The Most Important Homeownership Chart You'll Ever See

To be perfectly clear from the start, I'm a big advocate of homeownership. I own my own home, and have written before about all the reasons to buy a home. I simply believe that for many people, owning a home is a smart financial decision and here's why.

The financial benefits of owning a home

To illustrate the potential long-term financial benefits of homeownership, let's consider an example. We'll say that you're 30 years old and are debating between buying and renting, and that you have a $1,500 monthly budget for housing and enough cash in the bank for a 20% down payment. (Note: I'm aware that assuming you have enough cash to put 20% down is a big assumption.)

Based on a 30-year mortgage interest rate of 4% and the national average rates for property taxes and homeowner's insurance, this means that you could afford a $314,000 house.

Consider the following statistics and what they mean in this situation:

- Historically, home prices have increased at an average rate of 3%-4% per year. Assuming the lower end of this range, your house could be worth more than $762,000 after 30 years.

- Rent has historically increased at approximately the same rate. This means that after 30 years, your $1,500 monthly rent could balloon to $3,534 on the low end. Meanwhile, your mortgage payment (principal and interest) will stay the same -- in fact, after 30 years, your mortgage payment becomes $0.

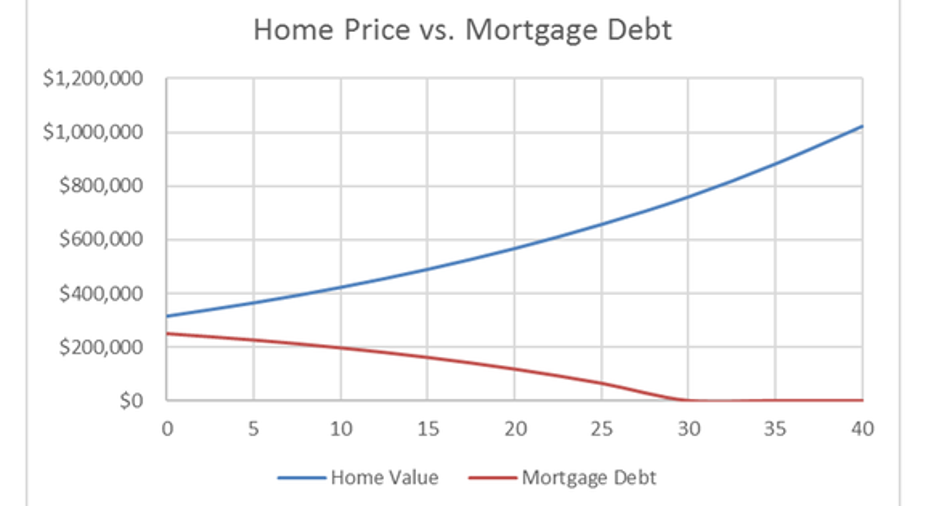

Perhaps the best argument to be made for buying a home and living in it for decades is this chart of home value versus mortgage debt over a 40-year period:

Data source: Author.

As we said, after 30 years, your home could be worth $762,000 and you'll owe no money. You would have paid $432,000 in principal and interest mortgage payments over the years. Even if we assume that your taxes and insurance costs will grow at a high rate of 5% per year, this still only translates to total housing costs of $671,000 over three decades -- less than the end value of the home. You could then sell it and put this cash in your pocket, minus any real estate commissions.

Meanwhile, if you had rented, you would have paid $856,357 in rent over 30 years, and would have no equity to show for it. This is a big reason why the Federal Reserve's Survey of Consumer Finances found a big gap between the net worth of homeowners and renters of all income levels.

Data source: Federal Reserve Board via www.risingrealty.com.

Reasons to buy and reasons to rent

In addition to the long-term financial reasons I already discussed, there are several other compelling reasons to buy a home, including:

- More location choices -- It's next to impossible to rent a home in many neighborhoods across the country.

- The freedom to customize -- If you want to paint the walls, build a fence, or put in a swimming pool, homeownership is the way to go.

- Lock in low mortgage rates -- Interest rates are still near record lows, and are widely expected to rise during the coming years.

- Tax breaks -- Homeowners may be able to deduct their mortgage interest, property taxes, and any mortgage insurance premiums from their taxable income.

However, I realize that owning a home isn't the best move for everyone. There are some good reasons you might be better off renting, such as:

- Smaller time commitment -- Buying a house is rarely a good idea if you're not going to stay in it for at least a few years. Renting is usually a better option if you want or need the flexibility to move around.

- No maintenance expense -- If you own a home, you'll need to maintain it. If a toilet breaks, the dishwasher stops working, or your roof starts to leak, you'll need to deal with it. As a renter, these things are as easy and cheap as a phone call to your landlord.

- Only one bill -- As a tenant, you won't need to worry about property taxes or hazard insurance, which can increase annually and can be rather high in some parts of the country. For example, the first house I owned was in the Florida Keys, and our homeowner's, windstorm, and flood insurance premiums added up to almost as much as the principal and interest payment on the mortgage.

This chart doesn't tell the whole story, but...

As I mentioned, homeownership is not for everyone, and there are some compelling reasons in favor of owning and renting. However, from a purely financial standpoint, it's tough to argue with the long-term benefits of buying a home.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies..

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.