These 2 Hated Dividend Stocks Are Buys

With so much euphoria going around Wall Street today, it's hard to find a stock that the market doesn't like as of late. What's even harder is finding great companies actually worth your investment dollars that aren't well received today. There are a couple out there, though, and two examples of these unloved stocks are oil services company Core Laboratories (NYSE: CLB) and broad line equipment supplier W.W. Grainger (NYSE: GWW).

Here's a look at why the market haven't been too keen on Core or Grainger's stocks lately, and why these companies are worthwhile investments despite Wall Street's pessimism.

Image source: Getty Images.

Bouncing back into form

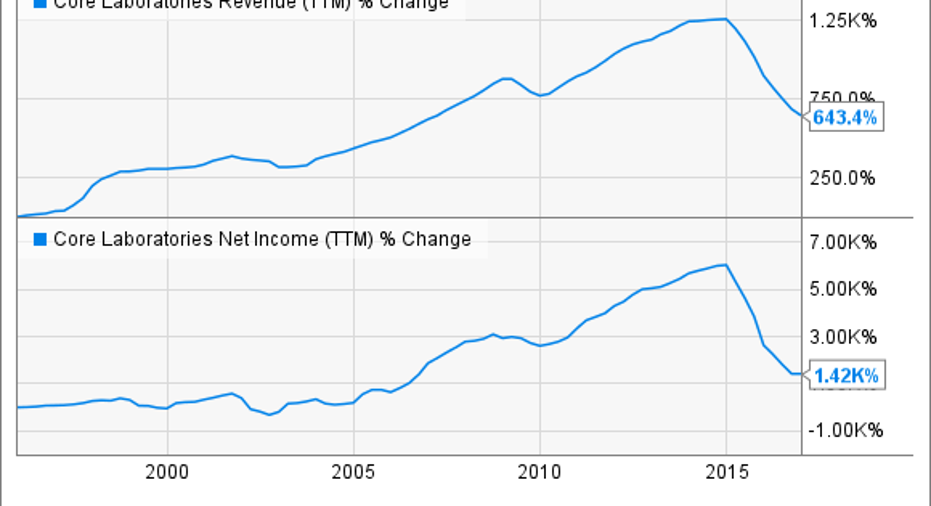

As an oil services company, Core Laboratories' prospects are going to wax and wane with how much producers want to spend on new production. Up until lately, that amount hasn't been much, and as a result, Core's revenue and bottom line have suffered quite a bit during this downturn. Consequently, bears have been piling onto this stock, with 13% of the company's stock sold short.

CLB Revenue (TTM) data by YCharts.

There isn't any real way to spin those numbers above as positive, but the one thing to keep in mind is the company's competitive strengths as the oil and gas industry pick back up again. One is that its primary service -- lab testing of reservoir core samples -- is an offering that improves well economics for producers. This is something that gives Core stronger pricing power than some of the more commoditized oilfield service offerings. Another major benefit for Core is that it is an extremely asset-light company. This means that its capital spending requirements are quite modest, and more revenue can be converted to free cash flow. In fact, even during this downturn, Core still generated $0.20 of free cash flow for every dollar of revenue.

Core Labs is an extremely difficult stock to value with most traditional metrics. It has bought back more stock than it has retained earnings over the year, and so its equity value is actually negative. Probably the best way -- although not a great way -- to value the stock is by its dividend yield, which stands at 1.9% today. That is well above its historical average and suggests that as the rebound in oil and gas drilling activity takes place, we will see a strong increase in earnings and stock price for Core.

What's not to like?

Like Core, W.W. Grainger has a pretty high short interest -- about 12.1% of total shares outstanding. Yet if you look at how the company has performed over the years, it is really hard to see the short thesis on this stock. Perhaps the biggest criticism lately is that its return on invested capital declined over the past 12 months to 13.8%, its lowest in over a decade. There is also the idea that the company's sales model has relied on customer service reps working with large business clients to supply maintenance, repair, and operations equipment, and that web-based procurement platforms could take market share and hamper margins.

If that is the most bearish thesis that can be built for this company, then it would seem that such high short interest isn't really justified. The company is tackling these two things head on. Grainger has shifted away from its older service model to one that has a greater focus on online purchase orders and delivery of products versus in store orders and pick ups. To accomplish this, it has increased spending to develop its online sales platforms and its logistics and distribution network. That higher rate of invested capital in recent years is why were seeing a decline in returns on invested capital. Simply put, there have been some large additions to capital that have yet to produce returns.

It's also worth noting that these new online sales models have provided an opportunity to go after smaller businesses, and it has turned into a boom for Grainger. Its single-channel business segment -- aka online ordering -- was just 10% of overall revenue, but saw a 35% jump in revenue growth in 2016, with a high return on invested capital. With much of Grainger's additional capital spending done, don't be surprised if those returns on invested capital jump back up again.

GWW Dividend data by YCharts.

At an enterprise value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization)ratio of 12.5, you can't really call W.W. Grainger a cheap stock, but the company has a long history of generating high rates of return and rewarding shareholders with an increasing dividend and buying back shares. With a major growth platform taking off added to a business that has a propensity to reward shareholders, it's hard to see why Wall Street hates this stock.

10 stocks we like better than Core LaboratoriesWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Core Laboratories wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe owns shares of Core Laboratories. The Motley Fool owns shares of and recommends Core Laboratories. The Motley Fool has a disclosure policy.