The Single Biggest Risk to Clean Energy Fuels Corp in 2017

Over the past couple of years,Clean Energy Fuels Corp(NASDAQ: CLNE) has issued a lot of cheap stock to pay down debt and raise cash. Heading into 2017, there's an argument that the company was in a pretty decent position to turn cash-flow positive. This would be particularly true if fuel volume sales continue to grow, as they have for years, even through the energy downturn.

But at the same time, there remain risks, as the company still needs to show that it can steadily and regularly produce profitable cash flows for a sustained period of time. Factor in a recent asset sale that raised $155 million in cash to reduce debt, but will have a negative impact on gross margins going forward, and there's uncertainty about the company's ability to make a profit.

Image source: Getty Images.

What's the biggest risk to the company in 2017? It could be the loss of the volumetric excise tax credit, also called VETC, which was worth $28 million in cash to the company in 2016. Let's take a closer look at this risk, and what to expect.

What is VETC?

Image source: Clean Energy Fuels.

In short, it's a tax credit worth $0.50 per gasoline gallon equivalent of compressed natural gas, or diesel gallon equivalent of liquefied natural gas, and Clean Energy has been able to claim this tax credit for a portion of its fuel sales each year.This credit exceeds the current gas and diesel excise tax of $0.184 and $0.244, respectively, per gallon.

In short, this tax credit had been used as an incentive for fleet operators to adopt natural gas vehicles, as it helped offset the incremental cost of a natural gas vehicle versus a similar gas- or diesel-powered version. This tax credit generally belonged to the fuel user, but Clean Energy has been able to claim around $25 million-$28 million in annual VETC credits in recent years.

When a political football impacts a company's cash flows

VETC expired at the end of 2016 with a lack of legislative momentum in the "lame duck" period at the end of Barack Obama's second term. Since the inauguration of President Trump, there has been little action on getting VETC, or any of the other so-called "tax extenders" group of credits, extended.

Will Congress and the Trump administration pick it up soon? There's some possibility, with congressional leaders and the President saying that they're ready to move on to tax reform. Unfortunately, it's far from clear if there will be enough common ground between congressional budget hawks and more moderate Republicans to get a deal done.

Chances are, VETC and every other expired tax incentive won't move forward unless there's a bigger reform effort, or until it becomes clear that won't happen. And frankly, after the Obamacare "repeal and replace" debacle, there's no telling what will happen.

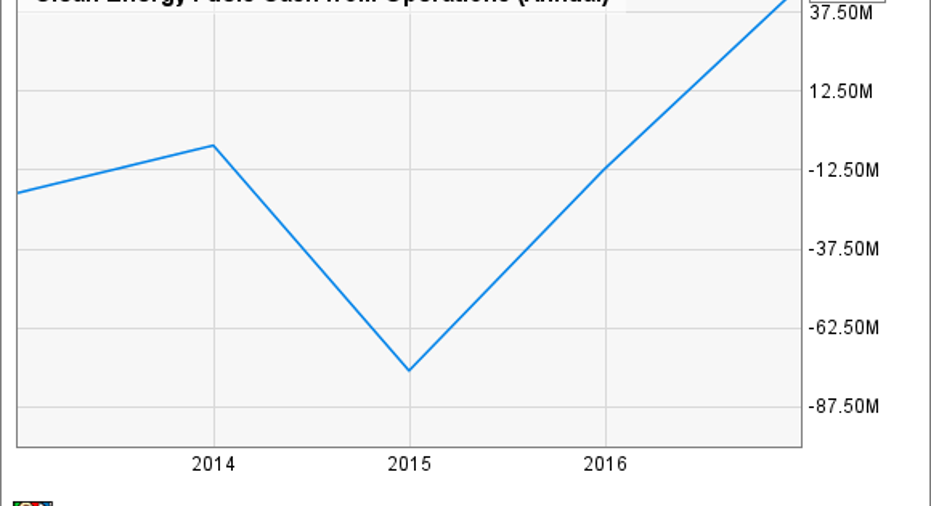

This isn't the first time political gridlock has impacted VETC and Clean Energy's cash flows. VETC similarly expired at the end of 2014 and wasn't on the books for almost all of 2015 before being reinstated in December, and being made retroactive to the entire year. Here's how that affected the company's cash flows:

CLNE Cash from Operations (Annual) data by YCharts.

As the chart shows, Clean Energy saw its operating cash flows plummet in 2014, though not entirely due to the expiration of VETC. However, its reinstatement near the end of the year played a substantial role in 2015 cash-flow growth, as the company received two year's worth of VETC revenue.

How will this affect Clean Energy in 2017?

With VETC expired and no clear political path forward, investors should probably assume the worst -- that this tax credit may not come back for some time, if ever. And that likely means at least $28 million in reduced cash flows this year. The good news is the company is probably much better able to deal with that loss than it was even a few years ago.

In recent years, Clean Energy has steadily cut costs and paid off lots of debt. Two line items -- selling, general, and administrative expenses (SG&A) and interest expense -- are on track to be as much as $55 million lower in 2017 than they were in 2014, for example, while capital expenditures will be down by $60 million from that year.

Fuel volumes also continue to grow, and the company is set to build and sell the most stations to its customers this year than ever. Gains in these areas should help offset the loss of VETC revenue.

Will the cost cuts and the sales growth be enough to offset the loss of VETC? It's not completely clear that it will, but that doesn't mean the company can't survive without this program. Clean Energy's balance sheet is much stronger now than it's been in years, with far less debt and enough cash on hand to bridge the gap, if necessary, while fuel volumes continue to grow on steady, if slow, adoption of natural gas vehicles.

Bottom line: Losing VETC will be a big blow to cash flows, but it seems unlikely that this will cause the company any lasting or permanent problems.

10 stocks we like better than Clean Energy FuelsWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Clean Energy Fuels wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Jason Hall owns shares of Clean Energy Fuels. Jason Hall has the following options: long January 2018 $3 calls on Clean Energy Fuels. The Motley Fool owns shares of and recommends Clean Energy Fuels. The Motley Fool has a disclosure policy.