This Chart Sums Up Wells Fargos Fall From Grace

Data source: Wells Fargo and JPMorgan Chase. Chart by author.

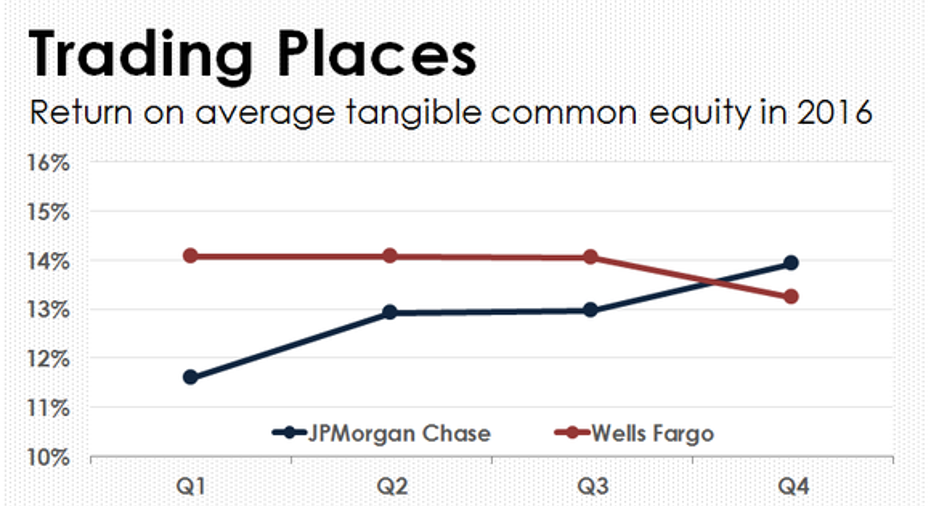

You can rest assured that Wells Fargo (NYSE: WFC) was more than ready to close the file on 2016 after a number of missteps tarnished its reputation and contributed to a lagging stock performance. But perhaps nothing illustrates Wells Fargo's recent fall from grace more than the fact that, as of the fourth quarter, it's no longer the most profitable big bank in the United States.

Wells Fargo was one of the few big banks to emerge from the financial crisis with its reputation intact. By steering clear of the worst corners of the subprime mortgage market in the lead-up to the downturn, it suffered significantly less damage than most of its peers.

This positioned the California-based bank to capitalize on the mistakes of others. Most notably, in 2008, it acquired its larger East Coast rival Wachovia for a significant discount to book value. This more than doubled the size of Wells Fargo's balance sheet and ultimately contributed to its ascent over Citigroup as the third-biggest bank in the country, with nearly $2 trillion worth of assets.

It was no coincidence that Wells Fargo was also the most profitable multitrillion-dollar bank in America throughout the past eight years. Fueled by comparatively low loan losses and an especially lean operation, it consistently returned 12% or more on its equity while its peers struggled to break the all-important 10% threshold.

The Wells Fargo Center in downtown Denver, Colorado towers over neighboring skyscrapers. Image source: iStock/Thinkstock.

But all of this changed last September when the Consumer Financial Protection Bureau revealed that Wells Fargo had been caught opening millions of fake accounts for customers in order to boost its cross-sell ratio. Although it was only fined $185 million for the transgression, which amounted to less than 4% of its quarterly earnings, the bank's problems with regulators soon snowballed.

Later in September, the Office of the Comptroller of the Currency (OCC), the principal regulatory body for nationally chartered banks, fined it $20 million for, among other things, improperly evicting U.S. servicemembers from their homes and repossessing their vehicles. And two months later, in November, the OCC doubled down by imposing a series of new restrictions on the bank that required it to seek regulatory approval for a wide range of business decisions.

Wells Fargo's downbeat year was capped off by the Federal Reserve's announcement in December that the bank was the only major U.S.-based lender to fail to remedy its previously criticized living will, a key regulatory test created by the 2010 Dodd-Frank Act. This led to further sanctions, including restrictions on the ability to make acquisitions, or expand internationally.

A rare decline in Wells Fargo's profitability followed. It started the year generating a 14.1% return on average tangible common equity in the first quarter. But by the fourth quarter, this had fallen to 13.2%. Not only was this disappointing in its own right, but it also provided an opening for JPMorgan Chase to steal the top spot. Indeed, as you can see from the chart at the top, Wells Fargo is now no longer the most profitable multitrillion-dollar bank in America.

10 stocks we like better than Wells Fargo When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Wells Fargo wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

John Maxfield owns shares of Wells Fargo. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.