The Waiting Game: When Will Energy Transfer Equity LP Finally Give Investors a Raise?

Image source: Getty Images.

Before the downturn in the oil market,Energy Transfer Equity (NYSE: ETE) had increased its distribution to investors for 12 straight quarters. It was also projecting to deliver pretty healthy distribution growth in the future. Unfortunately, that growth never materialized, with the company opting to keep its payout flat for the past four quarters due to worsening market conditions and concerns surrounding the company's ill-fated attempt to acquire rival Williams Companies (NYSE: WMB). That leaves investors and analysts wondering when the company will finally restart distribution growth.

An incorrect forecast

At its analyst day late last year, Energy Transfer Equity projected that it would be able to deliver peer-leading distribution growth of 21% compounded annually over the next couple of years:

Data source: Energy Transfer Equity investor presentation.

One of the drivers of that growth was the anticipated addition of Williams Companies, which at the time expected to be in the position to grow its payout by 12% annually. Needless to say, with Williams out of the picture it removed one of Energy Transfer Equity's growth drivers. Instead, it was left to rely on its three master limited partnership affiliates Energy Transfer Partners (NYSE: ETP), Sunoco Logistics Partners (NYSE: SXL), and Sunoco LP (NYSE: SUN) to drive growth going forward.

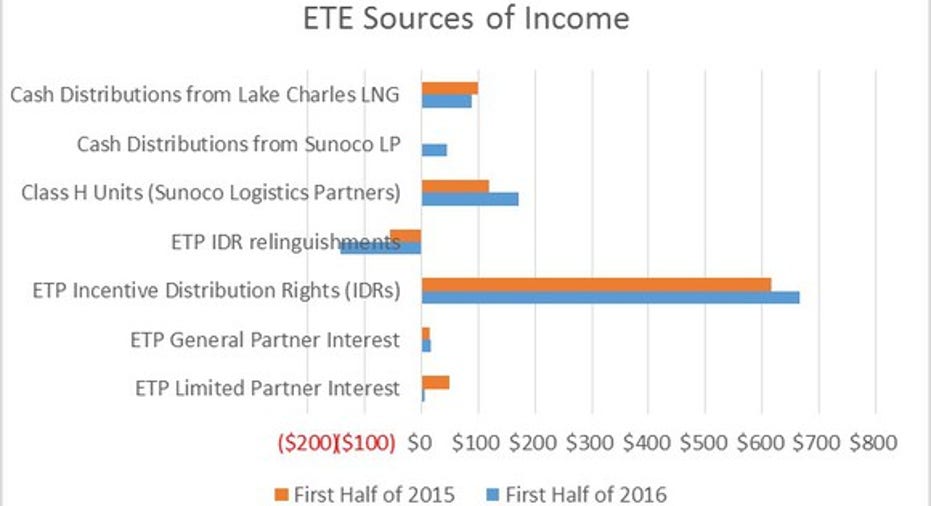

Of that trio, Energy Transfer Partners provides the bulk of Energy Transfer Equity's income:

Data source: Energy Transfer Equity investor presentation. Chart by author. Note: In millions of dollars.

As that chart shows, the incentive distribution rights (IDRs) from Energy Transfer Partners is the primary source of income. That is worth noting because Energy Transfer Equity is not collecting the full amount owed due to relinquishing a portion of those rights for the time being to support its MLP as it completes several major growth projects. In fact, last quarter it agreed to a further reduction in IDRs, which will increase each quarter from a rate of $75 million last quarter up to $130 million in the fourth quarter next year. Because of that, it does not have as much cash flow coming in to grow its payout as it initially anticipated.

Furthermore, both Energy Transfer entities recently agreed to provide similar support to Sunoco Logistics Partners in connection with its recent $760 million acquisition of crude oil logistics assets in the Permian Basin. Under the terms of the agreement, the Energy Transfer entitiesagreed to reduce Sunoco Logistics' incentive distribution rights by $60 million over the next two years. The net result is less income flowing into Energy Transfer Equity's coffers over the near term.

Patience is the key

Because of these agreements, as well as balance sheet concerns within the group, analysts do not believe that Energy Transfer Equity will be in the position to increase its distribution anytime soon.

Barclays, for example, expects that Energy Transfer Equity will keep its distribution flat through the end of next year as it provides additional support to its namesake MLP. The bank's analysts believe that once the support agreement ends that the company will restart distribution growth, possibly in early 2018. They also predict a payout increase by an average of 22% per year from 2018 through 2020.

Analysts at Baird, on the other hand, expect that Energy Transfer Equity will maintain its distribution at the current rate all the way through 2018. Driving that belief is Energy Transfer Equity' balance sheet, which is junk rated. As a result, the company might take the excess cash flow it generates over the next few years to trim its debt before boosting shareholder distributions.

Meanwhile, other analysts have yet to weigh in on when they believe Energy Transfer Equity will restart distribution growth. Goldman Sachs, for example, reminded investors that the company has a major project of its own in the backlog, with it currently pushing forward the proposed $8.6 billion Lake Charles LNG export project. While it would be splitting the cost of that facility 60%-40% with Energy Transfer Partners, the high capital costs could cause the companies to use excess cash flow to fund a portion of the project. That path could result in the distribution staying flat well into the 2020s when the project finally goes into service.

Investor takeaway

If there is one thing analysts agree on, it is that they do not expect Energy Transfer Equity to resume distribution growth anytime soon. Unless there is a major change, such as a significant rebound in the energy market or a transformational merger, it appears unlikely that Energy Transfer willbe in the position to increase its distribution until the end of next year at the earliest.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.