The Key Numbers From Wells Fargo's Earnings

In a week when coal miner filed for bankruptcy and rival bank increased its provision for credit losses by 46% largely because of pressure on its energy, metals and mining clients, investors' focus was naturally on energy portfolio. Let's take a look at how credit loss provisions hit income at Wells Fargo, and the other key takeaways from the first-quarter report.

It's a good idea to separate interest and non-interest income in a bank's earnings report, so here are the key numbers.

As you can see below, the increase in credit loss provisions of $478 million significantly profitability, even though oil and gas loans only make up 1.9% of Wells Fargo's outstanding loans. In fact, if credit loss provisions had been stable then income before income tax expense would have risen 4.9% instead of the reported 1% decline.

|

Q1 2016 |

Q1 2015 |

Change |

|

|---|---|---|---|

|

Net Interest Income |

11667 |

10986 |

6.2% |

|

Provision for credit losses |

1086 |

608 |

78.6% |

|

Net Interest Income after credit loss provision |

10581 |

10378 |

2% |

|

Noninterest Income |

10528 |

10292 |

2.3% |

|

Noninterest Expense |

13028 |

12507 |

4.2% |

|

Income before income tax expense |

8081 |

8163 |

(1%) |

DATA SOURCE: WELLS FARGO PRESENTATIONS

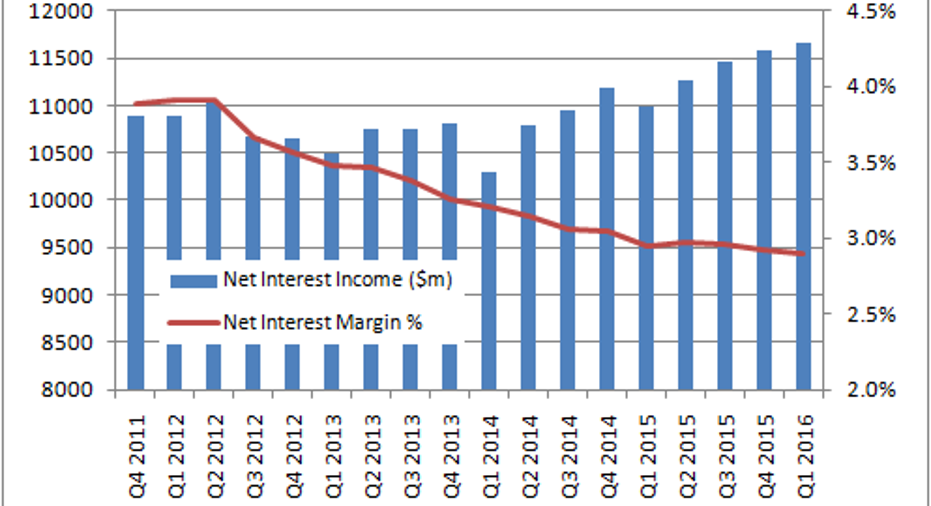

Interest income Aside from credit loss provisions, the two key measures to follow here are net interest margin (NIM) and loan growth. NIM is the difference between the interest a bank's investments generates and interest expense divided by its average interest earning assets. A higher NIM is better.

As you can see below, the bank is doing a pretty good job of increasing net interest income while NIM continues to decline. Incidentally, JPMorgan did better with its net yield on interest earning assets, increasing it to 2.3% from 2.23% the previous quarter.

DATA SOURCE: WELLS FARGO PRESENTATIONS

One way Wells Fargo is managing to grow net interest income is through expanding its loan book through organic growth and via acquisitions. For example, total loans increased a total of $30.7 billion from the previous quarter to $947.3 billion, largely thanks to a $24.9 billion contribution from the acquisitions made from GE Capital. Sometimes banks will take on riskier loans with higher interest rates in order to juice NIM. Fortunately for investors, Wells Fargo is typically a conservative underwriter and unlikely to have taken on bad debt.

Meanwhile, consumer lending had a solid-quarter. Home lending originations decreased $3 billion from the previous quarter to $44 billion, but applications (a measure of future growth) of $77 billion increased 20% from the previous quarter. In addition, auto originations increased 2% from the previous quarter and 9% compared to last year -- autos remain a bright spot in the economy.

Non-interest incomeOn the non-interest income side, there was some disappointment with non-interest expense rising 4.2%, more than offsetting the 2.3% increase in non-interest income.

Wells Fargo gauges its non-interest expenses with something called the "efficiency ratio." In simple terms, it's non-interest expenses divided by net interest income plus non-interest income -- a lower number is better. The first-quarter efficiency ratio came in at 58.7% compared to 58.8% in the same period last year.

Wells Fargo management expects it to continue at the high-end of its target range of 55%-59% for the full-year. By way of comparison, JPMorgan's efficiency ratio was 59.5% in the first-quarter compared to 61.8% a year ago. Clearly, JP Morgan is doing better than Wells Fargo in terms of reducing the efficiency ratio -- a key point as non-interest income growth is proving hard to come by in a low-growth economy.

Looking aheadAll told, it's clearly a difficult market for the banks and Wells Fargo and JPMorgan are both finding it hard to grow earnings as the economy continues to grow moderately and interest rates (and the NIM) remain low. In addition, both banks got hit by the deteriorating energy market, and there is no telling when energy market conditions will improve.

Focusing on Wells Fargo, if the economy remains in moderate growth mode, the bank will need to increase its interest income by growing its loan book, while trying to reduce its efficiency ratio on the non-interest income side.

The article The Key Numbers From Wells Fargo's Earnings originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool has the following options: short May 2016 $52 puts on Wells Fargo. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.