The Fourth Quarter Could Get Interesting for HCP Shareholders

Image Source: Getty Images

Earlier in 2016, healthcare REIT HCP, Inc. (NYSE: HCP) announced plans to spin off more than 300 of its properties into a newly created REIT. Well, the time is almost here. Here's the latest information about the upcoming spinoff, and what investors can expect after it's completed.

What we know about the spinoff

In its first-quarter earnings release, HCP, Inc. announced its plans to spin off the company's post-acute/skilled nursing properties, virtually all of which are a partnership with HCR ManorCare, into a newly created REIT. The new REIT will consist of 337 properties,and we have recently learned it will be called QCP, short for Quality Care Properties.

QCP's initial portfolio will consist of 274 post-acute/skilled nursing properties, 62 memory care/assisted living properties, and one surgical hospital. Additionally, QCP will own HCP's equity interest in HCR ManorCare of about 9%.

According to the most recent information, the spinoff is expected to be completed during the fourth quarter of 2016, and each current HCP shareholder will receive one share of QCP for every five shares of HCP stock held on the yet-to-be-announced record date. I anticipate this detail coming along with the upcoming third-quarter earnings release, but that's just my prediction. QCP has applied to list under the stock symbol "QCP", but this has also not been finalized as of this writing. The board of directors has approved the spinoff plan, and no shareholder vote is required.

We also know HCP's management team will consist of CEO Mark Ordan, President and CIO Greg Neeb, and CFO C. Marc Richards. All three have worked together previously, and bring a great deal of experience to the table.

Most recently, we've learned new details about HCP's financing structure. The company had previously said in regulatory filings that $1.8 billion in debt would give QCP sufficient flexibility to support its business and operating plan, including the approximately $1.7 billion that will be transferred to HCP in exchange for the assets. This will then be used to repay a portion of HCP's outstanding debt.

The company just announced a $750 million debt offering, a $1 billion term loan, and a $100 million five-year revolving credit facility. So it appears that QCP's capital requirements have been met.

Why does HCP want to get rid of its HCR ManorCare properties?

Simply put, HCP's focus is on maintaining a portfolio of rock-solid income-generating healthcare properties, and the HCR ManorCare properties haven't been up to par lately. Several industry headwinds, such as the shift away from a fee-for-service model, an increased number of Medicare Advantage plans, and increased scrutiny on government reimbursements have caused HCR ManorCare's performance to deteriorate, specifically in the latter half of 2015.

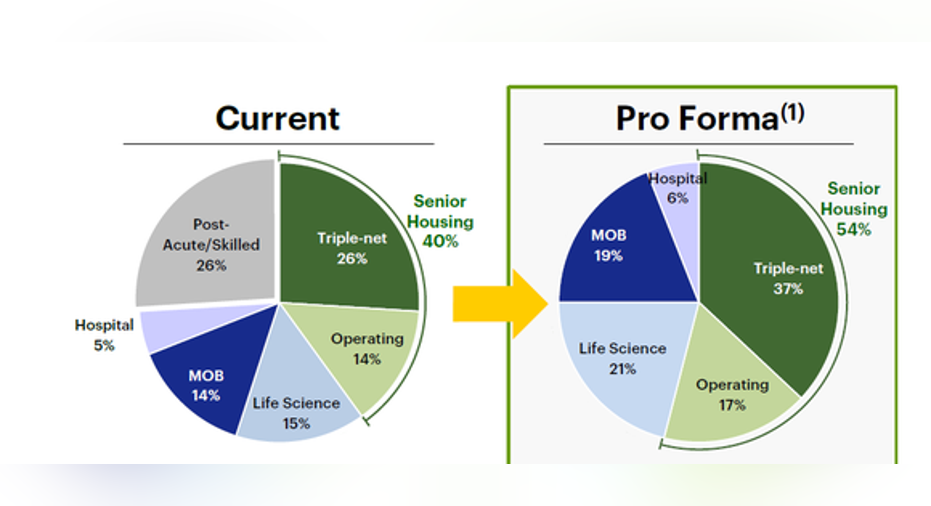

Shedding the HCR ManorCare assets will greatly improve the portfolio quality and growth profile of the remaining HCP portfolio, which will consist of about 850 senior housing, life science, and medical office properties. Nearly all of the remaining properties will be private-pay (stable), and the spinoff will result in an overall higher asset quality, as well as improved tenant diversification. After all, HCR ManorCare is a major tenant, making up about one-fourth of HCP's current portfolio.

Image source: HCP spin-off investor presentation

Theoretically, this improved quality will result in a lower cost of capital, and therefore more potential for growth through acquisitions at attractive spreads.

The spun-off QCP will also be set up for success, with a management team focused solely on maximizing the value of the post-acute/skilled nursing properties. HCP has stated that QCP will be able to use value-maximizing strategies that are either impractical or unavailable while the properties are still under the umbrella of HCP. QCP will be one of the largest REITs focused on its property type in the United States.

What to expect post-spinoff

The spinoff is likely to create some volatility in the short-term as the dust settles and the two new companies get used to operating independently. There's also the question of HCP's dividend, which has been raised every year for more than a quarter-century. You can bet that shareholders will be paying close attention to both REITs' dividend policies through this process.

However, the long-term potential created by the spinoff definitely outweighs the short-term volatility investors can expect. I don't think it will be long after the split before HCP becomes a rock-solid dividend powerhouse again, and if the HCR ManorCare assets actually start generating a significant profit, there is some serious upside potential from QCP. In the meantime, hold on tight -- it might be a bumpy ride in the fourth quarter.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matthew Frankel owns shares of HCP. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.