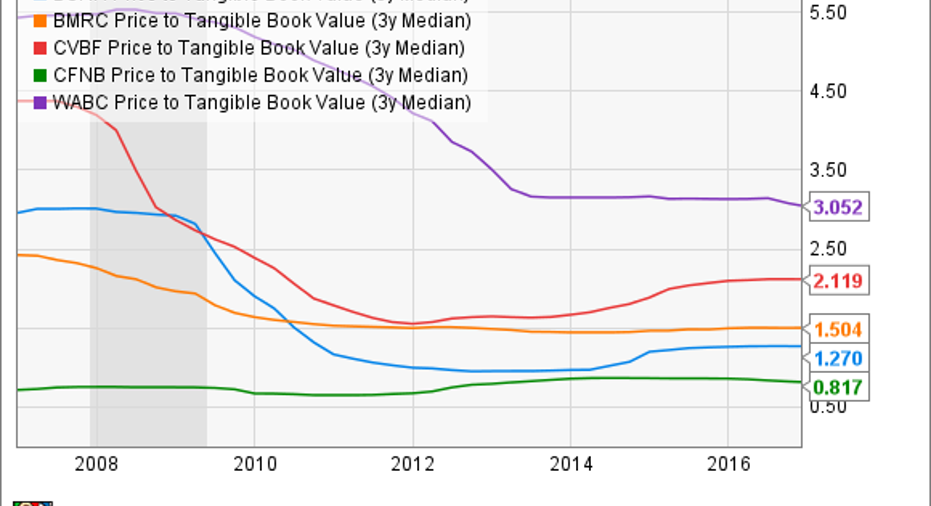

Price-to-tangible book (P/TBV) value is a easy way to value bank stocks in the same risk category. It examines the ratio of market capitalization divided by tangible assets minus liabilities. This eliminates any effects of intangible assets like goodwill that may not produce income. A price-to-tangible book value ratio below 1 means that you can buy the company's tangible book value at a discount.If there is nothing majorly wrong with the company, it's a great deal.

After the Great Recession of 2008-09, many banks were trading at depressed P/TBV ratios:

Some investors believe that the Dodd-Frank Act, enacted in 2010, has made banks less appealing. This act tries to make banks safer at the expense of short-term profits by limiting the amount of risk banks can take. This is a drag on their profits since they have to hold more reserves.

A Trump presidency is more likely to scale back these banking reforms. If restrictions on banks are loosened, these riskier banks will probably earn more money. So many investors think they are now worth higher P/TBV ratios.

In the weeks after the Republican win, many California regional banks surged upward in valuation:

Sierra Bancorp increased more than most, but still remains undervalued compared to similar banks. Because of its low-risk assets, management can increase leverage in the future without making the bank too risky. In this sense, Sierra Bancorp could increase further in the future as interest rates rise.

Going forward

If Dodd-Frank is repealed, it will be important to own banks that have been responsible in reducing their risky assets. Just like dogs, if they are all let off their leashes you want your bank to be well trained, not running wild all over the neighborhood.

The high quality loans at Bank of the Sierra and potential for increased leverage can support the recently increased prices. If earnings continues to improve as a result of future economic growth, or good acquisitions, I like Sierra Bancorp's chances.

10 stocks we like better than Sierra Bancorp When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Sierra Bancorp wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of November 7, 2016

Christopher Flens-Batina owns shares of BMRC. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.