This Social Security Spousal Benefits Loophole Closes Forever on April 30th

For ages, there's been a not-so-secret loophole for Social Security spousal benefits. It's called "File and Suspend," and it will soon be coming to an end. As you'll see, the loophole has the potential to be quite lucrative, and if you're thinking about using the strategy, your window for doing so is rapidly closing.

The basics of your Social Security benefitThe size of a retired worker's Social Security check is based on two factors:

- The highest 35 years of annual earnings -- adjusted for inflation.

- When the worker files for Social Security benefits.

Currently, a retired worker can receive his/her "full" benefit if they start collecting monthly paychecks at the age of 66. But, if that retired worker chooses to, he/she can delay benefits up until age 70 -- and the size of those monthly benefits will increase by 8% for every year after the age of 66 they wait. Plus, there are upwards changes from inflation that factor in as well.

If Rosie the Riveter is slated to take home $1,500 per month at age 66, she could instead deposit almost $2,000 per month if she waits to claim until age 70. That's a powerful incentive!

But what about Social Security spousal benefits?Rosie's husband, Rob -- who stayed home with the kids -- can also qualify for benefits. In fact, as long as Rosie waits until her full retirement age to claim benefits, Rob can take home as much as half of Rosie's benefit. In other words, he can take home $750.

But here's the rub: Rob's spousal benefits do not increase for each year Rosie chooses to wait beyond age 66. And this is where the "File and Suspend" loophole originated. Here's how it works:

- Rosie files for Social Security at age 66

- Rob immediately files for spousal benefits.

- Once Rob's paperwork clears, Rosie turns around and suspends her benefits until age 70.

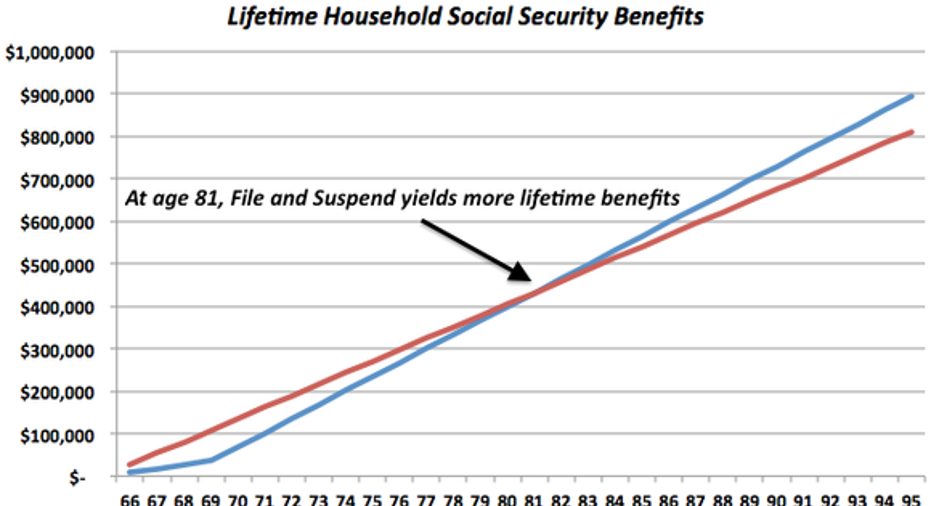

Rosie and Rob get to have their cake and eat it too: both will be able to maximize their Social Security benefits. To get an idea for how this plays out, look at the chart below. The blue line represents Rosie and Rob using File-and-Suspend, while the red line shows what happens if they both start collecting at age 66.

Source: Author's calculations

If Rosie and Rob live to the age of 81, then they have received a better lifetime deal from Social Security. In fact, if they live to the age of 100, they will have received over $100,000 more from the program -- in today's dollars.

The end of file and suspendThough these numbers are simply used to demonstrate the loophole, this helps explain why, in the debate over this year's Congressional Budget, both Republicans and Democrats agreed that the loophole needed to be closed. But when that decision was made, a 180-day grace period was enacted. During this time frame, would-be retirees can still use the strategy. But that grace period comes to an end on April 30 -- and will likely never open again.

That leaves three options. The first is to file for retiree and spousal benefits at age 66 -- or the red line above. The second is to wait until age 70 to start collecting. And the third is to start collecting at the same time somewhere in between.

Every household's life situation, values, health, and culture play a role in deciding which route to take -- or if its even worth exploiting the loophole while its open. I can't offer a one-size-fits-all solution, but its worth noting that this loophole is still available, albeit for a very short time.

The article This Social Security Spousal Benefits Loophole Closes Forever on April 30th originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.